Market News Today – USD dipped following ECB & weak US data but has recovered as USDIndex eyes 93.00 again & a “Golden Cross”. EUR 1.1770, JPY 110.30, Cable 1.3750. Equities struggled but ended up, USA500 (+0.20%), Strong Earnings #TWTR. Yields held gains 1.265%. Virus concerns continue to weigh, US Republicans now encouraging vaccinations. USOil breached & broke $70.00, Gold back over $1800. Overnight – JPY closed until Monday, shares in Asia struggled to follow US higher, AUD PMI data at 14-mth lows (50% of popn. in lockdown) & UK Retail Sales data beat as restrictions continue to ease and football was supposed to come Home.

ECB – Negative Rates Are Here to Stay – ECB tweaked its rate guidance yesterday which resulted in an even stronger signal that the bank expects this year’s inflation overshoot to be temporary. The marginally higher inflation target & refined hurdles for rate hikes have pushed an exit from negative rates even further into the future, but doesn’t necessarily clarify the outlook on asset purchases & PEPP. The focus on the forward guidance may actually signal a shift back from asset purchase targets to rates as the main signal for the ECB’s policy stance.

European Open – The September 10-year Bund future is down -3 ticks, Treasury futures are slightly underperforming. DAX and FTSE 100 futures meanwhile are up 0.3% and US futures are posting similar gains. The ECB’s affirmation of its ultra-accommodative policy stance and the strengthening of the guidance on rates should continue to keep sentiment underpinned. ECB’s Villeroy also stressed this morning that it was perfectly justified to stick with accommodative settings for now, but also indicated that the central bank will look at asset purchases again in September. For now though virus developments and the rapid spread of the Delta variant is likely to keep a lid on growth optimism.

Today – Flash Eurozone, UK & US PMIs, CBR Rate Decision, Canadian Retail Sales. Earnings from Danske Bank, American Express and Honeywell.

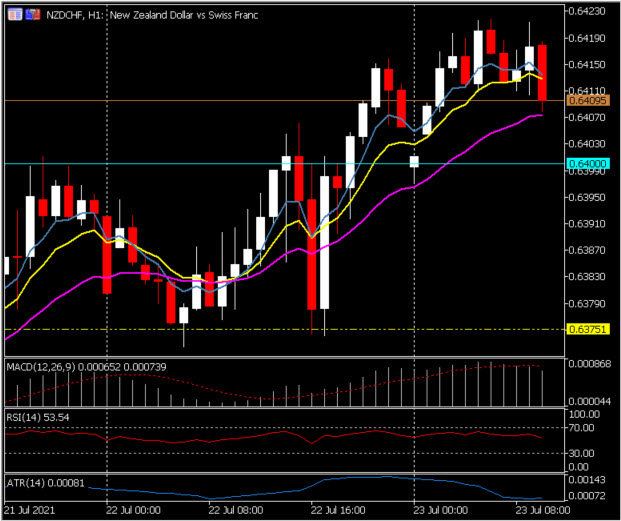

Biggest FX Mover @ (06:30 GMT) NZDCHF (+0.21%) 4th day of big move from lows of 0.6330 on Tuesday, to test 20-Day MA (0.6417) today. Breached 21EMA yesterday, faster MAs aligned higher, RSI 59 and rising, MACD signal line & histogram rising & significantly above 0 line. H1 ATR 0.0008, Daily ATR 0.0064.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.