FX News Today

Asian Market Wrap: 10-year Treasury yields are down -0.6 bp at 3.024% and JGB yields moved up 0.3 bp to 0.076%. Asian stock markets mostly traded cautiously higher ahead of the closely watched meeting between Chinese and US leaders that it is hoped to will prevent an escalation of trade tensions amid more signs of a slowdown in China. The manufacturing PMI fell back to 50.0 – signalling stagnation, from 50.2 in the previous month, while the non-manufacturing reading dropped to 53.4 from 53.9. Topix and Nikkei managed gains of 0.48% and 0.40% respectively. The Shanghai Comp is up 0.24%, but the Shenzhen Comp is down -0.07%, while the ASX slumped -1.58% amid worries of the impact of slowing growth in China and, uncertainty about US-Sino relations and low oil prices, which are slightly above recent lows, at around the USD 51.50 mark this morning. US futures are also heading south.

FX Action: USDJPY has been trading in a narrow range, of 113.34-48, so far today, and Yen crosses and most Dollar pairings have seen a similar lack of directional bias. Stock markets in Asia have been similarly directionally challenged. The dominant excuse in market narratives is the focus on the upcoming Trump-Xi meeting at the G20 gathering in Argentina, which has taken the status of a risk event for global markets. While the official China Daily newspaper has a trade agreement is possible, and Trump has said they are “close” to doing something, Trump has also said that he is happy with the current arrangements “because what we have right now is billions and billions of dollars coming into the United States in the form of tariffs or taxes.” The most interesting data today out of Asia has been China’s official manufacturing PMI survey for November, which produced the weakest headline since July 2016, of 50.0, a level indicating flat growth. Japanese data, meanwhile, were a mixed bag, with unchanged unemployment at 2.4% in October, while the November Tokyo CPI came in at 0.8% y/y, off the median forecast for a 1.1% y/y rate, and October industrial production rose 2.9% m/m, more than double the median forecast for 1.2% m/m growth.

Charts of the Day

Main Macro Events Today

- Euro Area Unemployment and Inflation Rate – The Euro Area Unemployment Rate is expected to have stood at 8% in October, compared to 8.1% in September. In contrast, the inflation rate in November is expected to have been at 2% y/y, compared to 2.2% in October.

- Gross Domestic Product – The Canadian GDP for the third quarter is expected to have stood at a 2% annualized rate, compared to 2.9% in the second quarter.

- Chicago PMI – The Chicago PMI in November is expected to come out lower than last month, at 58.0, compared to 58.4 in October.

- FOMC Member Williams Speech – FOMC Member Williams is set to speak at the Plenary Meeting of the Group of Thirty in New York.

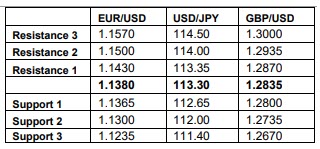

Support and Resistance

Click here to access the HotForex Economic Calendar

Dr Nektarios Michail

Market Analyst

HotForex

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.