Although the BOJ ended negative interest rates, this did not indicate a hawkish stance, but rather a dovish rate hike.

USDJPY on Tuesday [19th Mar] was up +1.17%. The yen fell to a 4-month low against the dollar based on dovish comments from BOJ Governor Ueda, who said BOJ policy will remain accommodative, even after ending the negative interest rate campaign. In addition, the yen came under pressure on Tuesday as 10-year JGB bond yields fell to a 1½-week low, after the BOJ said it would continue to buy long-term government bonds as needed.

After the meeting ended, the Bank of Japan announced the end of its Yield Curve Control framework and negative interest rate policy, saying that these measures had been instrumental in a significant change in Japan’s monetary policy. The BOJ’s conclusion that a virtuous cycle between wages and prices has developed and that the long-term inflation target of 2% is expected to be achieved in a sustainable and stable manner formed the basis for these significant actions. The majority of board members by a vote of 7-2, decided to set the overnight lending rate between 0 – 1.1%.

In order to maintain a certain degree of stability in the bond market, the BOJ will continue to purchase Japanese government bonds in roughly the same amount as before. By a vote of 8 to 1, this decision was hammered out. At the same time, the BOJ promised to respond flexibly, if long-term interest rates rise rapidly. In addition, the BOJ intends to stop purchases of J-REITs and ETFs and will gradually reduce purchases of corporate bonds and securities with the aim of stopping purchases in about a year.

Although the BOJ stopped negative interest rates, the move was more dovish than hawkish rate hikes. Further policy steps to normalise monetary policy may be taken, if there are more indications that inflation continues to be on target. The BOJ’s decision to stop negative interest rates did not come as any surprise, as it was expected. The JPY did not appreciate significantly, despite the symbolic end of negative interest rates.

In the market, the Yen did not gain much despite the end of negative interest rates. Additional BOJ rate hike cues are the only way for the Yen to gain strength.

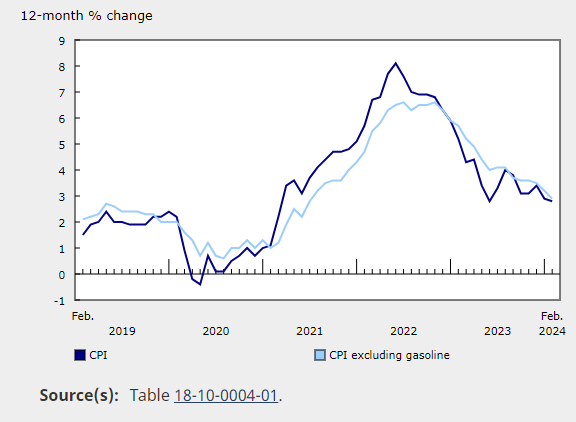

Meanwhile, from Canada, it was reported that the CPI for February decelerated to record an increase of 2.8% y/y, lower than the forecast of 3.1% y/y. This slowdown from 2.9% y/y in January offers some relief, as inflationary pressures show signs of easing. Excluding petrol, CPI fell from 3.2% y/y to 2.9% y/y. Petrol prices alone saw a slight increase of 0.8% y/y, a notable recovery from the -4.0% y/y decline observed in the previous month.

Median CPI, which is a measure that provides a middle ground by excluding extreme fluctuations, slowed from 3.3% y/y to 3.1% y/y, lower than the forecast of 3.3%. Similarly, the trimmed CPI, which removes the most volatile components, fell from 3.4% y/y to 3.2% y/y. Lastly, the headline CPI, which is often considered the core measure that tracks general price changes across categories, slowed from 3.4% y/y to 3.1% y/y, again missing the forecast of 3.4%.

In the Forex market, the CADJPY pair recorded a 16-year high of 111.80 last February before correcting to a 38.2%FR level of 108.67.

Further upside is still expected to chase the 111.80 high.A breakout of this level will confirm, that the continued uptrend from the 94.06 second leg is not yet over and another leg up will follow with projections for FE61.8% from 104.21 – 111.80 and 108.67 drawdown at 113.38.

Nonetheless, the continued rally will meet resistance at 111.80.As long as this level can hold, it will bring some consolidation first.

A drop below 108.67 is needed to confirm the near-term bearish trend going forward.

Click here to access our Economic Calendar

Ady Phangestu

Market Analyst – HF Educational Office – Indonesia

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.