- USD (USDIndex 96.60) rallied on Friday from 95.80 lows and holds gains to start the week. Stocks sank again on Friday and are lower today, Yields also fell and remain down. Oil tanked -2.79% Friday to 2-week lows, GOLD rallied and cooled but holds $1800. Risk off starts the new week with JPY in demand. Catalyst – OMICRON – lockdowns and further restrictions in Europe, health systems stretched. Other market news – China cuts borrowing costs, Biden’s $1.75tn build back better bill will be blocked by Manchin. Chile (worlds biggest Copper producer) elects young left-wing President (Boric).

- US Yields 10yr traded down significantly to 1.402% on Friday, now down again 1.36%

- Equities – USA500 -48 (-1.03%) at 4668 (was down over 68pt) Dow lost over 500pts– USA500.F trades down again at 4568.

- USOil – slumped over -2.79% to close at $70.14 and is down another $2.50 again today to $67.50

- Gold – Another volatile day on Friday, touched 1815 but closed at 1798. Holds over $1800 currently.

- FX markets – EURUSD 1.1250 from 1.1235, USDJPY 113.40 from 113.70 close on Friday, Cable closed at 1.3234 down again today to test 1.3200, after more political turmoil, as Brexit Minister Lord Frost resigns and more photos of Tory staff (including Jonson) breaking lockdown rules.

Overnight – ECB’s de Cos: Rate hikes are unlikely in 2022, NZD Trade balance improves significantly and consumer sentiment surprisingly holds up.

European Open – The March 10-year Bund future is up 36 ticks, the 30-year has rallied 90 ticks, alongside broad gains in US futures, amid concern that Biden’s spending package won’t get sufficient support to go ahead after all. US growth forecasts are already being revised down in some quarters and without the prospect of considerable fiscal support, it will remain up to the central bank to keep the economy afloat, which will likely mean a less aggressive tapering schedule from the Fed. Stock markets tanked across Asia on the news and DAX and FTSE 100 are down -2.2% and -1.7% respectively. Virus developments are adding to the risk off backdrop, with parts of Europe already back in lockdown and others once again contemplating wide spread closures over the holiday period as booster programs are not fast enough to deal with the Omicron variant.

Today – U.S. leading indicators

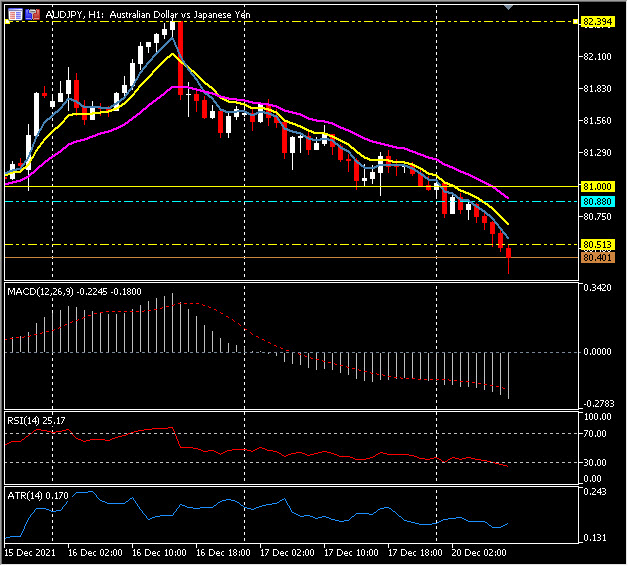

Biggest FX Mover @ (07:30 GMT) AUDJPY (-0.74%) Down from 82.40 on Thursday to 80.25 now. MAs aligned lower, MACD signal line & histogram moving lower & under 0 line since early Friday, RSI 26, OS but still falling. H1 ATR 0.17 Daily ATR 0.97

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our written permission.