FX News Today

- Bunds cautious after hawkish comments from Nowotny, who said the ECB should be prepared to disappoint markets sometimes.

- BTPs are rallying after confirmation that acting PM Conte will get a second chance, this time backed by a coalition of PD and Five Star Movement.

- Stock markets remained cautious amid the lack of firm news on the US-Sino trade front and waiting to see what impact the latest tariffs will have and what global central banks are doing, with further easing measures expected to be in the pipeline as trade tensions hit the world growth outlook.

- US Secretary Steven Mnuchin said US trade officials expect Chinese negotiators to visit Washington, but would confirm whether a previously planned meeting in September will take place.

- European and US futures are in the red: In Europe Brexit jitters and the increased risk of a no-deal scenario cloud over the outlook after PM Johnson moved to suspend parliament for a large part of the remaining time until the October 31 Brexit date.

- Oil prices slipped on growth worries, despite signs that OPEC supply cuts are curtailing US inventories.

Charts of the Day

Technician’s Corner

- USDJPY recovered from opening lows of 105.65, managing to rally to 105.95 after Wall Street turned higher. Treasury yields remain lower however, acting to limit the pairings upside potential. Bigger picture, the risk-sensitive USD-JPY may still have room to run lower, as flare ups in the U.S./China trade war are likely to continue. There is little sign of progress, or even talks under way, as additional tariffs on Chinese goods are set to kick in on Sunday. Monday’s 33-month low of 104.45 is the next downside target.

- USOIL rallied to $56.70 from $56.35 following the EIA inventory data which showed a 10.0 mln bbl fall in crude stocks. The street had been expecting a 2.0 mln bbl decrease, though the API reported an 11.1 mln bbl draw after the close on Tuesday. Meanwhile, gasoline supplies, seen down 0.5 mln bbls actually fell 2.1 bbls, while distillate stocks were down 2.1 mln bbls, versus expectations for a 1.5 mln bbl fall.

Main Macro Events Today

- Harmonized Index of Consumer Prices (EUR, GMT 12:00) – The German HICP inflation has jumped to 1.3% y/y for August after it was revised down to 1.1% y/y in July.

- US Gross Domestic Product (USD, GMT 12:30) – The preliminary Q2 GDP growth is expected to trim to 1.9% from 2.1%, with a $6 bln hike in consumption that accompanies a $2 bln boost for nonresidential investment. A downward revision is expected of -$5 bln for inventories, -$4 bln for exports, -$3 bln for imports, -$8 bln revision for public construction, -$2 bln residential investment, and -$1 bln for equipment spending.

- Tokyo CPI and Production Data (JPY, GMT 23:30) – The country’s main leading indicator of inflation is expected to have slip at 0.7% y/y core in August, and at 0.8% y/y ex Fresh Food. Industrial Production should post a 0.3% grow m/m in July, compared to -3.3% in June.

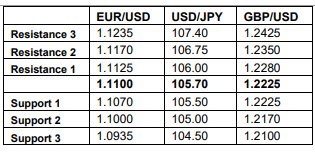

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.