- Traders continue to mull recovery hopes and central bank policies, after the Fed minutes yesterday signaled tapering could start as early as November.

- The market is starting to price in a Fed rate liftoff into September 2022 from December previously.

- BoE officials no longer seem concerned that the spike in inflation will be temporary and markets are concerned that an early move would stifle a still fragile recovery, especially as Brexit Britain is facing severe delivery problems and shortages of staff in key areas that could have longer lasting economic consequences.

- Yields: US Treasury yield has lifted 1.6 bp to 1.55%. A stellar, record-setting 30-year bond reopening evinced continued strong demand for yields.

- China: Record high PPI number & a slight drop in headline CPI readings.

- Equities up. JPN225 managed a 1.4% gain. GER30 and UK100 futures are still up 0.4% and 0.5% respectively and US futures are also higher, led by a 0.5% rise in the USA100, which already outperformed yesterday.

- Earnings season got off to a very strong start after a big beat by JPMorgan.

- Oil lifted above $81.00.

- FX markets – USD dropped, Yen corrected.

- EURUSD is eyeing the 1.1400 mark, Cablerebounds to 1.3668, USDJPY 113.30–113.60.

- TRYslumps over Central banks shuffle – USDTRY at 18. Erdogan dismissed three central bank monetary policy committee members and named replacements.

European Open – The December 10-year Bund future is down -10 ticks and US futures are also lower, while in cash markets the US Treasury yield has lifted 1.6 bp to 1.55%. EGBs rallied yesterday, led by Gilts, although yields closed up from session lows yesterday, as the move was mainly fueled by stagflation concerns with money markets increasingly pricing in an early liftoff on rates, especially in the UK.

Today – Today’s data calendar includes US PPI and US jobless claims.

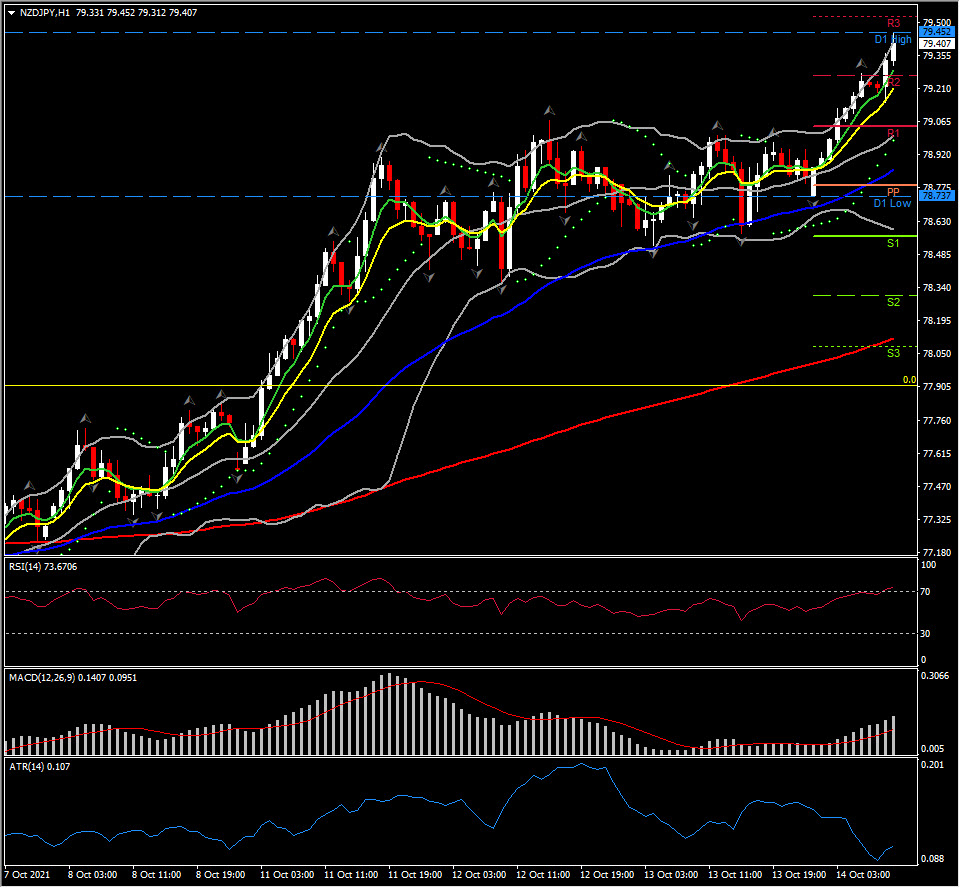

Biggest FX Mover @ (06:30 GMT) NZDJPY (+0.70%) Breached 79.45. Currently faster MAs keep pointing up, MACD signal line is at 0 & histogram trending higher. RSI 73 and sloping up, all indicating further upwards move. H1 ATR 0.107, Daily ATR 0.748.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.