AUDUSD & AUDJPY, H1

More of the same today, with the Dollar and Yen weakening while commodity currencies lead the outperforming pack as stocks and oil prices, and other industrial commodities, continued to rally. A risk-on cocktail of reopening global economies and expectations for further stimulus measures have been underpinning, which are for now offsetting concerns about US-China tensions and the potentially economically disruptive social order disturbances across America.

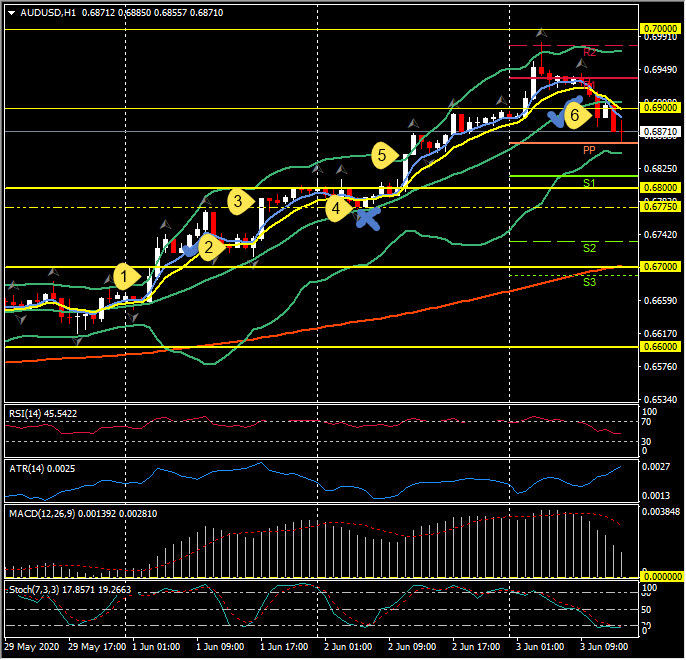

The narrow trade-weighted USDIndex fell a further 0.3% in printing a low at 97.25, the lowest level seen since March 12th. EURUSD concomitantly lifted to a high at 1.1227, which is its loftiest level since March 16th. Cable posted a fresh one-month peak at 1.2625. Yen underperformance floated USDJPY to a new near-two-month peak at 108.85, despite concurrent dollar losses against other currencies. AUDJPY continued to be the outperforming cross out of the main dollar pairings and cross rates. The cross gained over 0.7% in pegging a new high at 75.76, its best level since mid January. AUDUSD posted a new high for 2020, at 0.6983, a level last seen on December 29th last year. USDCAD etched out a new near-three-month low at 1.3478.

Front-month WTI crude prices hit a new three-month peak at $38.17, whilst Gold dropped below the $1725 daily support level to test $1713. The MSCI Asia-Pacific equity index rallied to its best levels since March 9th and the pan-Europe STOXX 600 rallied 1.5%, while the 30-year US T-bond yield is at its highest since mid March.

Among today’s data releases so far, investors overlooked negative GDP figures out of Australia, with April building approvals and final May PMI data painting a picture of a rebounding economy. Final China services and composite PMIs for May, meanwhile, signalled a sharp rebound, as did final May PMI readings out of Europe. As a Reuters article highlights, high-frequency data, such as restaurant bookings and mobility data, are showing significant improvement in many key global economies from the nadir of April. The final May UK composite PMI was revised fractionally higher, to a headline reading of 30.0, up from the initial estimate of 29.9. This marked a pronounced rebound from the April record low of 13.8, though still signalled an economy deep in contraction. The PMI surveys highlighted steep declines in private sector employment in the manufacturing and services sectors, which fell in May at the second sharpest rate since the data series began in 1998. The story was no different across the English Channel, as Eurozone services PMI revised up to 30.5 in the final reading for May, from 28.7 reported initially and versus 12.0 in the previous month. This helped to lift the composite to 31.9, versus 30.5 in the preliminary report and compared to 13.6 in April. A stronger than expected rebound then that confirms that confidence bottomed out in April, although with indices still pointing to broad based contraction across both manufacturing and services sectors.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.