The Dollar got a small boost following the data, where jobless claims were in line with expectations, and the Philly Fed index came in much stronger than expected. US initial jobless claims rose 8k to 216k in the week ended July 13. US Philly Fed index bounced 21.5 points to 21.8 in July, much better than expected. It more than erases 16.3 point drop to 0.3 in June. This is the best in a year, while the June figure was the worst since the -4.1 from February which was a 33-month nadir.

Overall, the Greenback so far today has rebounded after printing fresh lows against the Euro, Yen and a number of other currencies in early European trading. This was due to a reappraisal for the chances of the Fed entertaining an outsized 50 bp rate hike at the upcoming FOMC meeting, which has been concomitant with a WSJ report suggesting that trade negotiations between the US and China are at a “standstill.”

US equities are mildly weaker but above earlier lows. Concern over slowing global growth is weighing on sentiment, US-China tensions have flared up again and uncertainty over Brexit is on the rise. Also, poor earnings from Netflix yesterday after the close are weighing. More earnings are due today. Morgan Stanley earnings, released this morning, topped expectations. The WSJ reported the trade talks with China had “stalled.” G7 officials highlighted the slowing in growth. The USA30 is 0.1% lower, the USA500 is down 0.02% and the USA100 has fallen 0.05%.

Currency Market

USDJPY:

USDJPY recovered some from the better than 2-week lows printed overnight, trading over 107.90 from lows of 107.62. The pairing closed under its 20-day moving average of 108.00 on Wednesday, which now becomes the next resistance level. General risk-off conditions, led by global slowing, trade war threats, and wobbly equity markets, will likely continue to support the risk-sensitive Yen, with upside USDJPY potential expected to be limited. Resistance is at 108.10-108.30. Support at 107.35 and 107.00.

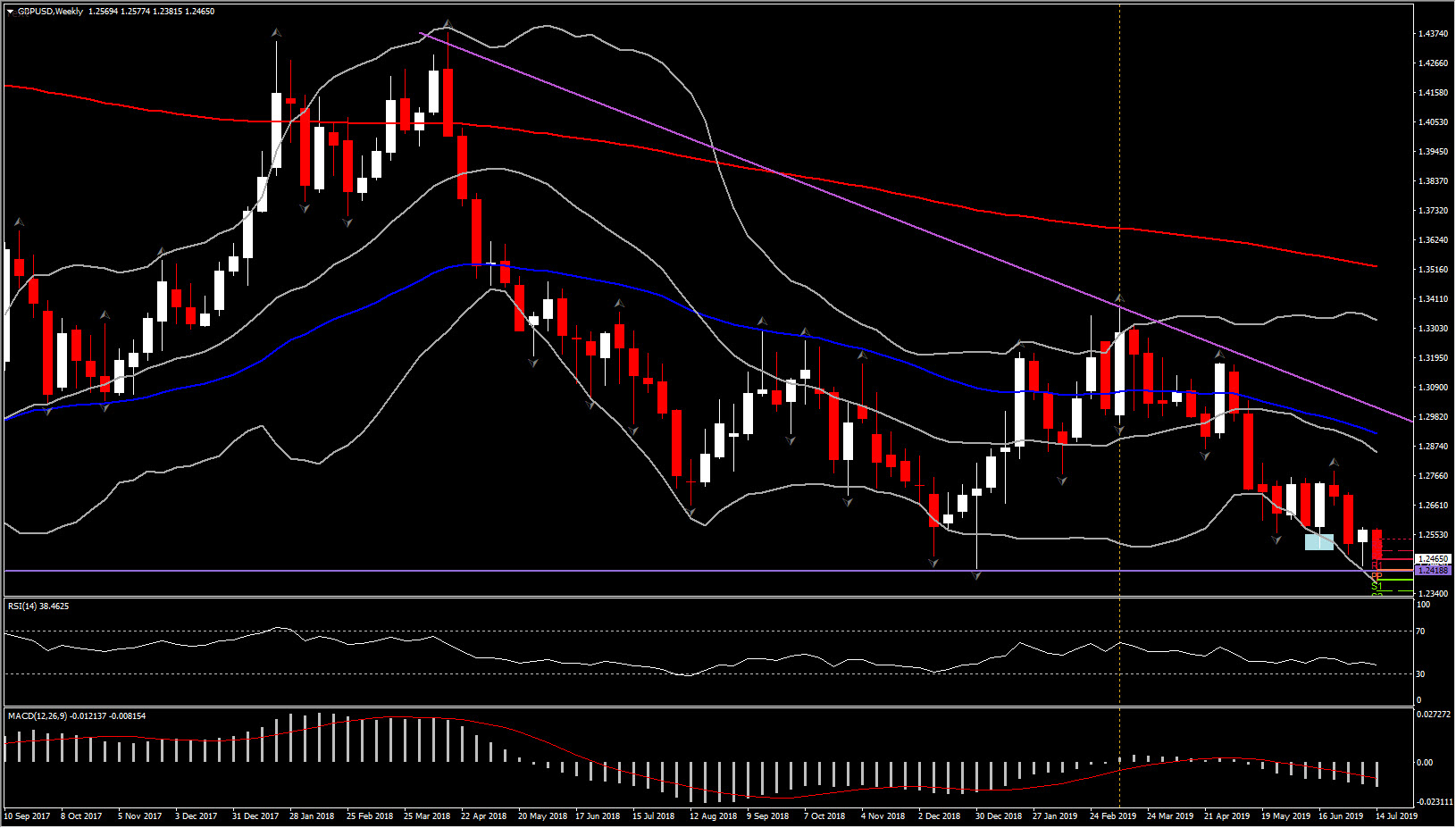

GBPUSD:

The Pound rallied, aided initially by Dollar softness before gaining versus other currencies following above-forecast UK retail sales data. UK June retail sales unexpectedly rose 1.0% y/y following a 0.6% y/y contraction in May. Cable posted a 27-month low at 1.2382 this week, extending a distinct bear trend that Pound has been enduring since early May. This comes with the deleterious economic effects of prolonged Brexit-related uncertainty having become increasingly palpable, with the UK economy now in a state of stagnation. Markets have also been factoring increased odds for a no-deal Brexit as Boris Johnson heads to a more-than-likely victory in the Conservative Party’s leadership context.

USDCAD:

USDCAD is bearishly trading the last 6 weeks, with the 9-month low seen last Friday at 1.3018. A sharp drop in oil prices, with the WTI benchmark showing a near 6% decline from week-ago levels, on signs of easing tensions between the US and Iran brought some pressure on the Canadian Dollar, which has put a floor under USDCAD, though broader declines in the US buck have been diminishing the impact of this. The USDCAD is expected to remain in this distinct bear trend that’s been unfolding since late May, with the pair having declined in five of the last six weeks. Trend resistance comes in at 1.3071-73 or higher at 200-week SMA, at 1.3115. The Fed’s course to policy easing has been driving the downward bias. As for the BoC, the central bank maintained a neutral bias last week as it delivered the widely expected no change in the 1.75% rate setting. Officials did however emphasize that the trade and geopolitical backdrops are clouding the outlook. Policy remains data driven for the BoC, which will “pay particular attention to developments in the energy sector and the impact of trade conflicts on the prospects for Canadian growth and inflation.”

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.