September 10-year Bund future rallied with Treasury futures overnight & in cash markets the US 10-yr rate corrected a further -1.3 bp to 1.33%. Υields also dropped in Australia & New Zealand, with the former outperforming despite a drop in the unemployment rate to just 4.9% – the lowest in 10 years. EGBs also ended higher yesterday after Fed Chairman Powell calmed nerves on the inflation front & managed to ease fears the Fed will move earlier than expected on tapering- Tapering is still “a ways off.”

The BoC left rates unchanged, as expected, while cutting its weekly QE purchases by C$1.0 bln, also as expected. The BoC statement left forward guidance unchanged from the previous meeting, though did downgrade 2021 GDP modestly while upping growth expectations for 2022.

BoE’s Bailey & ECB’s Schnabel were also out to calm nerves, with Bailey highlighting the central bank will need to assess the transitory factors that are driving headline rates at the moment, though comments from Ramsden sounded more cautious on inflation risks – no rush on rate decision.

Asia stock markets traded mixed after today’s round of growth data out of China. China Q2 GDP growth slightly weaker than expected at 7.9%. UK ILO unemployment rate unexpectedly lifted to 4.8% in the three months to May and pick up in employment fell short of expectations at just 25K.

Earnings: BOA shares fell after revenue declined from a year earlier because of a 6% drop in net interest income due to lower interest rates. Citigroup beat analysts’ estimates for profit, thanks to a $1.1 billion boost from releasing reserves the bank had previously set aside for loan losses. Wells Fargo posted Q2 profit of $1.38 a share as revenue jumped 11% from a year earlier to $20.3 billion, soundly beating Wall Street’s expectations despite weak demand for loans. BlackRock’s assets under management jumped to a record $9.49 trillion in Q2 from $7.32 trillion a year earlier.

FX markets: USD steady to weaker, with USDJPY at 109.74. EUR & GBP lifted against a weaker USD, though EURUSD is at 1.1846 & Cable below 1.3865. USOIL dips to $71.44 per barrel – the combination of a reported production agreement between Saudi Arabia and the UAE, allowing the Emirates to pump more oil in 2022, combined with an unexpected weekly rise in US fuel supplies, has weighed on prices. Gold topped at 1,832 (50% Fib).

Today – Fed Chair Powell’s testimony day 2 and Jobless claims.

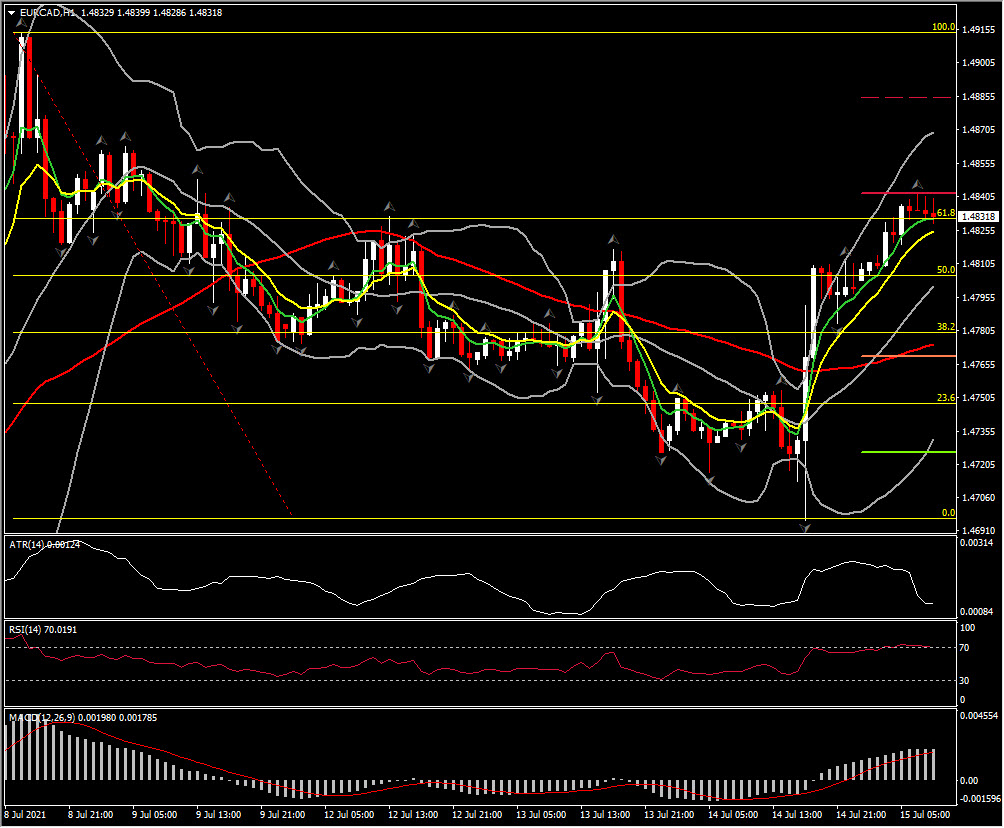

Biggest FX Mover @ (07:00 GMT) EURCAD (+0.27%). CAD headed lower, despite the taper move, in what appeared to be a case of sell the rumor, buy the news.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.