Market News Today – Stocks have moved broadly higher as investors continue to focus on the recovery. Hence stocks closed Q1 mostly firmer, with a new record high on the USA500, rising 0.46% to 13,246. The USA100 climbed 1.54% to 13,246 as big tech recovered some poise and helped the index post a 0.4% gain on the month. While for the first three months of the year, the USA30 was up 7.76% as reflation/reopening trades gathered steam. Risk appetite has been supported by vaccines, and now by expectations of more stimulus with President Biden announcing another $2.25 tln infrastructure deal.

Tightened restrictions resulting from virus flareups in some parts of the world were overlooked for now, but have the potential to limit the rise in markets that have already come a very long way. Yields have also risen sharply and the Bloomberg Barclays index tracking US government bonds, reported the worst quarterly performance since 1980.

In Europe, Eurozone bond markets closed higher and stocks struggled, with dovish comments from ECB’s Lagarde helping to underpin peripheral markets. The central bank head stressed once again that monetary policy will remain very accommodative for some time to come, which helped to counterbalance the uptick in inflation.

In FX markets, after hitting fresh near 5-month highs overnight, the USDIndex lost some ground through in NY and Asia trade falling to 92.99 lows, but USDIndex is back on 93.30 area again this morning. Profit taking appeared to be a motive, despite mostly better data. The USDJPY was little changed at 110.71, with both gaining against most other currencies. AUD meanwhile was the main underperformer. The EUR and GBP are firmed holding into two-week low territory. The USOIL is at $59.61.

Today – For today, the focus will be on confidence numbers again, with the final round of manufacturing PMIs, which are likely to confirm a further acceleration in the pace of expansion. Attention is on US Friday’s jobs report.

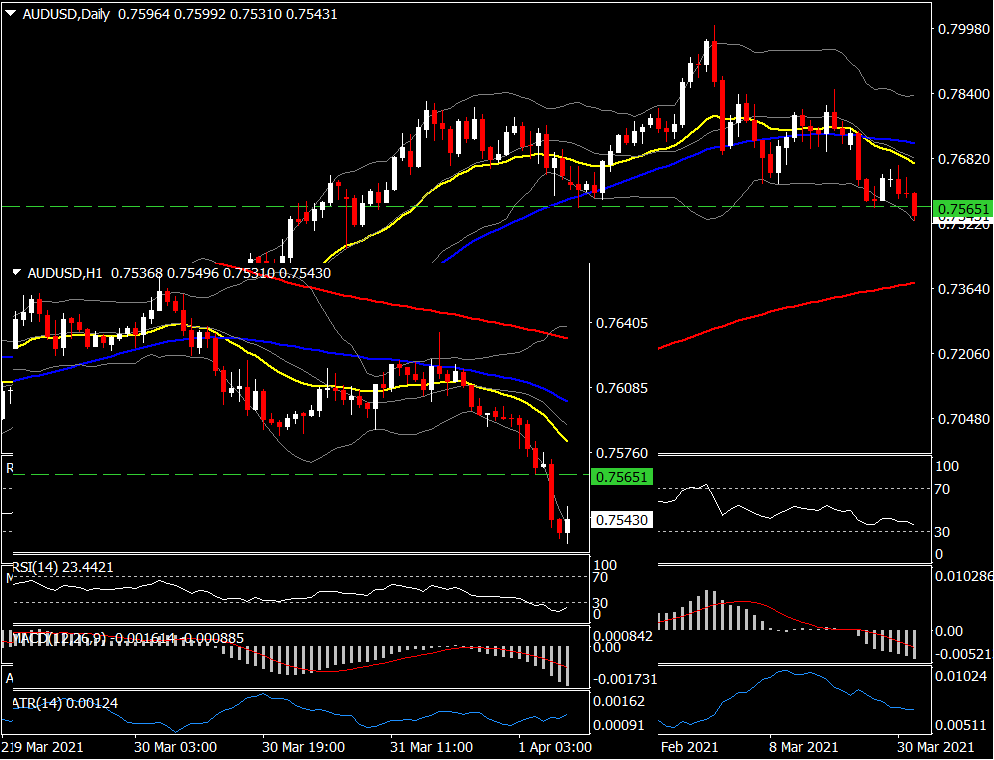

Biggest (FX) Mover @ (07:30 GMT) AUDCAD (-0.71%) The asset drifted to 0.7530 breaking a 3-month support level which seems also to be a neckline of a head and shoulder formation. Fast MAs aligned lower, with RSI turning higher in the OS area, however MACD histogram & signal line are negatively configured. H1 ATR 0.00125, Daily ATR 0.00696.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.