• Institutions and investors have their eyes fixed on today’s US Inflation rate. Analysts expect the Consumer Price Index to read 0.2% and Core CPI 0.3%.

• The US Securities and Exchange Commission gives a Bitcoin Spot ETF the green light, but Bitcoin trades lower. This is potentially due to the upcoming vital inflation data.

• JP Morgan advise the Federal Reserve may cut more than it is signalling. However, monetary policy continues to depend on inflation data.

• Europe stocks are poised to open higher ahead of today’s US inflation data which will affect more than just US-linked assets.

USA100 – NASDAQ Corrects Previous Losses!

The price of the USA100 has now officially redeemed all lost ground from the previous week. The USA100 is now trading close to the all-time highs from December 2023, and investors are considering whether the asset will continue to renew highs. This is something we will look at throughout today’s article. Up to now, the USA100 is forming its fifth consecutive day of climbs and has already added 0.40% during this morning’s Asian session.

The performance of the USA100 will depend on three major factors: interest rate cuts, the soft-landing possibilities and AI demand. If inflation does indeed continue to decline and interest rates fall, investors are more likely to invest in the stock market. This is because the possibility of the economy avoiding a recession will remain high. In addition to this, the recent demand has also been due to higher earnings and the AI drive. In order for demand and momentum to remain, these two factors will need to persist.

The US inflation rate over the past 6 months has largely been due to Core Services, whereas the rest of the basket is close to experiencing stagnation. Therefore, this area is where investors will be keen to see lower figures. If Core CPI figures read lower than 0.3%, investors may be more driven and persuaded to invest in Tech.

In addition to this, JP Morgan advise the Federal Reserve may cut more than the policymakers had signaled towards the end of 2023. However, according to JP Morgan analysts, this is only a possibility if the economy starts to witness a slowdown. When looking at the top 10 stocks holding the highest weight within the index, 8 of the ten ended the day higher. Only Broadcom and Tesla witnessed a decline. The best performing stocks within the index were Intuitive Surgical +10.25%, Palo Alto Networks +5.22% and Meta +3.65%. The price of the top three most influential stocks (Apple, Microsoft and Alphabet) are also trading higher after trading hours.

Lastly, bond yields this morning are trading significantly lower, declining 0.40% and have again dropped below 4.00%. Lower bond yields are known to also support the stock market as it creates an environment with lower borrowing costs. However, as mentioned above, the key price driver will be this afternoon’s inflation data. The same will apply to Bitcoin even after the SEC approval of a Spot ETF. In terms of technical analysis, the price continues to trade above price sentiment indications, oscillators, and the day’s VWAP. Therefore, technical analysis continues to signal a potential price increase.

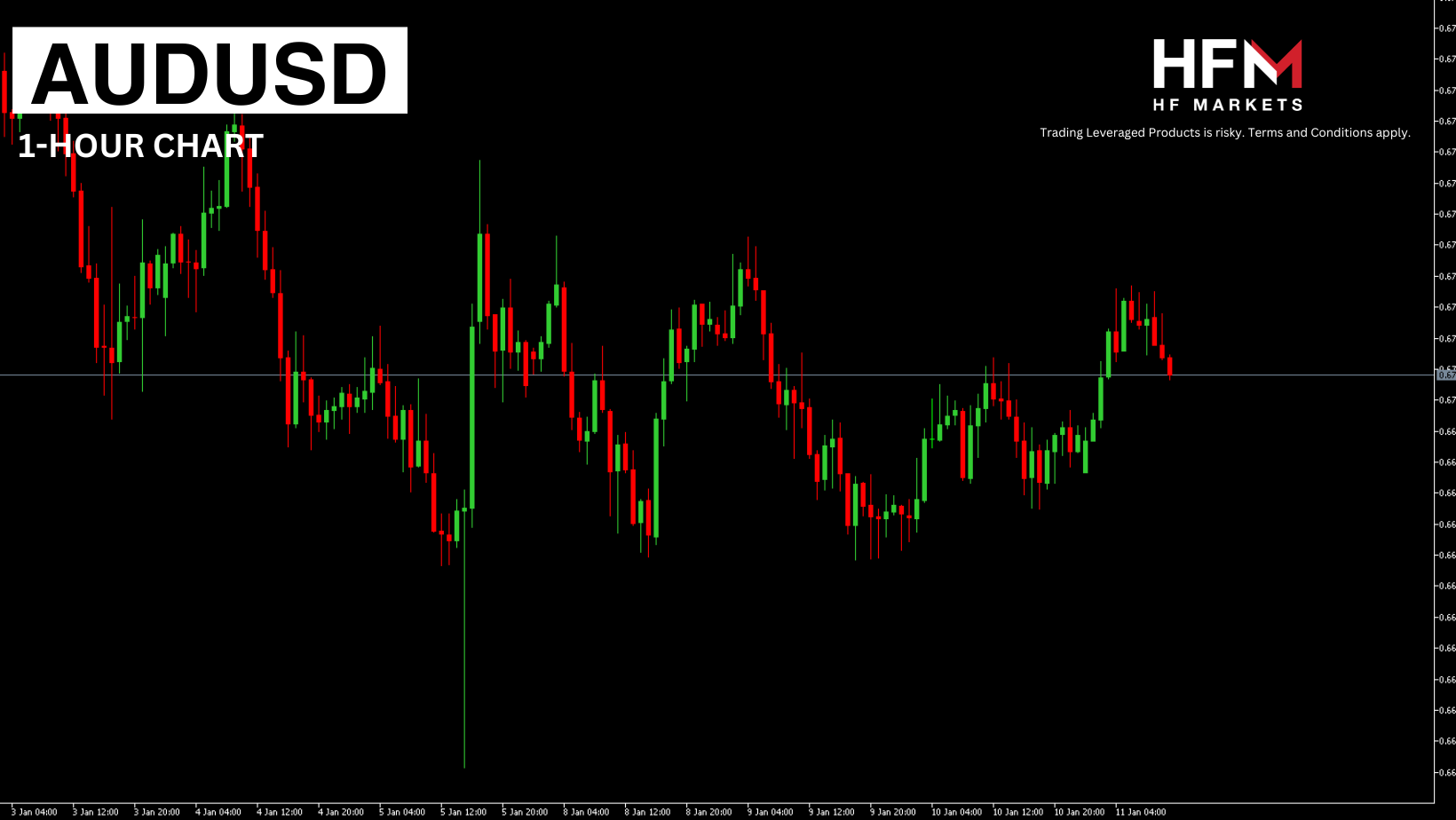

AUDUSD Forms Symmetrical Triangle Pattern Ahead of CPI Release!

The price of the AUDUSD is trading slightly lower than the 75-bar Exponential Moving Average and is also forming a symmetrical triangle pattern. Due to this, the exchange rate is trading at a neutral area which indicates the asset could swing in either direction. If the exchange rate breaks above 0.67330, the asset is likely to obtain buy signals. Whereas a price below 0.67000 will trigger sell signals to materialize. However, the movement will again depend on today’s US CPI.

In turn, the Australian Monthly Consumer Price Index was recorded at 4.3% in November, below preliminary estimates of 4.4%, and reflecting the slowest growth since January 2022. The data excluding prices for fuel, food, as well as tourist trips, amounted to 4.8% after 5.1% in October. The statistics confirm the majority view that the Reserve Bank of Australia will leave interest rates unchanged in the foreseeable future but continue its trend of tightening monetary conditions to contain inflation pressures.

Click here to access our Economic Calendar

Michalis Efthymiou

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.