FX News Today

- Global stock markets have been buoyant.

- Treasuries held modest gains to start the week, unwinding Friday’s selloff on the NY Fed’s walk back, albeit in a low volume trade.

- Japanese bourses outperformed in thin trade, while markets in Hong Kong and mainland China struggled to make headway and China’s new Star market of tech companies fell back after the rally on the first day of trading yesterday.

- Stock futures in the US and Europe are moving higher, led by a 0.6% rise in the GER30 future as markets hopes for at least a dovish signal from the ECB on Thursday, with some lingering hope that the central bank will already move this week.

- A meeting between tech executives and White House officials yesterday sparked hopes of progress on Huawei, which would help to clear hurdles for fresh face to face trade talks between China and the US.

- RBNZ has reportedly been taking a fresh look into unconventional measures and hopes of easing from not just the Fed, but also the ECB helped to underpin sentiment as did an announcement from US President Trump of a bipartisan deal to suspend the borrowing limit and boost government spending levels for two years.

- Oil prices remain underpinned by ongoing tensions in the Middle East, leaving the WTI future trading at USD 56.31 per barrel.

Charts of the Day

Technician’s Corner

- EURUSD – It descended to a 1-month low at 1.1189, driven by bearish bias for a third consecutive day. Recent tops have been limited to the 1.1280 region, and ahead of the ECB meeting on Thursday, the pairing remains in sell-the-rally mode. The Bank is expected to shift to an explicit easing bias this week, with a rate cut likely coming at the September meeting. While a Fed rate cut of 25 basis points is expected at the end of July, it has been priced into the Dollar for now. Further dovish noises from the ECB should see the Euro give way on Thursday, with the first major downside target at the June low, of 1.1159.

- NZDUSD – The biggest mover out of the main pairings has been NZDUSD, which fell over 0.3% in hitting a six-day low at 0.6729. This came with the RBNZ reportedly taking a fresh look into unconventional monetary policy stimulus measures. Next Support holds at 200-day SMA at 0.6718, while Resistance is set at Wednesday’s high, at 0.6745.

Main Macro Events Today

- The announcement of the next Prime Minister of the UK – Event of the week – Original Brexit campaigner Boris Johnson remains the front runner in the race and is widely expected to be confirmed as the new Prime Minister today.

- Housing Data (USD, GMT 14:00) – A steady rate is anticipated for existing home sales in June at the firm 5.340 mln pace seen in May. The median sales price is estimated to ease to $275,000, for a y/y gain of 0.4%, down from 4.8% in May. In Q1, we saw an average sales pace of 5.207 mln. In Q2, a better 5.297 mln pace is expected.

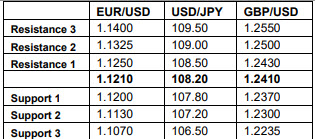

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.