Market News Today – Equity markets started the week with modest caution. Asian stock markets headed south and Treasuries have erased earlier gains and are unchanged on the day, leaving the 10-year yield at 1.66%. JPN225 lost -0.59%, the ASX lost -0.4% and Hang Seng and CSI 300 are down -0.7% and -1.3%. China imposed a record CNY 18 bln antitrust fine against Alibaba, which seems to have weighed on overall sentiment, even as the company stock rallied as the decision removed a regulatory overhang. US comments on China’s relations with Taiwan, virus jitters and in Australia uncertainty over the vaccination program added to the cautious tone as investors brace for major earnings reports this week. Higher than expected PPI inflation out of Japan also didn’t help. GER30 and UK100 futures are down -0.2% and -0.3% respectively, alongside similar losses in US futures. Infection numbers continue to climb in Germany where state and federal governments continue to argue over restrictions and the possible need of a new hard lockdown. In the UK meanwhile the economy continues to open against the background of a rapid vaccination process.

In FX markets the Yen was supported and USDJPY dropped back to 109.55 although the US Dollar was steady to higher against most other currencies. The EUR and GBP both dropped against the Dollar, however, with EURUSD now at 1.1889 and Cable at 1.3686. The GBP also retreated against the EUR. USOIL meanwhile is trading at USD 59.07 per barrel. Bitcoin rallied, retesting all record highs again.

Today – Data releases today are thin on the ground and focus on Eurozone retail sales data ahead of German ZEW investor confidence and UK monthly GDP numbers later in the week. US-China relations and virus developments are in focus as investors brace for key earnings reports later in the week.

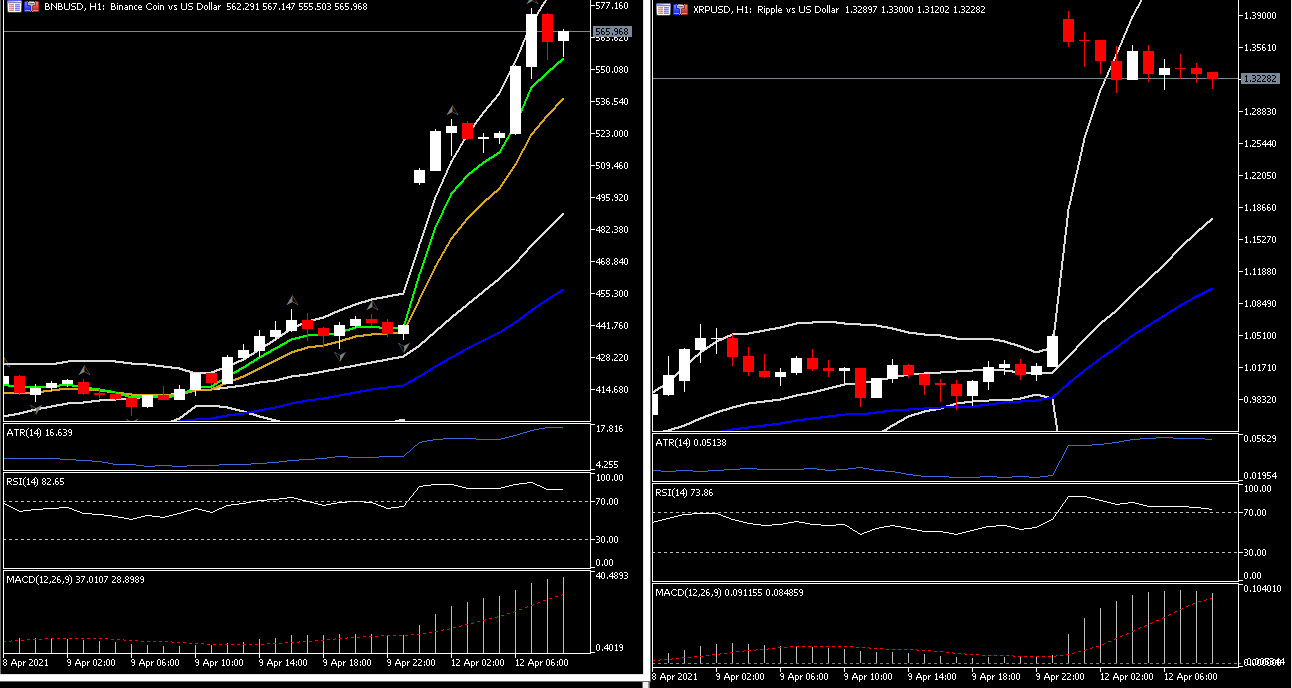

Biggest (FX) Mover – (BNBUSD at 07:30 GMT +30.49%) – The majority of Cryptocurrencies gapped up higher on open with BNBUSD at 573.38 from the 438 area. Bitcoin on the other hand broke the ascending triangle pattern, with near-term indicators suggesting an increasing positive bias.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.