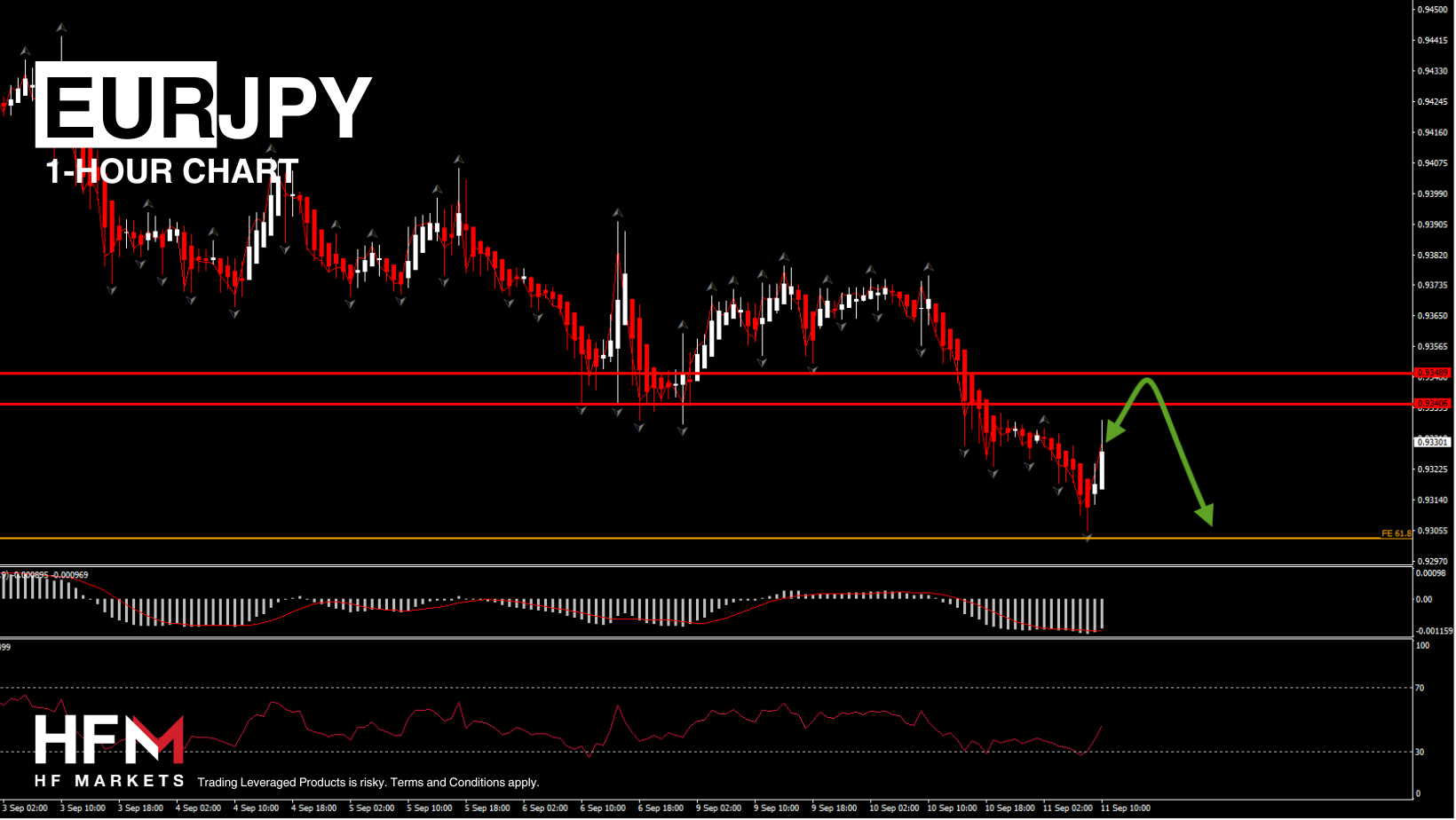

Investors remain cautious about the gloomy outlook for China’s economy & worry that the Fed has delayed easing monetary policy. Traders are anticipating at least 1 significant rate cut this year, ahead of the CPI report, which is expected to show modest inflation growth.

Asia & European Sessions:

A higher inflation reading today could lead to increased volatility ,while a softer number might give the Fed more room to cut, but could also signal faster-than-expected economic slowdown.

Financial Markets Performance:

- The Yen surged to its strongest level against the US Dollar since December, recovering its yearly losses. It is currently at 141.40 after retesting the 140.696 level.

- The USDCHF drifted further to a 13 year bottom, with CHF and JPY buoyed by faltering carry trades funded through low-interest currencies and increased demand for safe-haven assets. EURCHF remains below its 2015 bottom.

- Bitcoin dipped to $56k again due to Trump’s support for the cryptocurrency sector.

- Oil extended the month’s downleg to 65.34, dropping by nearly 20% this quarter, as worries about slowing growth in the US and China dampen demand.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.