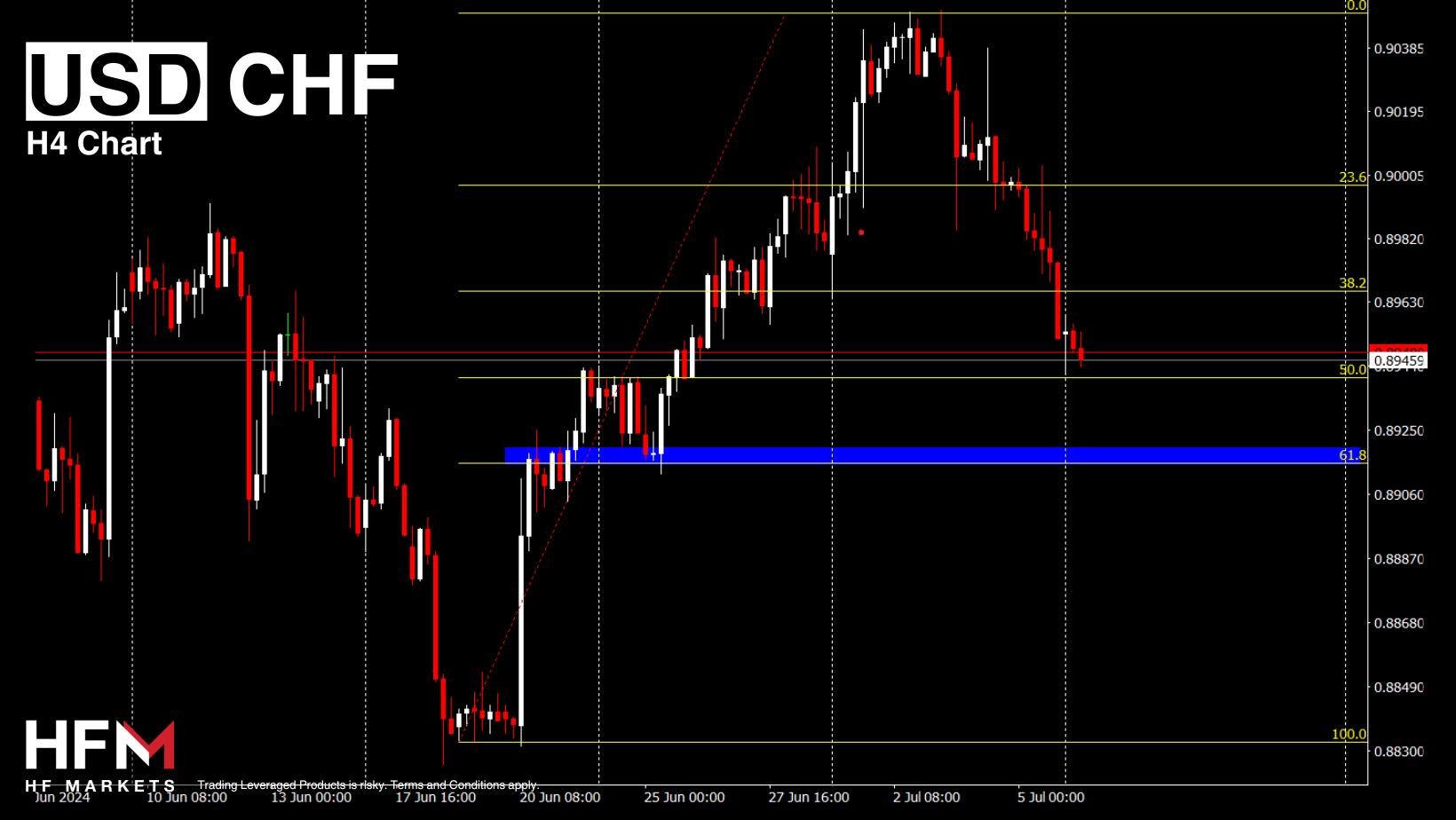

Economic Indicators & Central Banks:

- The USDIndex holds below 105, while EURUSD returned some losses and turned back to 1.0835 area. The USDJPY recovered to 160.80.

- Bitcoin fell by 5.2% to $55,290 some $19,000 below March’s record high. This is due to concerns over potential sales by creditors of the failed Mt. Gox exchange which has begun returning a roughly $8 billion hoard of the largest digital asset.

- Gold and Oil prices steadied. Oil traders monitored twin threats to production from a storm in the US and wildfires in Canada.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.