FX News Today

- Wall Street managed modest gains, supported by a better than 1% rise in industrials which offset a drop in materials. The markets generally shrugged off a sharp drop in the Empire State manufacturing index and a weaker than expected NAHB housing market index.

- Asia stock market gains were capped by caution ahead of the Fed meeting.

- Topix and Nikkei lost -0.88% and -0.81% respectively as the Yen strengthened, the Hang Seng continued to recover and moved up 0.70% after being pressured by political protests last week.

- The ASX gained 0.54% after getting cut a boost from RBA meeting minutes signaling another rate cut could be underway.

- GER30 and UK100 futures are trading narrowly mixed.

- US futures are slightly in the red.

- Speculation that the Fed will signal rate cuts is mounting and in Europe ECB officials seem to be readying further easing measures, while the BoE is widely expected to remain on hold amid ongoing Brexit uncertainty.

Charts of the Day

Technician’s Corner

- AUDUSD also fell to a 5-month low, at 0.6833. The underperformance of the Australian dollar was catalyzed by the release of the RBA minutes to the June policy meeting, which saw the central bank cut its cash rate to a record low of 1.25%. The minutes showed that the RBA is of a mind to ease policy again, as soon as July, given prevailing concerns about unemployment and disinflation. AUDJPY pegged below 3-year lows at 74.50, hence next Support is at June 2016 low at 72.40 .

- GBPJPY has hit fresh lows, and the Yen has remained bid amid a backdrop of continued sputtering in global stock markets. GBPJPY daily volatility has fallen from 140 pips in February to less than 120 today. Key Support levels for both pairs sit at 133.80 and 132.30 respectively.

Main Macro Events Today

- Consumer Price Index (EUR, GMT 09:00) – Prices are expected to fall in May to just 0.3%m/m from 0.7%, whilst the overall inflation is expected to stand unchanged at 1.2%y/y.

- ZEW Economic Sentiment (EUR, GMT 09:00) – Economic Sentiment for June is expected to rise slightly at -0.5 compared to -2.1 last month, however the negative reading means pessimists once again outnumber optimists and that escalation in US-Sino trade relations affects the outlook.

- BoE’s Governor Carney speech (GBP, GMT 14:00)

- ECB’s President Draghi speech (EUR, GMT 14:00)

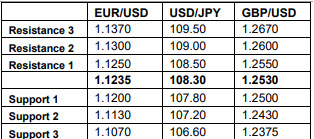

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.