All eyes will be on the ECB on Thursday with Draghi and Co set to confirm that the central bank is heading for additional easing measures as global growth slows down while global trade tensions escalate.

First quarter Eurozone GDP numbers came in stronger than expected, but were boosted by special factors including stock building ahead of the original Brexit deadline, as well as the later timing of Easter this year. Data since then suggests a marked slowdown in the second quarter and forward looking surveys leave the balance of risks firmly tilted to the downside. The above along with geopolitical trade tensions and ongoing Brexit uncertainty are weighing on confidence and adding to pressure on the ECB to ease policy again.

Some council members would likely want the central bank to cut rates now and this clearly is a “live” meeting with a non-negligible risk that the central bank lowers rates by 10 bp. However, if the ECB moves ahead of the Fed, the impact of the dovish signal would likely evaporate quickly if the central bank doesn’t follow up the Fed’s likely move at the end of July with yet another cut.

Against that background we see a somewhat greater chance, however, that the central bank will wait for September for the great reveal of a package of measures, that will likely include a rate cut as well as a mechanism to limit the impact of the negative deposit rate. This could involve setting an additional reserve “allowance” above the required reserves.

Source stories this month also suggested that the central bank is considering moving to a symmetrical inflation target rather than the current “upper limit”, which if set at 2% would create more room for temporary inflation overshoots over time, but mainly have a signaling effect at the current juncture.

In practice this may not change much as inflation has already been allowed to rise above the medium term limit but it will send a message that many believe will help to anchor inflation expectations. Officials are also looking into ways to expand the room for QE purchases and how to limit the impact of further cuts in the deposit rate, which already stands at -0.40%.

Unless things change decisively the central bank is expected to cut rates by 10 bp at the September meeting and a tiering of the deposit rate, where at least part of banks’ deposit with the ECB get preferential treatment and won’t face even higher “penalties” seems also under discussion, even if ECB studies suggest that the impact of negative rates on bank profits has been limited so far.

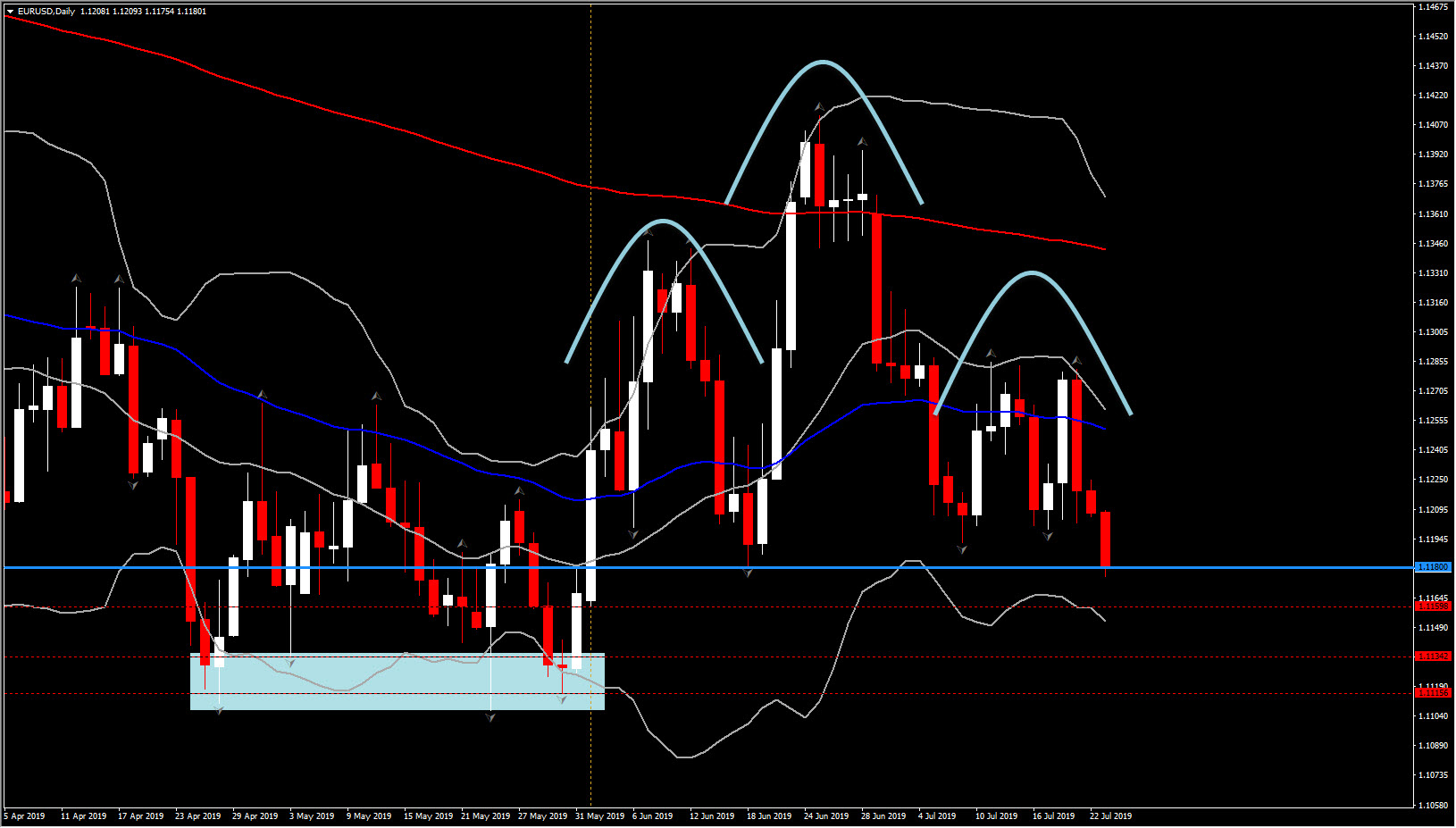

What about EURO?

Away from the economic side of things, EURUSD established a bearish outlook after coming off from a bullish June, and as it headed today a southwards move below the key Support level at 1.1180 (June 18 low and Neckline of Head and Shoulders formation pattern).

Hence, as market has retained a more circumspect view of Fed easing potential and as ECB is heading in the direction of the stimulus spigot, the move below 1.1180 today considered to be crucial, as it confirms the bearish view from technical perspective as well rather only from fundamental.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.