- USD (USDIndex 93.85) down again from Friday’s 1-yr high 94.62, under 94.00. PPI today & CPI tomorrow weigh as equities grind higher & yields slip again. FED Vice-Chair Clarida remained Dovish “a ways away from considering raising interest rates,” although “necessary conditions for raising the target range for the federal funds rate will have been met by year-end 2022.” Bullard & Bowman much more Hawkish; “If inflation is more persistent than we are saying right now, then I think we may have to take a little sooner action in order to keep inflation under control.”

- Evergrande contemporary Kaisa needs “help”, downgraded by Fitch; Fed warns “ailing Chinese real estate sector poses threat to US economy” – FT

- US Yields (10yr closed down again at 1.474%) lifted a tad overnight to 1.497%, below key 1.50 level.

- Equities at all-time highs again but limited gains – USA500 +4.17 (+0.09%) at 4701 – Big movers – TSLA -4.84%, AMD +10.14%, AMC +8.06%. Softbank, PayPal, Roblox, Tencent and Zynga all beat Earnings expectations – USA500.F back to 4686. Asian equities weaker.

- USOil – slips below $81.00 to $80.65. Biden may act on high US Gasoline prices – speaking with OPEC+ re output, Private Inventories later today.

- Gold recovers further from Friday’s breach & break of $1800 as yields remain weak, inflation worries swirl and seasonality looms. Touched $1827 for a 45-day high earlier, back to $1824 now.

- FX markets – EURUSD up to 1.1600, USDJPY under 113.00, @112.80 & Cable up to 1.3570.

Overnight – JPY data mixed; Earnings & Current Account weaker than expected, Lending and Econ. Sentiment significantly higher. JPY recovers recent losses. German Trade Balance missed – Exports declined -0.7% while Imports nudged up 0.1%, suggesting more weakness.

European Open – Dec 10-yr Bund future up 1 tick, DAX & FTSE 100 futures down -0.2% & -0.3% respectively, US futures also in red, after a largely weaker session across the Asia-Pacific region overnight. Volatility in bond markets has been very high, as markets struggle to find an equilibrium amid the gradual advancing turn in CB cycles. That keeps central bank comments firmly in focus.

Today – EZ ZEW, US PPI, A whole gaggle of CB Speak – ECB’s Panetta, Knot, Lagarde, Schnabel, BOE’s Bailey & Broadbent, Fed’s Bullard, Powell, Daly. US 10-yr Bond Auction.

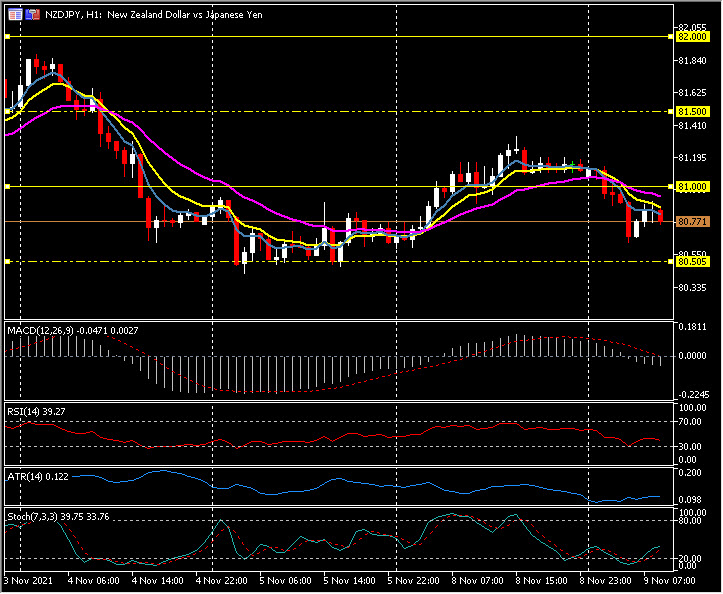

Biggest FX Mover @ (07:30 GMT) NZDJPY (-0.39%) RJPY up on overnight data mix. back under 81.00 today to test 81.60. Faster MAs aligned lower, MACD signal line & histogram falling & under 0 line, RSI 39 & falling. H1 ATR 0.122, Daily ATR 0.784.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.