After BoJ and FED, the next key policy meeting of the week is the ECB tomorrow. However, let’s make a small recap where Europe is standing right now.

As reported last week, European countries are slowly starting to ease virus-restrictions and while economies will have to adjust to a new normal there seems to be some light at the end of the tunnel. In the UK, PM Johnson has returned to Westminster after his recovery from Covid-19 and while he, as well as other European leaders, urged caution there is hope that we may have seen the worst of the death tolls. EU leaders meanwhile agreed on a large recovery fund, and even though there are difficult negotiations over the details ahead, that will help to keep hopes of a rebound in 2021 alive.

EU leaders in principle agreed on a huge recovery fund worth 1 to 1.5 trillion Euros to finance stimulus measures designed to boost the recovery after the lock downs have ended. As usual the devil lies in the details though, with no agreement yet on how the package will look like. The Commission pledged to come up with detailed proposals, although the way things are going, it seems there will be a focus on low interest loans, rather than the budget transfers countries like Spain and Italy have been hoping for. The other obstacle to a quick deal is the question of how monies will be disbursed with a new fault line opening up between the southern European countries, which have been hardest hit by the crisis, and eastern European countries, such as Poland and Hungary, which so far have been the main beneficiaries of the EU’s regional funds.

Against that background the ECB eased collateral rules again last week, and thus “virus-proof” liquidity provision in the Eurozone.

The ECB is now expected to hold rates steady at the April council meeting on Thursday. Aid measures are set to drive up deficit and debt levels sharply and the ECB is focused on keeping spreads in, with the PEPP allowing the front loading of asset purchases. Some expect the PEPP program to be extended to push out the need to balance the book and distribute asset holdings according to the capital key, but while that clearly is a possibility, we would expect the central bank to keep that option for later, if necessary. Meanwhile collateral rules have been loosened again, with the ECB committing to “grandfathering” fallen angels that lost their investment grade status due to the crisis.

The fact that Italy escaped a ratings downgrade last week has helped the ECB in its quest to keep spreads low, although like it already did with Greece, the central bank would also overlook a low Italian credit rating in its crisis measures, if it proved necessary.

This week however, the Eurozone spreads have widened, as the core rallied, while Italian BTPs sold off after Fitch lowered the country’s credit rating to BBB- with a stable outlook. However, the ECB’s bond buying program is expected to keep Italy afloat even if there are further downgrades.

The policy meeting is not expected to impart much directional impact on EURUSD, as both the FED and ECB are already pursuing aggressive loose monetary policies and with neither expected to alter prevailing settings (other than perhaps an extension of the new emergency bond buying program in the case of the ECB) while repeating the “do what it takes” guidance.

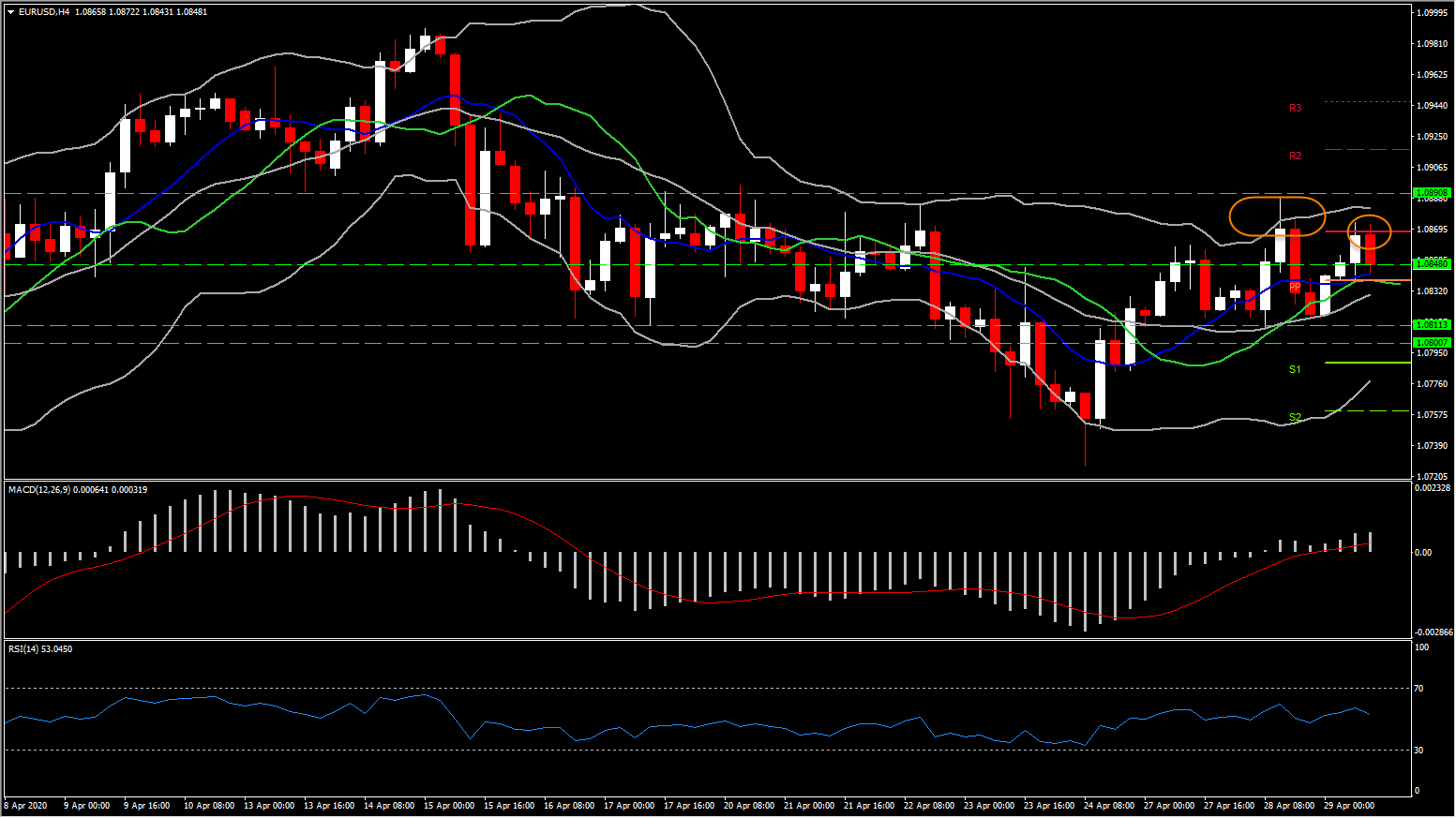

So far today, EURUSD initially lifted over 50 pips to a high of 1.0868, but turned to 1.0848 on the anticipation of Fed announcement today. It has remained comfortably below yesterday’s 9-day high at 1.0890. This price action has come with the narrow trade-weighted USDIndex ebbing to a low at 99.54 after closing yesterday in New York at 99.87.

The gains that EURUSD has seen this week have put the pair a step back toward the halfway mark of the volatile range that was seen during the height of global market panic in March, which was marked by 1.0637 on the downside and 1.1494 on the upside.

The sharp narrowing in the Dollar’s yield advantage that was seen in March, when the Fed reversed all rate hikes it made from late 2015 through to last year, came to a pause in early April, with Treasury/Bund yield differentials having since been holding steady. That said, EURUSD looks likely to lack a clear directional bias, though risks seem to be skewed to the downside given the political stresses within the EU.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.