Stock markets closed higher after another volatile day (DOW +0.78%) Asia markets higher but in thin trading, USD & Yields weaker, Oil holds a bid and Gold sinks below $1800. RBA’s Lowe decision to end bond buying wasn’t a signal of a quick lift off on rates, which helped the ASX rally 1.2%. The focus shifts to earnings and company reports as the excitement over the Fed’s road map to higher rates eases with BoE & ECB in the background.

China, Hong Kong and other markets remained closed for the Lunar (Tiger) New Year holidays.

- USD (USDIndex 96.18) slips again, next support key 96.00 level

- US Yields 10-yr closed at 1.80% & trades at 1.79%.

- Equities – USA500 +31 (+0.69%) 4547 – (UPS +14.08%) USA500 FUTS slip 4504. Alphabet gained +7% after hours & 20 for 1 stock split. Santander profits up 8-fold.

- USOil – Spiked close to 7-yr high over $87.00 on drawdowns and OPEC+ meeting today, now $86.68

- Gold – topped at $1807 back to $1796 now.

- Bitcoin remains under $40,000 back to test $38,300

- FX markets – EURUSD up to 1.1277 USDJPY down to 114.60 & Cable to 1.3535

Overnight – NZD – Unemployment rate a tick lower at 3.2% but jobs growth 3 ticks worse than expected at 0.1% vs. 0.4% expected and significantly worse than last Q at 1.9% due to new lockdowns

European Open – The March 10-year Bund future is up 19 ticks, outperforming versus US futures, which are also slightly higher. DAX and FTSE 100 futures are posting gains of 0.7% and 0.5% respectively, while a 1.1% rise in the NASDAQ is leading US futures higher. The German 10-year rate closed in positive territory again yesterday as the ECB announcement comes into view, where central bankers are increasingly under pressure to justify ongoing net asset purchases as inflation continues to overshoot not just the target, but projections. Manufacturing PMIs yesterday flagged that companies are preparing to pass on mounting cost pressures, which will keep inflation high for a while to come. The situation in the UK is not much different and the BoE is widely expected to hike rates tomorrow, or at the very least clearly flag a move at the following meeting.

Today – EZ CPI (Flash), US ADP, AUD Services PMI, OPEC+ Meeting, BoC’s Macklem & Gravelle, US Quarterly Refunding. Earnings from Meta, AbbVie, T-Mobile, Novartis, and Vodafone.

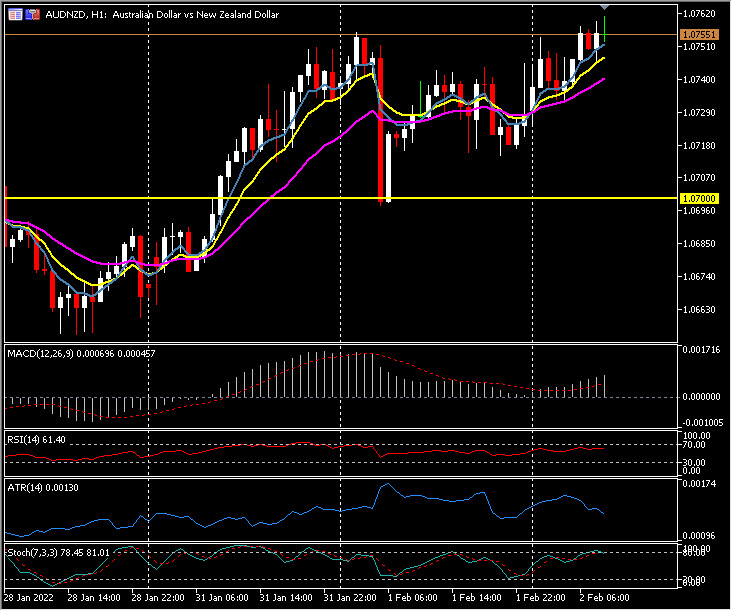

Biggest FX Mover @ (07:30 GMT) AUDNZD (+0.30%) Rallied from key 1.0700 to 1.0756 now. MAs aligned higher, MACD signal line & histogram rising & over 0 line, RSI 61 & rising, Stochs OB zone, H1 ATR 0.0013 Daily ATR 0.0060.

Click here to access our Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.