FX News Today

- German 2Q GDP -0.1% vs -0.1% q/q expected. The headline meets expectations and confirms that the German economy shrank in Q2.

- Treasury yields fell back -2.7 bp to 1.676% overnight, as weak data out of China revived growth concerns. JGB yields still moved up 2.1 bp to -0.277%, as Asian stocks moved higher following gains on Wall Street after news yesterday that the US will delay the new tariffs on Chinese imports until December – at least for some products that are high on holiday shopping lists, after a “productive” call with China.

- Meanwhile China said it is sticking to September trade talks with the US. Weaker than expected industrial production numbers and retail sales out of China added to signs of slowing growth and revived fears of a global recession, but CSI 300 and Shanghai Comp still managed to hang on to gains of 0.7% and the Hang Seng is up 0.56%, after being hit by ongoing anti-government protests on Tuesday. The Nikkei is up 1.0%.

- The AUD slipped with the Yuan following China’s data misses and is little changed at 0.06%, while U.S. futures are in the red.

- Market sentiment remains fragile as data continue to signal downside risks to growth. USOil is trading at $56.42 per barrel and Gold holds the $1500.00 handle

Charts of the Day

Technician’s Corner

- EURUSD: Fell to session lows of 1.1170 after the trade news, where U.S./China negotiations are set to resume in two-weeks, and the imposition of additional tariffs were pushed back to December 15 from September 1. The pairing recovered to 1.1227 highs. Firmed up Treasury yields and a sharp Wall Street helped the pairing lower initially, though given the on-again, off-again trade talks, traders may take yesterday’s news with a grain of salt. An errant Trump tweet could quickly undo the apparent progress made today without warning. Bigger picture, EURUSD is liable to remain anchored to the 1.1200 level, as Italy’s political crisis, and Brexit, along with Europe’s fading growth outlook will limit the Euro’s rise, especially given the ECB is set to ease policy in September as well. EURUSD currently trades down at 1.1170 again.

Main Macro Events Today

- Industrial Production and Retail Sales (CNY, GMT 02:00) – The Chinese Industrial Production growth decreased at 4.8% y/y in July from 6.3% y/y last month and worse than expectations of a 5.8% reading. Retail Sales figures also missed expectations (8.6%) when they came in at 7.6% down from 9.8% in June.

- Gross Domestic Product (EUR, GMT 06:00-09:00) – German Preliminary Q2 results stood at 0.4% q/q. Eurozone prelim. Q2 GDP growth expected to be confirmed at 0.2% q/q and 1.1% y/y.

- Consumer Price Index (GBP, GMT 08:30) – The UK July CPI expected to meet once again the expectations at 2.0% y/y, which was unchanged from the May rate. Core inflation should remain to 1.8% y/y. The data fits BoE projections, and shows that perky wage inflation hasn’t translated into higher headline rates yet.

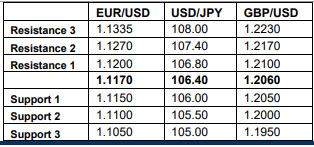

Support and Resistance levels

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.