A 10%-plus rebound in crude prices catalyzed gains in oil-correlating currencies, including the Canadian Dollar and Norwegian krona, and other commodity currencies, while helping give stock markets a lift after a sputtering session in Asia. The wake of ugly 6.6 mln surge in US jobless claims, which was about double the consensus forecast, weighed on global markets. US equities reversed lower as risk appetite eroded again, taking back earlier gains, while Aussie for example has more than given up intraday gains, with AUDUSD presently pushing on lows at 0.6019, down just over a big figure from the intraday high that was seen during the Sydney session.

The massive gain in initial claims, which followed a similarly hefty rise the previous week, was well anticipated but provided a timely reminder of what is to come.

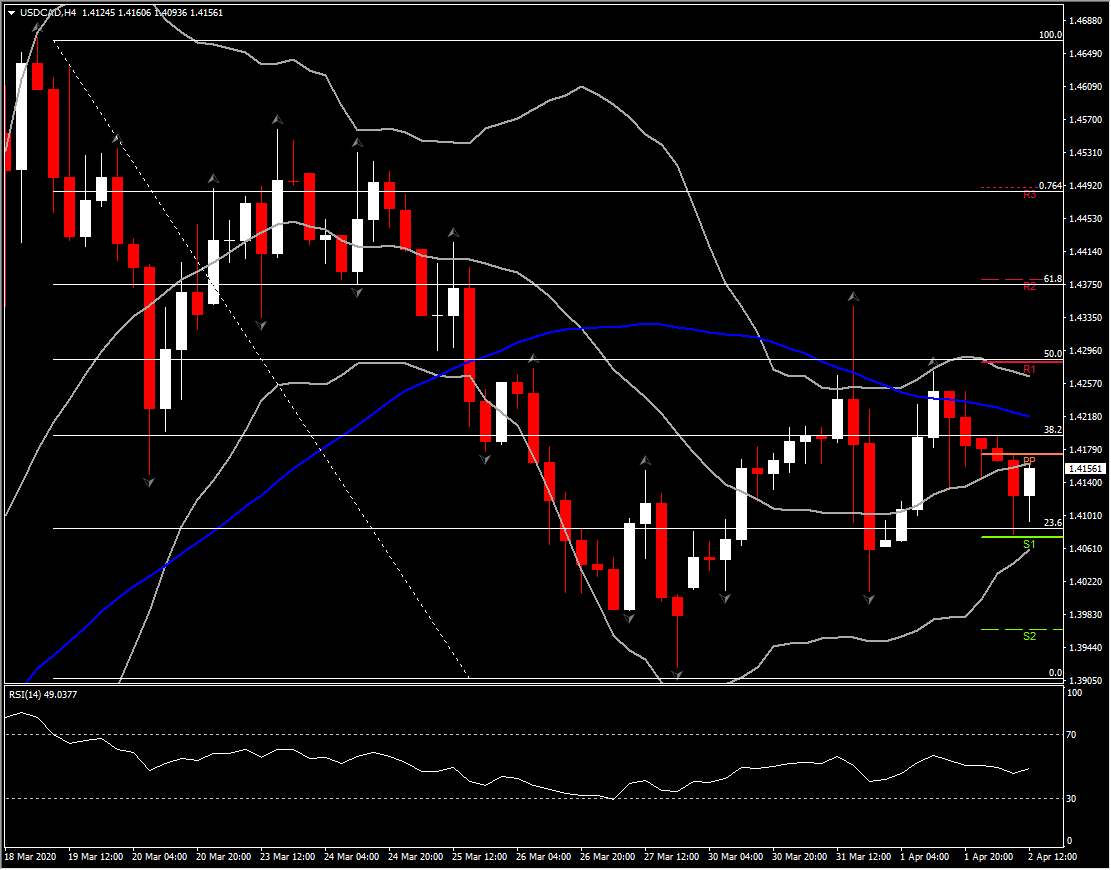

USDCAD has dropped by over 0.6%, driven by a bid for the Canadian Dollar amid a 10%-plus oil price surge. The pair posted a low at 1.4079, though has so far remained above its Wednesday low at 1.4060. A Bloomberg report, citing sources with inside knowledge, said that China is moving forward with plans to buy oil for its emergency reserves. Beijing is reportedly aiming to build up a crude stockpile that would cover 90 days of net imports with the possibility of expanding this to 180 days. China is the world’s biggest oil importer and is taking advantage of the 60%-odd collapse in oil prices. USOIL prices posted a 6-day high at $22.55, but still remain down by just over 65% from the highs seen in early January. This level of price decline in Canada’s principal export, while it sustains, marks a significant deterioration in the Canadian economy’s terms of trade. Assuming that China’s buying spree won’t close this gap substantially, given the glut of crude flooding the market, and given that demand will remain weak for a historically protracted amount of time, CAD should remain apt to underperformance. In the medium term, USDCAD could retest its recent 17-year high at 1.4669.

Both the AUDUSD and NZDUSD rallied, although both remained within their respective Wednesday ranges against the US Dollar.

USDJPY and most yen crosses, in particular those involving a commodity currency, have gained concomitantly with the improvement in risk appetite, which saw the yen’s safe haven premium unwind some.

GBP is again ranking among the currency outperformers today, gaining over 0.7% versus the Dollar and by over 0.8% against both the Euro and Yen on the day so far. Market narratives have been pointing to the impact of the Fed’s launching of a new “FIMA” facility (announced Tuesday) , which will start on April 6 and allow foreign central banks to obtain Dollars without selling Treasuries. This will run alongside the swap lines created with 14 central banks, and the two should ease strains in global dollar funding. This is seen as a particular positive for the Pound, given the UK’s recently proven vulnerability to global liquidity shortages, with its large financial sector and dependence on foreign investment inflows (equivalent to about 4% of GDP) to finance its large current account deficit.

The Pound had underperformed even commodity currencies during the worst of the recent global liquidity crunch, which ran from about March 10th through to March 19th, before measures by the Fed and other central banks provided a mitigating impact. Sterling lost about 10% of its value in trade-weighted terms over this period, and tumbled by 12% versus the Dollar, hitting a 35-year low, and an 11-year low against the Euro. The worst now looks to be over for the Pound, especially with markets starting to bet that the UK will ask the EU for an extension of its post-Brexit transition membership of the Union’s customs union and single market. Neither the UK nor EU has the resources to conduct detailed trade negotiations under the prevailing circumstance of the coronavirus crisis. This is seen as Sterling positive as it will avoid the possibility of the UK leaving the transition period and shifting a big chunk of its trade onto less favourable WTO trade terms.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.