The Walt Disney Co., a diversified international family entertainment and media enterprise founded since 1923, shall release its Q1 2024 earnings result on 7th February (Wednesday), after market close. The company operates via two main segments: Disney Media and Entertainment Distribution (DMED) and Disney Parks, Experiences and Products (DPEP). The former covers the company’s global film, television content production and distribution activities, while the latter encompasses parks and experiences and consumer products.

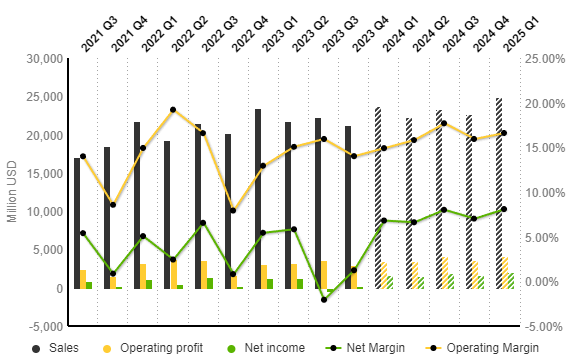

Walt Disney generated $21.2B revenue in Q4 2023, down -4.88% from the previous quarter, but up 5.41% from the same period last year. According to the official report, revenue generated from the Disney Parks segment was up 13% (y/y) to $8.2B (boosted by gains in international parks buoyed by increased attendance and guest spending growth, but slightly offset by lower results at domestic parks and resorts). Nevertheless, segment operating income was up 31% (y/y) to $1.76B.

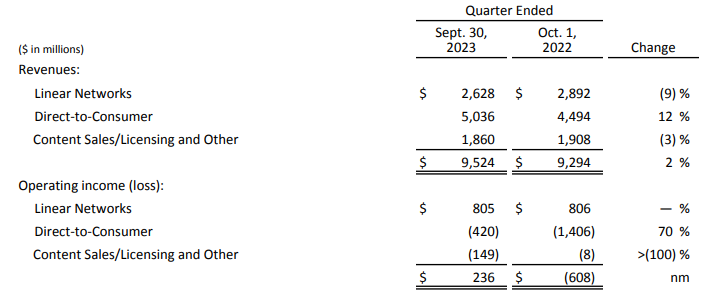

On the contrary, the company’s Media and Entertainment Distribution was up 2% (y/y) in revenue to $9.5B. Both domestic and international channels reported losses, leading to Linear Networks down -9% (y/y) to $2.6B. Operating income for the segment were down -5% (y/y) and -3% (y/y) for domestic and international section, to $528 million and $115 million, respectively. Revenue for Content Sales/Licensing and Other was down -3% (y/y) to $1.86B. The losses of the two segments were slightly offset by gains in the Direct-to-Consumer segment, which was up 12% (y/y) to $5.04B. Its operating losses narrowed to -$0.42B (was -$1.41B in the same period last year), following higher subscription revenue (from Disney+ Core and Hulu), as well as reduced cost in marketing, technology and distribution.

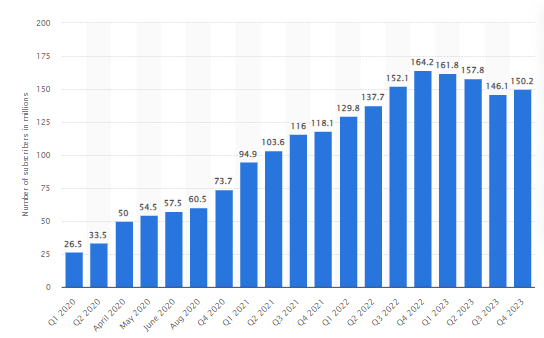

The company reported an improvement in global Disney+ subscribers, to 150.2 million, marking the end of the falling trend for three consecutive quarters. By average monthly revenue per paid subscriber (ARPU), domestic Disney+ reported an increase of $0.19 from the previous quarter to $7.50, whereas International Disney+ reported an increase of $0.09 to $6.10. The former was attributed to higher advertising revenue, while the latter was attributed to an increase in average retail pricing, but partially offset by a higher mix of subscribers to promotional offerings.

All in all, the management remains optimistic over the outlook in the near term:

“As we look forward, there are four key building opportunities that will be central to our success: achieving significant and sustained profitability in our streaming business, building ESPN into the preeminent digital sports platform, improving the output and economics of our film studios, and turbocharging growth in our parks and experiences business,” – CEO Bob Iger

In addition to that, key focus will be on the company’s streaming business profitability and subscriber growth, consumer demand as well as its cost management approach.

According to projections by S&P Global Market Intelligence, sales revenue is expected to reach $23.8B in the coming quarter, up 12% from the previous quarter, and up 1.2% from the same period last year. Operating profit and net income should see significant improvement, at $3.5B and $1.62B respectively. This would bring net margin and operating margin up by 5.56% and 0.9% from the previous quarter, to 6.80% and 14.91%, slightly better than the results in the same period last year.

Technical Analysis:

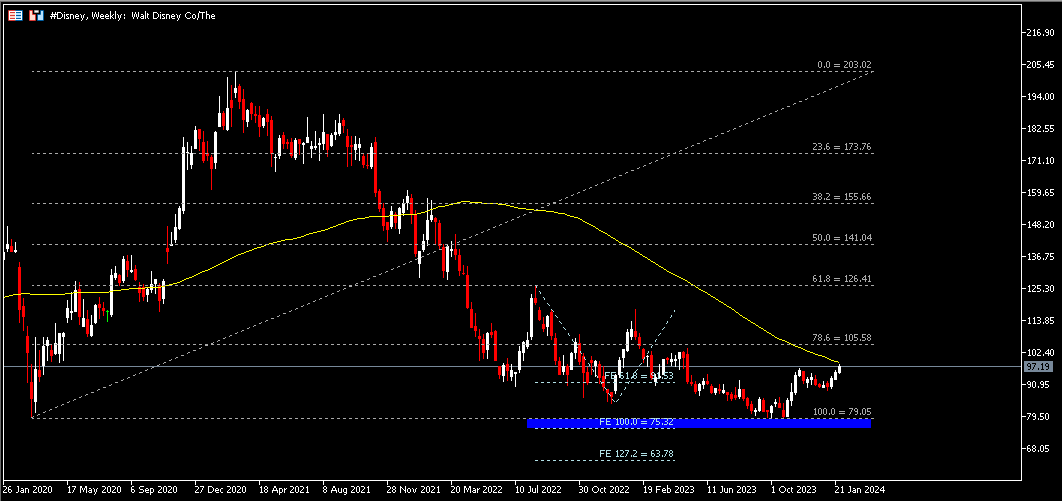

The #Disney share price remains clearly above its 52-week low ($78.73). The level together with $75.30 projected from Fibonacci Expansion, form a strong support zone. The latest stock price closed above FE 61.8%, or $91.55, and approaching 100-week SMA. A bullish breakout above this dynamic resistance may bring $105.60 (FR 78.6%, extended from the lows in March 2020 to the highs in March 2021) into focus, followed by $126.40 (FR 61.8%).

Click here to access our Economic Calendar

Larince Zhang

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.