- The price of Gold declines 1.10% along with other metals and most commodities.

- The more expensive US Dollar and higher bond yields continue to pressure Gold.

- The US Dollar Index is the only currency index which is trading higher during today’s European and Asian sessions.

- The US Employment Cost Index rises to its highest level in 12 months and surpasses previous expectations. As a result, the US Dollar Index trades 0.42% higher.

XAUUSD – Metals and Commodities Struggle Ahead of Event Packed Wednesday.

The price of Gold has declined 1.10% and is experiencing its strongest decline since April 22nd. The reasoning behind the decline is de-escalation in the middle east while the US Dollar strengthens. in addition to this, economic data continues to indicate a more hawkish Federal Reserve.

This afternoon, the US released their latest Employment Cost Index which read 1.2%. The index rose to its highest level in a year and read 20% higher than Wall Street’s expectations. The index measures salaries amongst private and business salaries for labour. Increases are known to create stronger upward pressure on inflation and indicate an unbalanced employment sector.

As a result, the Fed are less likely to feel the need to adjust interest rates. After this afternoon’s Employment Cost Index, more than 77% of the market believe the Fed will now not cut rates before September 2024. Furthermore, analysts are not expecting something different from Friday’s NFP reading. For this reason, Gold is witnessing lower demand and less buy orders.

The price is currently trading below the 75-Bar Exponential Moving Average and at 36.50 on the RSI. Both indicate sellers are controlling the market in the short-medium term. However, investors are also cautious that the price is trading close to support levels from the 23rd to 25th April 2024 and the divergence signal on the 15-Minute Chart. Based on the Fibonacci retracement levels, if the price drops below $2,306.10, the price may see sell signals strengthen.

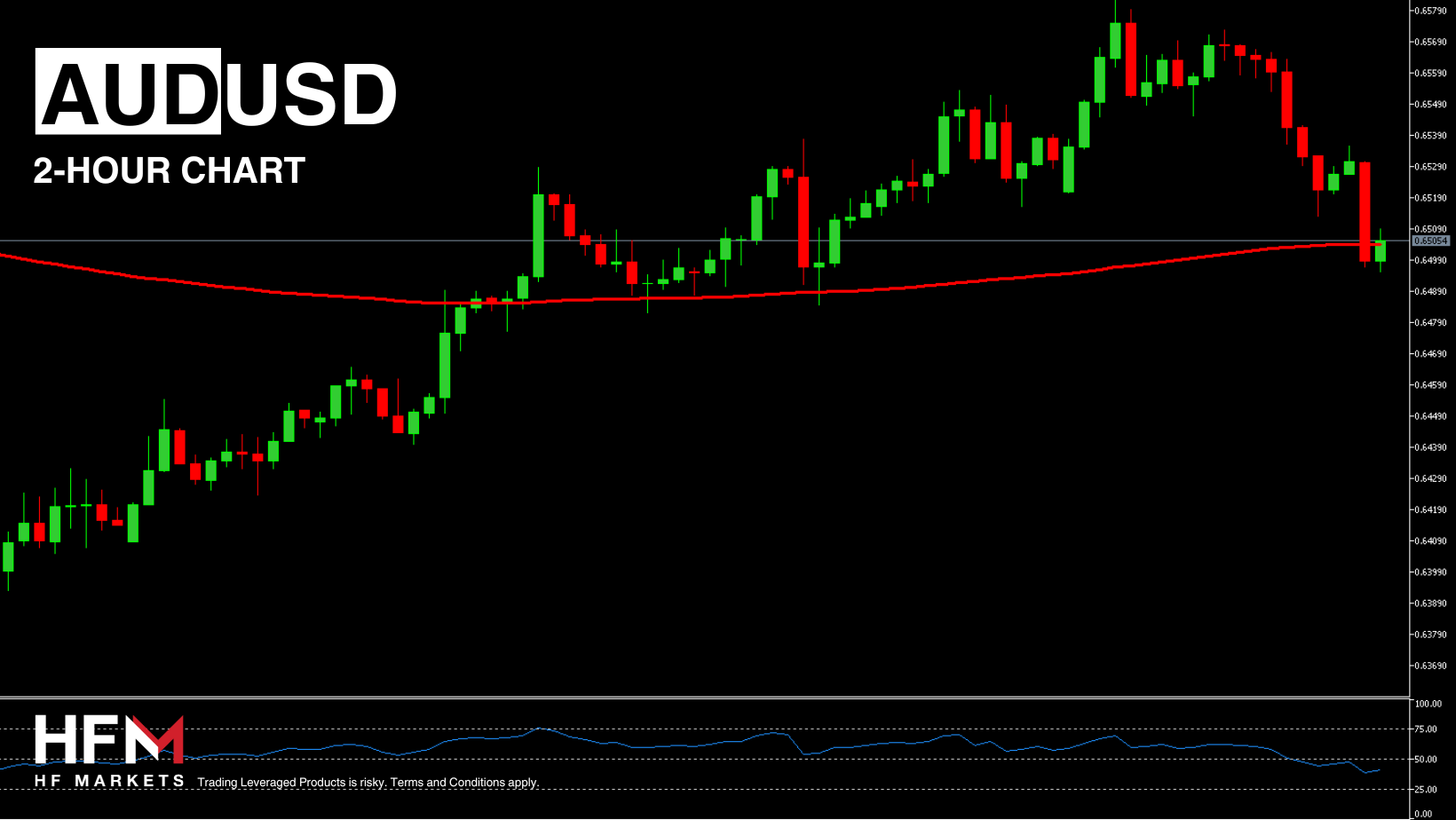

USDAUD – The Countdown Begins For the Fed’s Rate Decision and Press Conference.

Investors looking to trade the day’s best performing currency against the worst performing will be drawn to the AUD and JPY. The price of the US Dollar is largely being driven by the latest Employment data and predictions for a hawkish central bank.

The US Dollar is increasing in value against each currency and is trading 1.03% higher against the Australian Dollar. The AUDUSD is trading below the trend line for the first time since April 23rd and is witnessing “sell” signals quickly materialise. As the price is trading significantly low, some traders may opt to wait for the retracement and then trade the continuing wave. Others may consider a bearish breakout of 0.64953 as the next signal.

Tomorrow’s Federal Reserve statement and press conference will be the main price driver for the exchange rate. If the Chairman confirms the possibility of a rate cut over the summer months is diminishing, the US Dollar can continue to rise. In addition to this, the higher bond yields are also contributing to the more expensive Dollar.

Michalis Efthymiou

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.