Market News Today

The selloff in Treasuries deepened as the market returned from its long Presidents Day weekend. The stock rally started to run out of steam, while the selloff in bond markets continued. The bear steepener remained fully intact as the reflation trade and technicals gripped the market. 10-year Treasury yields reached levels last seen in February 2020 yesterday, before falling back -1.5 bp and settling around the 1.3% mark. Longer dated yields are at or near 1-year highs. But even when the full equity rally fizzled and the USA100 fell into the red, bond yields continued higher. A stronger than expected Empire State index also supported the bearish case in bonds.

JGB rates have lifted 2 bp to 0.094% and bonds also sold off in Australia and New Zealand, leaving rates more than 8 bp higher on the day. Meanwhile the JPN225 corrected -0.6%, despite an unexpected rebound in core machinery orders. GER30 and UK100 futures meanwhile are down -0.04% and up 0.3% respectively, while US futures are posting fractional gains after a mixed session in Asia.

Equities have already come a long way and there may not be much appetite to push valuations out further at this point, but stimulus hopes and vaccine developments continue to fuel reflation trades and central bank efforts to try and slow the rise in yields by stressing that monetary policy will remain accommodative, risk fuelling a bubble in speculative assets that could come back to haunt markets further down the line.

In FX markets USDJPY dropped back to 105.96, amid a broadly higher yen, although the Dollar rose against most other currencies. USOIL meanwhile is trading at $60.19 per barrel. EURUSD dropped back to 1.2070, Cable to 1.3868. Bitcoin rose, again, through $50,000 as signs of big investor interest in the asset drive more and more buying. Gold prices extended losses for a fifth straight session on Wednesday, slipping to near 2-week lows as soaring US Treasury yields and a firmer Dollar dented the bullion’s appeal.

Today – Data releases today focus on US Retail sales and Canadian inflation for January, along with the FOMC minutes.

The FOMC minutes to the January 26, 27 policy meeting should underscore the Fed’s commitment to a lower for longer rate stance, with no intention of trimming QE. We know the meeting resulted in no change in policy and so the minutes will not break any new ground. Indeed, last week Chair Powell’s sombre outlook where he emphasized the need for ongoing support from monetary policy due to the pandemic was in keeping with the tweaks in the January policy statement. One such tweak was that the Fed’s acknowledgement that “the pace of the recovery in the economy and employment has moderated in recent months, with weakness concentrated in the sectors most adversely affected by the pandemic.” We’ve also heard Fedspeak that the entire FOMC is generally on board with this posture, including allowing inflation to run hot for some time.

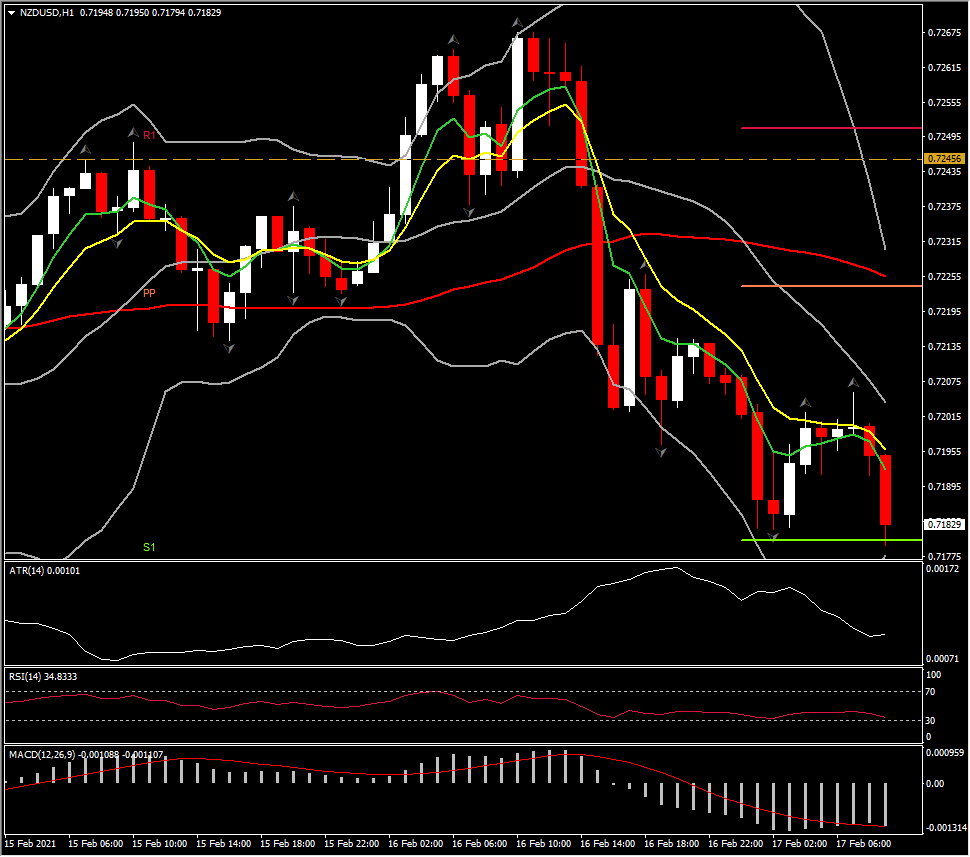

Biggest (FX) Mover @ (07:30 GMT) NZDUSD (-0.40%) extended losses below 20-DMA. Next Support remains at the 50-DMA at 71.60. MACD lines and RSI are neutral but still turning lower while intraday they are both negatively configured, with fast MAs sloping further lower.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.