FX News Today

- Treasuries were weaker Wednesday after a poorly subscribed 5-year auction, while aggressive Fed rate cut expectations continued to be priced out.

- The bond markets in Asia were under pressure as stocks moved higher.

- Markets are pinning their hopes on Saturday’s meeting between Trump and Xi Jinping at the side-lines of the G-20 meeting with reports that the US is willing to hold off further tariffs for now helping to bolster confidence.

- At the same time, President Trump threatened with additional China tariffs if there is no agreement.

- Still, without a firm and formal agreement in place risks of set backs remain high, especially as US-Iran tensions and the no-deal Brexit scenarios in Europe provide a risky backdrop.

- European stock futures are moving higher in tandem with US futures after broad gains in Asia.

- WTI crude surged to 4-week highs on API data showing big US inventory drop.

- USD is trading mixed today after rallying Tuesday on Fed’s walk back of dovish guidance.

- JPY down, Dollar bloc currencies up quite sharply on US-China optimism.

- GBP is underperforming again on persisting Brexit related demand-supply imbalance.

Charts of the Day

Technician’s Corner

- EURUSD rallied to 1.1391 highs, after bouncing from the session low at 1.1348, which is also the 200-day moving average. The pairing has since run into sellers in front of the 1.1400 mark, settling in under 1.1360. Softer US data weighed on the Dollar, though Fed Chair Powell’s more neutral stance on policy may tone down market’s aggressive easing potential, likely to limit EUR gains going forward. In addition, increasing prospects for further ECB easing should also keep a cap on EURUSD.

- AUDJPY has been the biggest mover, rising about 0.5% in printing a 16-day high at 75.62. The Yen weakened as markets opted for risk-on positioning ahead of the G20 summit. USDJPY posted an eight-day high at 108.13. This price action came as Chinese markets led broader gains across Asian stock markets, which propelled the MSCI Asia-Pacific index up by 0.6%. Meanwhile, as AUDJPY seems overbought outside from upper Bollinger Bands pattern, some correction could be seen with immediate Support at 75.33. Resistance holds at 75.67 and 75.80.

Main Macro Events Today

- Harmonized Index of Consumer Prices (EUR, GMT 12:00) – The German HICP inflation is expected to be unchanged to 1.3% y/y.

- US Final Gross Domestic Product (USD, GMT 12:30) – The final release of the Q1 GDP growth rate is expected unchanged from 3.1%, with downward revisions of -$6 bln for service consumption and -$1 bln for factory inventories.

- Tokyo CPI and Production Data (JPY, GMT 23:30) – The country’s main leading indicator of inflation is expected to have grown at 1.3% y/y in June, and at 1.2% y/y ex Fresh Food. Industrial Production should post a 2.6% decline y/y in May, compared to -1.1% in April.

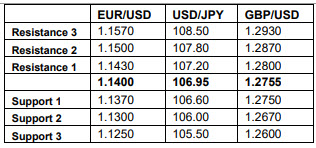

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.