FX News Today

- RBNZ surprises markets with hefty 50 bps cut; official rate now at 1.00%.

- India’s RBI cut rates by 35 bps – more than expected; repo rate at 5.4%.

- Decisive action from central banks in New Zealand and India also fueled fresh speculation of deep cuts from the likes of Fed and ECB.

- New Zealand’s 10-year rate led a broad slide in yields across Asia.

- The RBNZ surprised markets with a hefty 50 bp cut that left the official cash rate at a record low of 1.00% and will spark fresh speculation of deep cuts world-wide.

- The NZD dropped sharply as a result and AUD was also dragged lower as the 10-year rate dropped -8.3 bp, with traders expecting the RBA to follow.

- Still, pressure eased somewhat in stock markets, after China took steps to steady the Yuan yesterday.

- JPN225 is down -0.27%.

- US futures are in the red after a positive close on Wall Street yesterday and the WTI future is trading at just USD 53.66 per barrel.

- In Europe, German production numbers at the start of the session underpinned easing hopes.

- German industrial production slumped -1.5% m/m in June, with the May reading revised down to just 0.1% m/m.

- The German curve has already settled below zero and pressure on Draghi to not just cut rates but restart asset purchases is mounting.

Charts of the Day

Technician’s Corner

- NZDUSD: The New Zealand Dollar over 2% in hitting its lowest level against the US Dollar since January 2016, at 0.6377, and trading at near seven-year lows in the case against the Yen. This followed a more aggressive than expected 50 bp rate cut by the RBNZ to an all-time low 1.00%, which was pinned on flagging growth conditions as a consequence of simmering trade tensions and a global economic slowdown.

- AUDUSD fell in sympathy, with the RBA, after cutting rates in June and July, having signalled yesterday that more rate cuts could be in the pipeline. The pair smashed through the early January flash-crash low on route to printing a 10-year nadir at 0.6677. AUDJPY also dove into 10-year low territory.

- USDJPY: The Yen lifted against the Dollar and Euro, though remained below highs seen earlier in the week. USDJPY posted a low at 105.93, extending the retreat from yesterday’s 107.09 high.

- EURUSD continued to orbit the 1.1200 level. Sterling came back under pressure after a positional-driven rally earlier in the week. Cable nudged back under 1.2150 after failing to sustain gains above 1.2200, while EURGBP lifted back above 0.9200, drawing back in on the 24-month high at 0.9249.

Main Macro Events Today

- Ivey PMI (CAD, GMT 14:00) – A survey of purchasing managers, the Index provides an overview of the state of business conditions in the country. Canada’s July Ivey PMI is expected to improve 2.6 points to 55.00 after the decline seen in June. The data is supportive of the steady policy story, as the economy returns to potential growth contrasts with an outlook “clouded by persistent trade tensions.”

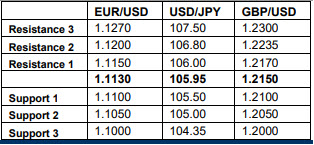

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.