Hot CPI data on Friday, all-time highs for stocks, & steady to stronger USD, greets a big week for central banks as markets enter the last three weeks of the year.

- USD (USDIndex 96.22) rises from dips below 96.00 on Friday. Omicron news improves, case peaks appear to have been hit in Gauteng, South Africa, hospitalizations have stabilized & projected death rates appear to be 25 x lower than Delta, while mixing Pfizer, AZ & Moderna vaccines appear to give better immunity & Anti-viral drugs from Merck & GSK new data improving. US deaths top 800k, Omicron now present in 30 states and first case traced to Nov. 15. Stocks hit new all-time highs Friday USA500 +0.95% (+44pts) 4712, Futures now at 4722

- US Yields 10-year rates fell to 1.48%, down about 5 basis points from last week’s peak, and trades at 1.49% now.

- Asian Markets – Asian indices broadly higher, despite slightly weaker than hoped Japan Tankan survey& more omicron warnings, which were counterbalanced by signs China will take further steps to boost economy. Topix & Nikkei currently up 0.1% & 0.7% respectively, while Hang Seng & CSI 300 are posting gains of 0.5% & 0.7%. Shanghai & Shenzen Comp have lifted 0.4% & 0.6% so far, ASX closed 0.4% higher.

- USOil – continues to recover and holds over $70.00 for a 5th consecutive day and trades at $72.25.

- Gold – dipped to test key $1770 on Friday, recovering to $1785 now

European Open – The March 10-year Bund future is down -16 ticks, U.S. futures are outperforming slightly, but are also in the red. DAX and FTSE 100 futures are currently posting gains of 0.4% and 0.3% respectively and U.S. futures are also posting gains of around 0.3%. In FX markets both Euro and Sterling struggled against a largely stronger dollar, leaving EURUSD at 1.1285 and Cable at 1.3227 and USDJPY at 113.50. The UK upped its warnings on the omicron variant over the weekend and is targetting all adults to have received a booster by year-end, a month ahead of current schedule. In the short run at least, the risks to growth forecasts are to the downside, which will also overshadow central bank decisions this week.

BoE, ECB, SNB & Norges Bank all set to announce policy on Thursday – hot on the heels of the FOMC decision on Wednesday. For the BoE it will likely mean that the flagged rate hike will be pushed out into next year, and possibly 2023 although inflation & labour market data ahead of the announcement could throw a spanner in the works.

Today – OPEC Oil Market Report, BoE Financial Stability Report, Speech from BOE’s Bailey.

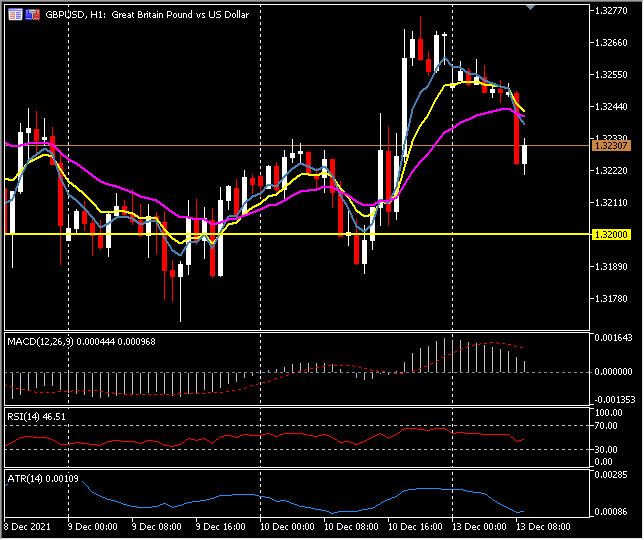

Biggest FX Mover @ (07:30 GMT) GBPUSD (-0.31%) Recovered from sub-1.3200 Friday to 1.3265 highs, down on open, 1.325 now. Currently MAs aligned lower, MACD signal line & histogram moving lower, RSI 46.00 & weakening. H1 ATR 0.0011, Daily 0.0081.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.