EURUSD, H1

The Dollar fell back concomitantly with rallying European stock markets and US index futures, which was likely a repositioning dynamic after declining over the last two weeks.

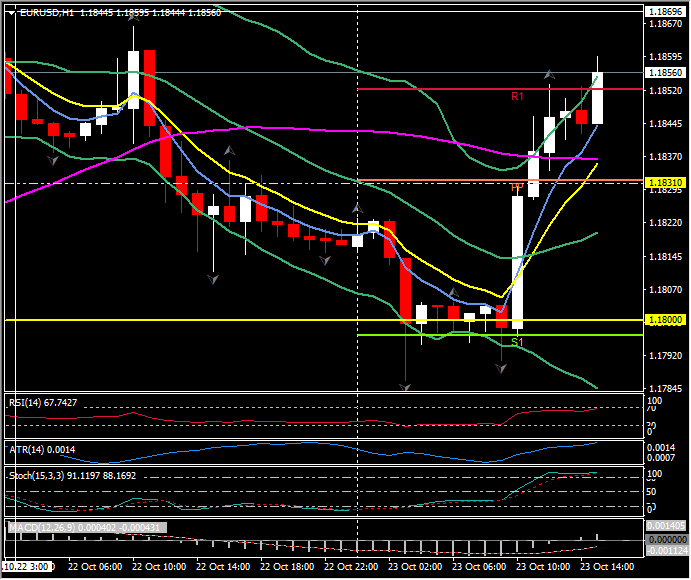

EURUSD rebounded quite strongly, rising back above 1.1850 from a three-day low at 1.1787. Preliminary October PMI data in the services and composite readings out of the Eurozone and UK undershot the median forecast of economists, but didn’t impact the Euro or Sterling. Technically, the H1 chart has moved over the 50-hour moving average (1.1835) to test R1 at 1.1852; above here is Wednesday’s high and R2 at 1.1885. Today’s pivot point is next support at 1.1830, below the 50-hour moving average. The MACD histogram has broken the zero line and the signal is starting to rise, although still south of the zero line, RSI is positive and trades at 64.50, Stochastics are moving into the OB zone.

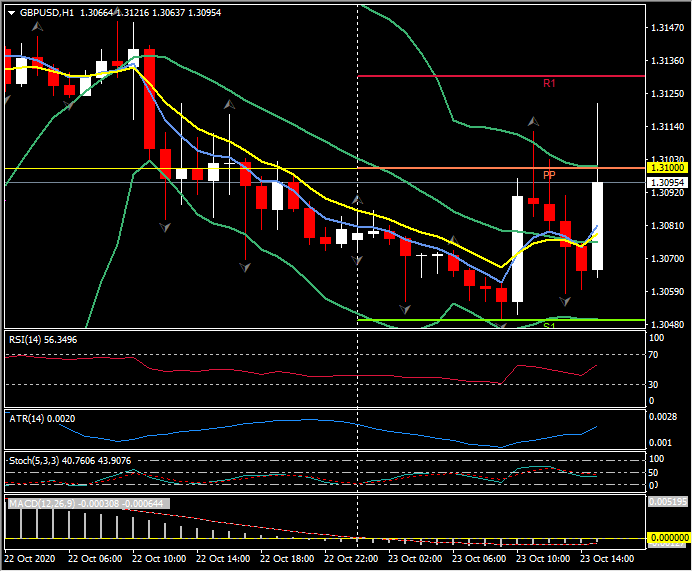

Cable settled at near net unchanged levels around 1.3090-95 after dropping back from a high at 1.3124. The UK currency remains comfortably up on week-ago and month-ago levels against the Dollar and Euro, and others, with market participants anticipating a limited trade deal between the EU and UK. The two sides are amid intensive face-to-face discussions. The UK and Japan today signed the trade deal that was agreed in principle a month ago.

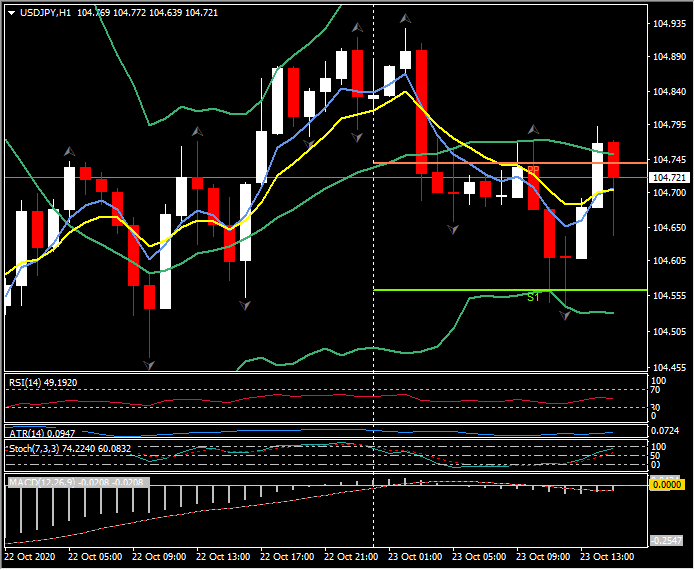

USDJPY is modestly softer after upside forays over the last day stalled at 104.93-95. At levels around 104.70, the pair remains down by 1% on the high seen on Wednesday. AUDUSD rallied to an eight-day high at 0.7158, floated by higher stock markets in Europe and an above-forecast composite PMI reading out of Australia. Global asset markets are likely to remain skittish, notwithstanding the rally today, with investors pondering the uncertainties presented by the surge in Covid cases in Europe and elsewhere, including now in many US states and in Canada, and which are leading to ever more restrictive countermeasures. The ongoing delay in new US fiscal stimulus and the event risk posed by the upcoming US elections are also in the mix. Regarding the elections, polls point to a Biden presidency, but it is less clear if his Democratic party can take control of the Senate. If not, then Congress will remain split at least until the mid-term elections in two years, which will limit the scope for policy changes and crimp Democrat ambitions for expansive fiscal policy.

US data later is topped by flash PMI data, Manufacturing numbers are expected to show a slight rise to 53.5 from 53.2 last time, whilst the more important and significant Services numbers are expected to increase by a single tick from 54.6 to 54.7. The data is due at 13:45 GMT.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.