USDIndex, H4

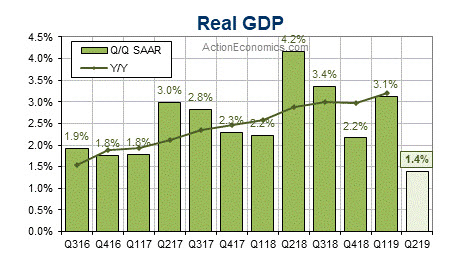

Following yesterday’s better than expected Durable Goods headline report (but weaker advanced indicators report) what can we expect from today’s US GDP numbers for Q219 ? The market consensus is a growth of 1.8% in Q2, with a sturdy 2.5% growth rate for final sales thanks to solid growth rates of 3.9% for personal consumption and 4.3% for government purchases, alongside a big $33 bln unwind of the Q1 inventory pop.

However, two key analysts, the Atlanta Fed GDPNow tool and Action Economics, both revised their expectations for 2Q GDP lower following the data yesterday. The Atlanta Fed Q2 GDPNow growth estimate was revised down to 1.333% after the data versus 1.566% on Wednesday. And they are down from 1.590% clip as of Tuesday (July 23). Nowcasts of the contributions of inventory investment and net exports to real Q2 GDP growth decreased from -0.97% and -0.50%, respectively, to -1.09% and -0.63%, respectively. Action Economics also trimmed their Q2 projection to 1.4% versus 1.8% after the weak advance indicators numbers. However, they boosted their Q3 forecast to 2.7% versus 2.5% previously.

The advance indicators report revealed big downside surprises for both exports and retail inventories, alongside small upside surprises for imports and wholesale inventories. Whereas, June US durables data beat estimates after disappointing reports in April and May, primarily due to a big 1.2% June orders rise ex-transportation that followed a small May boost to 0.5% from 0.4%, and solid June gains for equipment orders. We saw a June hit from a 14.6% defense orders drop, and a big downward May revision for transportation orders that exacerbated the May-June orders gyration, with weakness in transportation related to Boeing. Shipments rose by a solid 1.4% in June, while inventories rose by a lean 0.3%.

USD index has held its bid for the week, rising from lows last Friday (July 19) around 96.50 to breach 97.00 on Tuesday (July 23) and move north of 97.50 on last night’s close (July 25), following the relative volatility of the ECB Interest Rate Announcement and Press Conference.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.