Risk seemed to bounce back yesterday, but investors turned cautious again as the FOMC meeting comes into view. Data out of China, including industrial production and retail sales, beat expectations and the PBOC injected 600 bln yuan via a 1 year MLF, which helped China bourses to move higher. Hang Seng and CSI 300 meanwhile are up 0.5% and 0.7%, also helped by comments out of China that a vaccine could be taken in November.

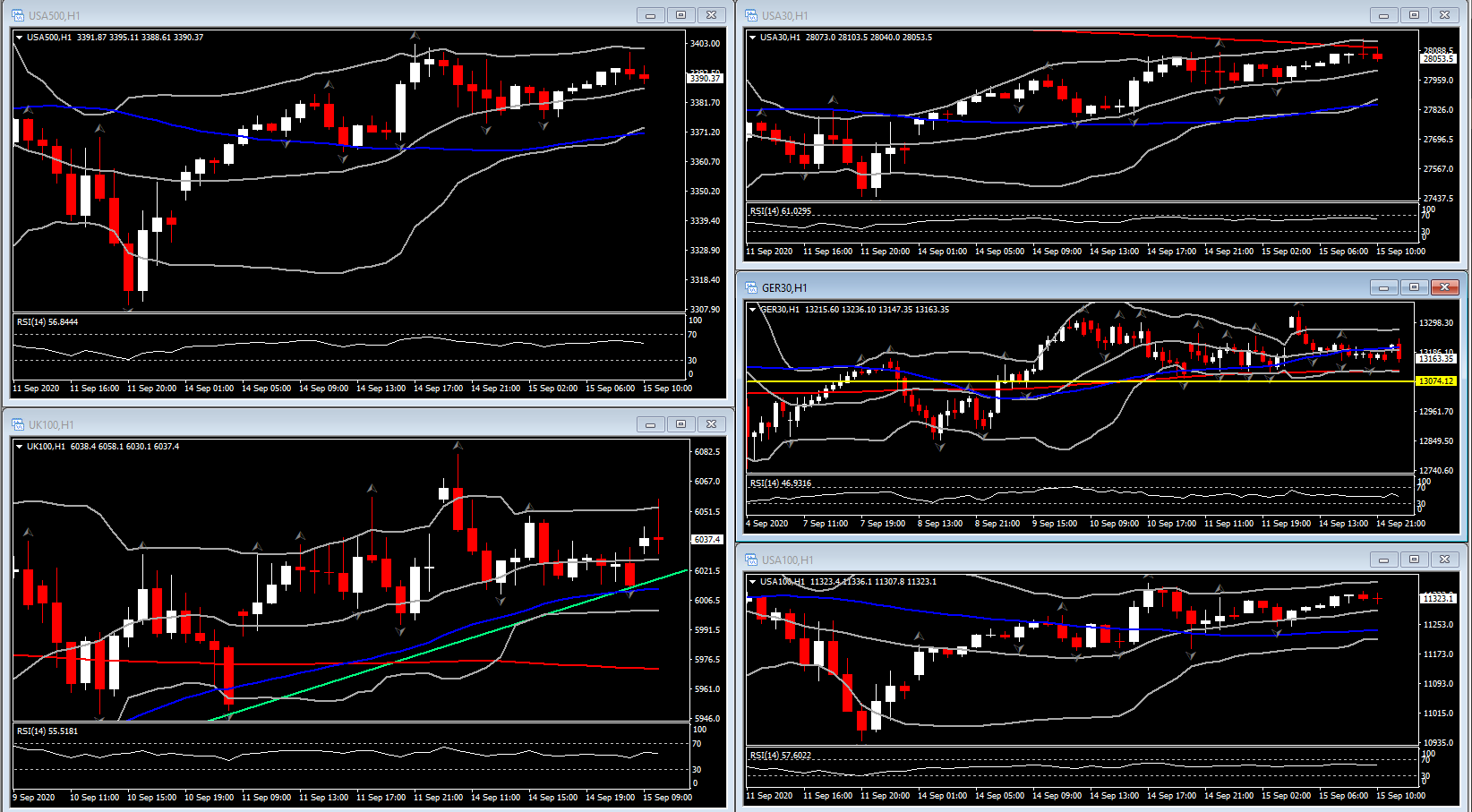

The main US equity indexes closed on Wall Street yesterday with gains of over 1%, and USA500 mini is up 0.5% in overnight trading. Positive news on the Covid-19 vaccine and treatment front, news of some mega mergers, along with above-forecast data out of China, have collectively floated investor spirits.

Elsewhere Asian markets traded mixed, however Eurozone peripheral markets are mostly outperforming slightly, after ECB officials including President Lagarde strengthened the central bank’s message on the EUR since last week’s policy announcement. The message that if the exchange rate threatens to undermine the inflation projection, the ECB will act, is getting clearer and has already seen peripheral markets rallying yesterday.

GER30 and UK100 futures are both up 0.1% at the moment, underperforming versus US futures, which are up around 0.5% after a mixed session in Asia overnight. The GER30 and UK100are hardly changed as the focus turns to the FOMC meeting, which starts today and its policy statement and new Summary of Economic Projections (SEP) on Wednesday.

Chair Powell largely pre-empted this meeting in terms of policy with his Jackson Hole announcement of the FOMC’s new strategies where it will pursue an average inflation target and monitor any shortfall in employment. An upward revision is seen in the Fed’s GDP and inflation outlooks, and a downward bump to unemployment, as a consequence of its regime change. The upward revisions to growth may give the US Dollar a lift, though the lower-for-longer strategy on interest rates may offset.

The BoE, which announces its policy decision on Thursday, is also expected to keep overall settings on hold, against the background of Brexit and virus jitters. PM Johnson managed to get his controversial Internal Market Bill through the first reading in parliament yesterday and that leaves the risk of a no-deal scenario firmly on the table.

In FX markets

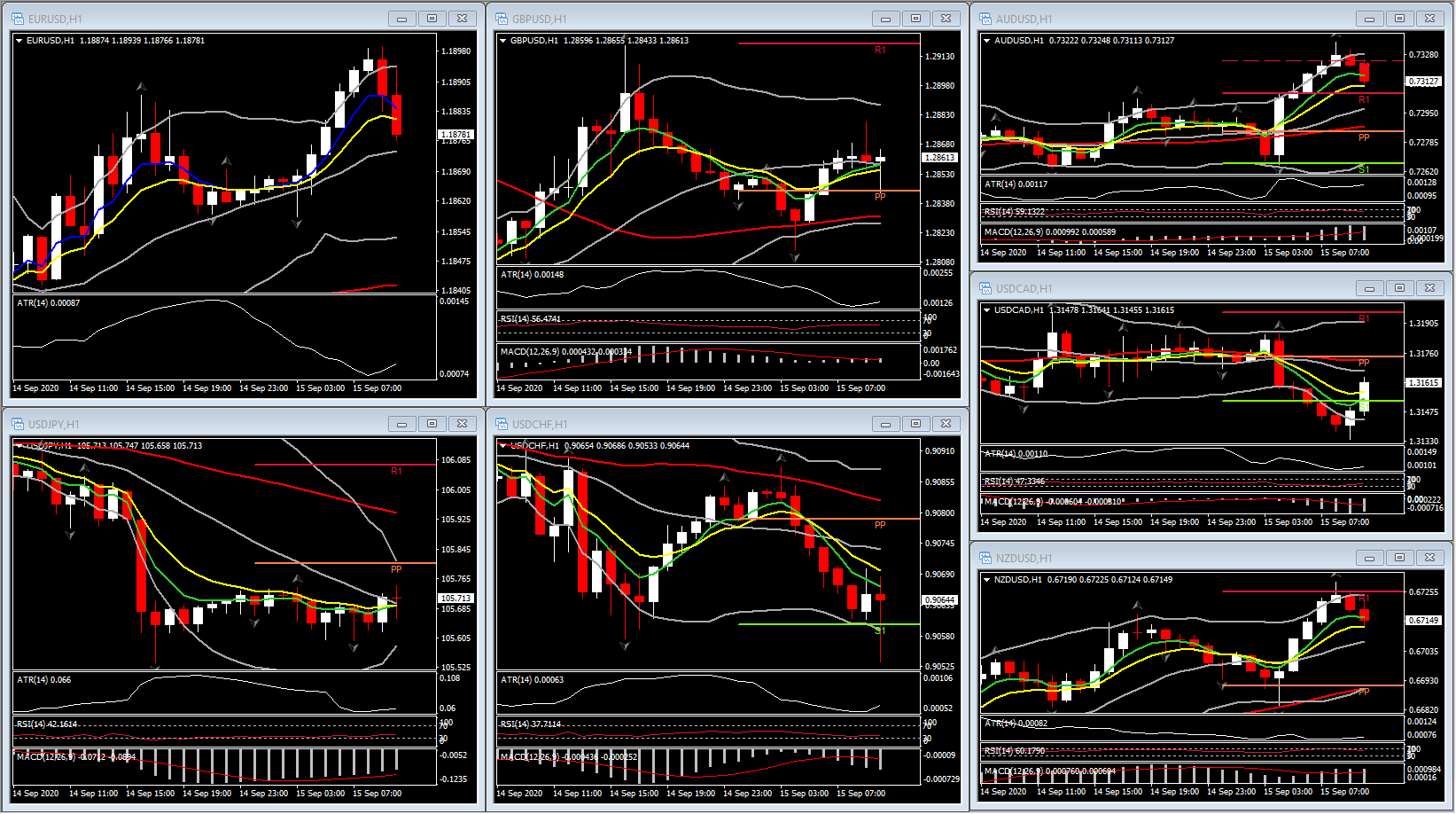

The USD and JPY softened against their peers amid a background theme of mostly higher stock markets. Among currencies, the USDIndex printed a 5-day low at 92.84. Sterling remained heavy, though remained above above recent lows. The UK government’s controversial Internal Markets Bill was passed in the House of Commons, and will now go the House of Lords.

As for the Euro, attention will be on the latest ZEW investor sentiment survey, which is the first major confidence data of September. A slight decline in the expectations reading is expected to 71.0 from 71.5. Nothing yet to shake the ECB’s baseline scenario, with Brexit and virus/casedemic developments the key factors that policymakers will be watching closely. EURUSD concurrently pegged a 5-day high at 1.1900. USDJPY flatlined in the mid-to-upper 105.00s (PP at 105.80).

AUDUSD rallied by over 0.5% to a 12-day high at 0.7336 but retreated to 0.7310. The release of the latest RBA minutes, although stating “a lower exchange rate would provide more assistance to the Australian economy,” sparked initial Aussie Dollar buying as markets deemed the minutes to be less dovish in overall tone than had been anticipated. The Aussie was subsequently given a further lift by above forecast Chinese data. .

USDCAD has been playing a narrow range in the mid 1.3100s, below the 3-week high that was seen last Wednesday at 1.3261. Oil prices have stabilized in recent days following a near 20% tumble, which has arrested the recent decent in oil-correlating currencies, such as the Canadian Dollar. The flattening out in the recovery pace of the global economy, juxtaposed to large global crude stockpiles and uncertainty about Chinese demand (which has been importing crude in record quantities in recent months, but may now be ready to slow this process down), caused the rotation lower in oil prices.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.