The FOMC cut rates a quarter point, as was well telegraphed by the Fed over the last month, and as was fully anticipated by the markets. But the policy statement and Chair Powell’s press conference didn’t deliver the dovish policy path that had been priced in. Indeed, the presser was highlighted by Powell’s comments that this is a “mid-cycle” action and “not the beginning of a lengthy cutting cycle.” Though he walked that back a bit, it nevertheless disappointed bond and stock bulls alike, while the Dollar was the beneficiary. Of note, there were two dissents against the easing from the two hawks George and Rosengren.

Chair Powell’s comment on the rate cutting cycle was initially a casual, almost off-handed remark. “The Committee is thinking of today’s action as a mid-cycle adjustment to policy,” he said, designed to provide support for the economy, ensure against downside risks, and support inflation.

But the markets jumped on it to mean one-and-done in terms of easings. Short rates surged while the USA30 plunged. He walked that remark back somewhat, stating “I didn’t say it’s just one rate cut.” And he added this is not “the beginning of a long series of rate cuts. When you think of rate cutting cycles they go on for a long time.” The Committee is not seeing that, he added, and he indicated that the Fed might still ease again.

This mid-cycle adjustment has precedent, and in fact was seen 24 years ago in 1995 when the FOMC cut rates on July 6 after a string of rate hikes through the year. In that case, it was just a one-and-done cut, as the FOMC’s next policy move was a tightening one year later on July 3.

The Fed’s policy statement was in line with expectations and did not offer much new. To rationalize the move the Fed said it lowered rates “In light of the implications of global developments for the economic outlook as well as muted inflation pressures.” That was because the economy is actually doing well. The statement indicated that economic activity has been “rising at a moderate rate,” while job gains have been “solid.” Household spending has “picked up some,” though growth in business spending has been “soft.”

For forward guidance, the Committee “will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.”

On the other hand, the Fed did decide to end the balance sheet run-off a month early on August 1. The markets should eventually be appeased by the early end to quantitative tightening, and Fed’s dovish shift over the last six months.

Meanwhile, there were two dissents, with hawks George and Rosengren who preferred an unchanged rate stance. They are two of the most hawkish on the Committee. There haven’t been two dissents since December 2017, under Chair Yellen’s watch, and they were by two doves, Evans and Kashkari, voting against a hike.

Bonds and stocks recovered into the close, but were still reflecting disappointment.

The 2-year yield finished 2 basis points cheaper at 1.87% versus the knee-jerk high at 1.96%. The 10-year outperformed and closed 4 basis points richer at 2.01%, after hitting 2.07%, with the 2s-10s curve nearly 7 basis points flatter at 18.8 bp.

Wall Street closed with losses of over 1%, hurt by the FOMC’s less than aggressive easing tone, earnings, worries over the trade talks with China, and the Fed’s stress on the spillover from weakness overseas.

US DOLLAR

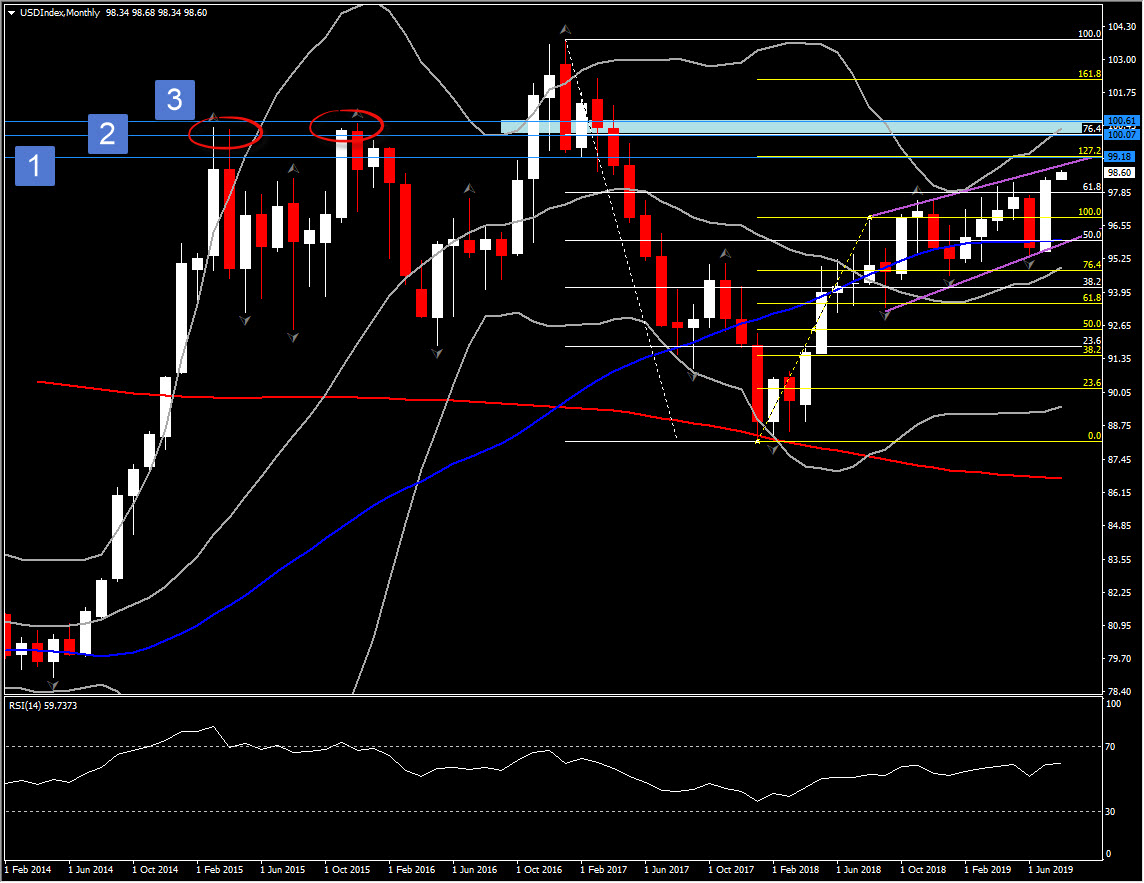

So far Dollar has extended post-Fed gains during the early part of the Asia session, with the narrow trade-weighted USDIndex gaining by a cumulative 0.9% in printing a high at 98.92, which is the highest level seen since May 2017.

EURUSD concurrently fell to a fresh 27-month low at 1.1034 while USDJPY lifted to a two-month peak at 109.32. Elsewhere, the Brexit-afflicted Pound has managed to hold above recent trend lows versus the Euro, Yen and other currencies, with GBPUSD drifting to 30-month low, at 1.2101.

Interestingly, the USDIndex closed the month 3% higher, with a monthly change that hasn’t been seen since 2016 adding further positive bias to the asset in the medium to long term outlook. The huge bullish candle decisively broke the 98.00 barrier and the 61.8% Fib. retracement level set since the decline from the 103.80 area (January 2017). Hence the nearly full body bullish monthly candle, along with the formation of a descending candle since September 2018, and the positive configuration of momentum indicators, suggest that the move is likely to continue to the upside in the medium to long term. Momentum indicators from Daily up to monthly timeframe are extending higher with MACD presenting bullish cross. Immediate Resistance and Support level are at 99.20 and 98.30 respectively. In the medium term though the medium term pivot band is at the 100.00-100.60 area.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.