European bond markets have sold off today, Bund futures are down -15 ticks, US futures are also lower, with yields extending the March spike across the globe. Curves shifted higher pretty much across the board, but with the short end underperforming slightly amid lingering stagflation concerns. UK’s inflation today hit 6.2% y/y (30-year highs) in February. The RPI – still an important measure for wage negotiations – stood at 8.3% y/y in February and coupled with an increasingly tight labour market the risk of second round inflation effects is clearly rising, as is the pressure on the government to do something to ease the jump in the cost of living.

Ukraine developments aside, fiscal responses to the jump in energy prices are also in focus this week, as governments discuss ways to cushion the impact and the UK budget is set to be unveiled today.

Companies are not only facing a sharp rise in energy costs, but also supply chain disruptions as the Ukraine war puts a stop to deliveries of intermediate goods, which has disrupted German car production in particular. At the same time, China’s lockdown in the tech hub of Shenzhen threatens to lead to ongoing delays in long awaited deliveries.

- USD is ranging (USDIndex 98.50).

- 10-year Treasury has lifted 1.3 bp to 2.395% overnight.

- Equities – Stock markets remained supported across Asia, and GER40 and UK100 futures are posting gains of 0.8% and 0.7% respectively, with US futures also higher but underperforming. Wall Street continued to see the glass half full and rallied, led by the USA100 1.95% pop, with the USA500 up 1.13% and the USA30 0.74% higher. Nikkei has rallied another 3%.

- USOil – firm above the $105 per barrel mark and Ukraine developments remain in focus, although stock markets still seem back in demand.

- Gold – remains under pressure at $1919.

- Bitcoin pullback to $41,700.

- FX markets – EURUSD steady at 1.1020, USDJPY extends to 121.40 and Cable crossed 20-DMA , currently at 1.3260.

Today – Chancellor Sunak will present his spring budget today amid mounting pressure that he ditches the planned rise in national insurance contributions. Looking ahead, the PMI reports (Thursday) in particular will be in focus in light of Ukraine tensions and the pick up in energy prices.

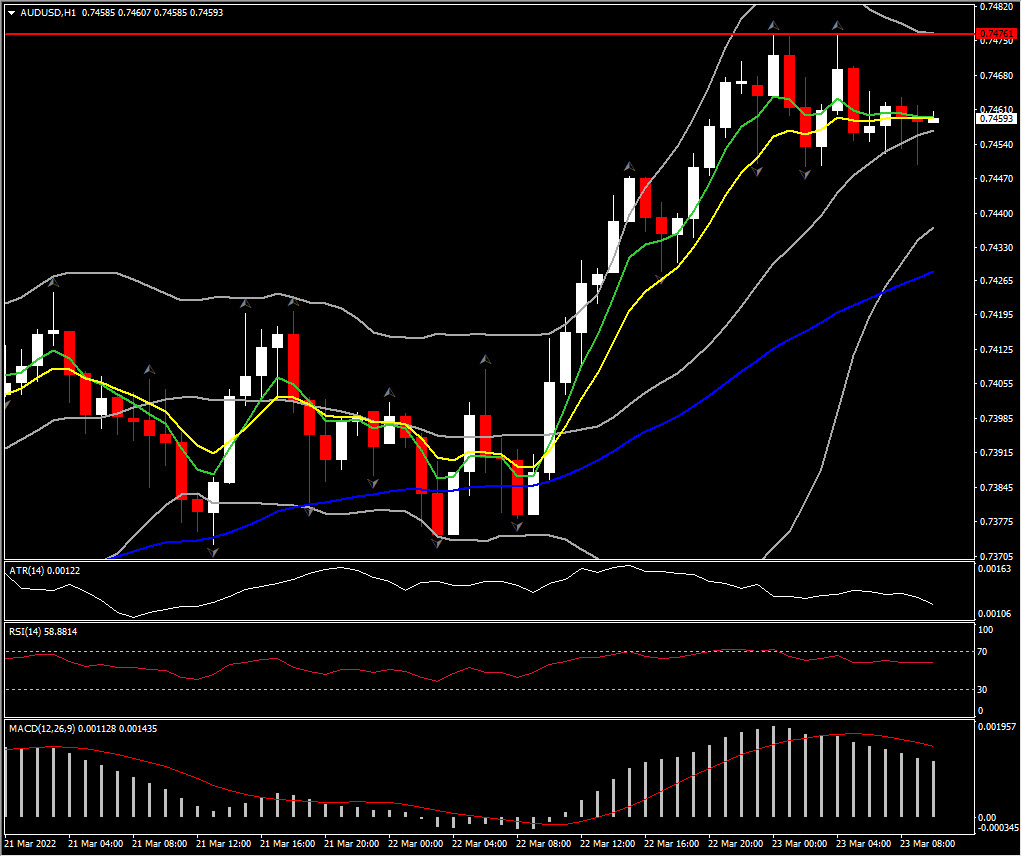

Biggest FX Mover @ (07:30 GMT) AUDUSD (+0.23%) Rallied to 0.7476. Fast MAs flattened along with RSI (59) while MACD histogram turned below signal line, implying near term pullback/consolidation. H1 ATR 0.0012, Daily ATR 0.0084.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distribution.