USA500, Daily

Last week there were signs of life in the equities market – August has certainly been volatile with relatively high volumes and some key technical areas tested.

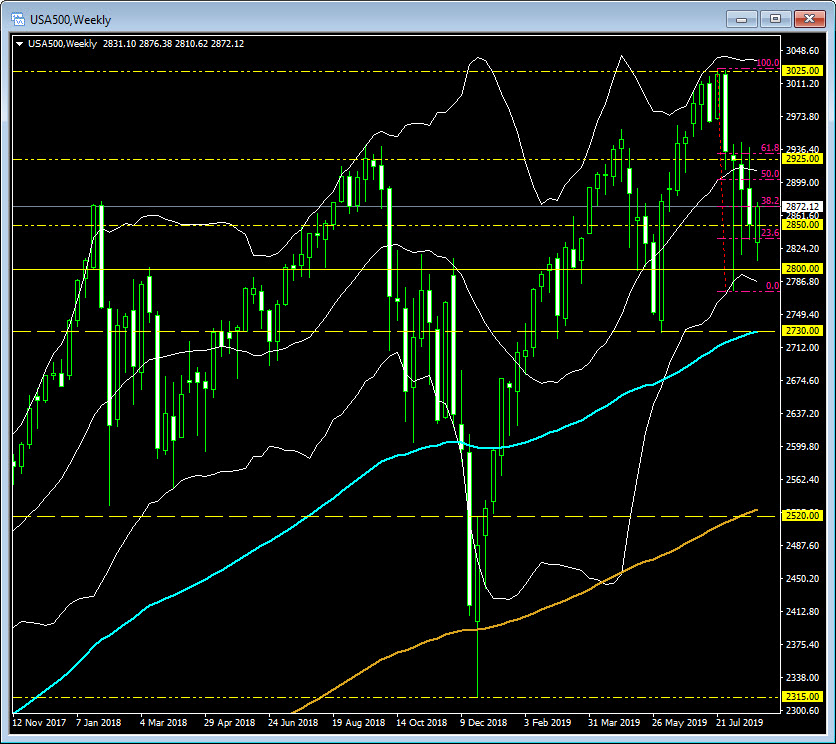

Tuesday (August 20) the USA500 – the world’s most important and significant equity market closed over the key 20-day simple moving average for the first time in 16 trading days at 2924.43, having rallied from the psychological 2900 level.

Technically, the 200-day moving average sits as support at 2850, 2800 is a key psychological support (and 100-day moving average), with the summer & spring lows (June 3 & March 8 respectively), at 2730. Additionally, the close over the 20 SMA also coincided with the 61.8 Fibonacci retracement level of the move down from the all-time high from mid-July over 3025 to the recent August 6 low of 2775.

The market slump on Friday (August 23), following the ramping up of the tit-for-tat tariff war between China and the USA, tested these key levels again. The 2935 resistance level from earlier in the week was rejected and the USA500 completed the fourth consecutive week of losses. In the higher time frames, the 2730 low is the weekly 100-moving average, with the 200-moving average sitting at 2520 and hiatus low of Christmas week 2018 at 2315.

Today, the USA500 continued lower in the Asian session testing S1 at 2811, before recovering significantly on news that President Trump said that China called US negotiators and that “we’re going to start talking very seriously with China” and that “I think we will make a deal”. The market currently trades at 2870 which represents the new daily pivot point and the 38.2 Fibonacci level. The Crossing EMA Strategy (H1) triggered long at 08:00 GMT (2867) with T1 at 2882, T2 at 2902 and a SL at 2830. This follows the 57 point move down from Friday.

It could be another key week for the USA500, with the US Durable goods numbers today, Consumer confidence tomorrow and the key Q2 GDP first revisions on Thursday. However, as we approach the notoriously volatile September-October time frames the key underlying sentiment, driven by the US-China trade war and the US bond market rally, remains both fragile and volatile.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.