- Supply chain disruptions are increasingly hitting production targets and adding to stagflation concerns.

- The bond market is overlooking Wednesday’s CPI data and the prospects for a hot report and the FOMC Minutes tonight.

- Global Yields grab helped underpin the long end- reflected in the solid 10-year auction results, while the 3-year evinced weaker metrics. The 2-year is 3.2 bps higher at 0.350%, the cheapest since mid-March 2020.

- Equities down. JPN225 dropped back -0.2%, the ASX declined -0.1%, although other markets looked somewhat better. Hong Kong remained closed due to weather warnings, but mainland China bourses outperformed amid strong export growth and stabilising sentiment on property developers. Japan’s machinery orders unexpectedly contracted and sentiment hit a 6-month low.

- Oil steadied in the $79.00-$81.00 area.

- FX markets – USD eased against majors, GBP strengthened

- EURUSD is ranging 1.1522-1.1560, Cable rebounds to 1.3614, USDJPY 113.30-113.60.

European Open – The December 10-year Bund future is down 6 ticks, but the 30-year has rallied while US futures are little changed. GER30 and UK100 futures meanwhile are up 0.2% and down -0.1% respectively, with US futures also lower, after a cautious session across Asia overnight. China angst eased somewhat, but elevated energy prices, supply chain disruptions and delivery problems are keeping stagflation fears alive.

Today – US inflation data will be in focus today, as markets assess tapering risks. The EU calendar includes monthly GDP numbers and production data for the UK as well as final German inflation readings for September.

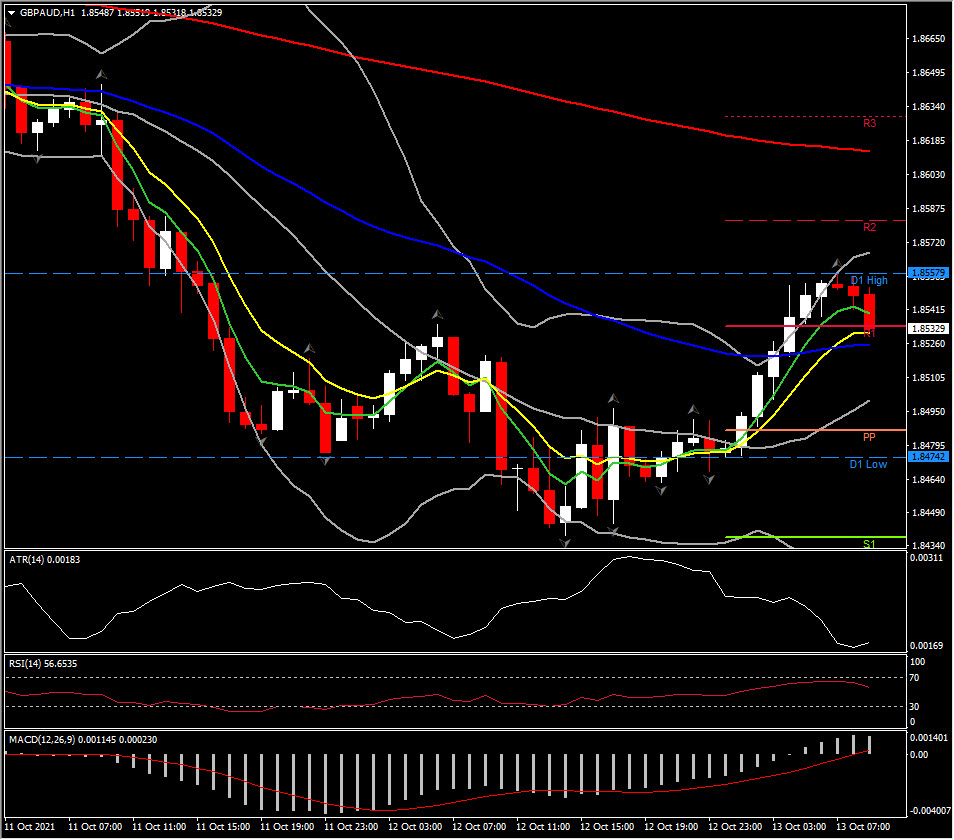

Biggest FX Mover @ (06:30 GMT) GBPAUD (+0.43%) Rebounded from 1.8435 to 1.8557. Currently faster MAs started pulling back, MACD signal line is at 0 & histogram trending higher. RSI 43 and slowing down, all indicating a correction after rally. H1 ATR 0.00184, Daily ATR 0.01096.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.