Hopes of further stimulus measures underpinned global growth. China has already announced stimulus measures after cutting growth targets, the Fed may be on hold for longer and in Europe the focus turns to Draghi, who is widely expected to send a dovish signal at tomorrow’s meeting, even if the central bank may not be ready yet to confirm another round of cheap Targeted longer-term refinancing operations (TLTROs) loans.

Policy Outlook

From the ECB Policy perspective, the latest comments from officials in the last meeting confirmed that there is a debate around the question of whether there should be a change in the guidance, which so far still keeps the option of a rate hike later in the year on the table.

Key Question: Is the current slowdown temporary, or is it the start of a more protracted slowdown?

If rates were to stay in negative territory for longer than previously expected, there clearly would be arguments in favour of another round of cheap TLTRO loans to offset the negative impact on banks and keep the bank lending channel open.

The updated projections should bring downward revisions to growth and inflation projections, but comments from ECB’s Lane, who is set to become the bank’s next chief economist, suggest that these may not be very large. Indeed, while the manufacturing sector is clearly struggling in the current climate, there have been some glimmers of hope and the latest employment and retail sales numbers, coupled with strengthening sentiment in the services sector, suggest that the domestic economy is actually holding up rather well.

The Brexit saga continues to drag on, but the odds of a no-deal scenario seem to have diminished somewhat.

If the chance that things might turn out better than feared is ruled out, Bundesbank President Weidmann may not be the only one who is reluctant to rule out further policy normalisation just yet and commit to more TLTRO loans.

Ultimately, it is widely expected that Draghi will be delivering one of his mixed messages, where the initial statement sounds less dovish than markets expect, but the press conference compensates for that with the assurance that the ECB is already laying the ground and preparing for additional cheap funding, which it will be taking a final decision in June at the latest.

Hence it is nearly certain that expectations for a hawkish stance have been eliminated. Therefore, monetary policy expected to remain very accommodative and that ties in with the cautious assessment of the outlook. HICP inflation accelerated to 1.5%y/y and core fell to 1% y/y, giving the doves at the ECB something to argue with, especially as PMI readings offer little hope of a quick recovery in the manufacturing sector.

Economic Outlook

Additionally, the risks to the European economic outlook are increasingly tilted to the downside, based on the disappointing economic data mainly from Germany but also from the Eurozone as a whole.

Yesterday’s forecast-beating retail sales data out of the Eurozone, along with upward revisions in the final February Eurozone services and composite PMI figures, suggested that a slowdown in the Eurozone (as Draghi stated) is not a fait accompli. Consumer confidence remains in negative territory while the manufacturing sector is facing a crisis. The overall industrial sentiment is also in negative territory, with global trade tensions, fears of a slowdown in world growth and of course Brexit risks all weighing on the sector.

The above is another indication that the ECB has already missed the boat on further policy normalisation steps.

A no-change decision is all but a given, but guidance is keenly anticipated. The central bank is expected to trim growth and inflation expectations and Draghi is likely to assure markets that the groundwork for additional cheap funding has been laid, with a final decision to be taken by June.

Market Reaction

As hopes for stimulus from ECB tomorrow are increasing, market participants should expect a more neutral/minor reaction from the market. The likelihood of a third TLTRO in the next ECB meetings should not be rejected and this action could contribute on the stability for the eurozone financial system. Dovish tone could be supportive for equities similarly to what we have seen today on China’s announcement for stimulus measures after cutting growth targets.

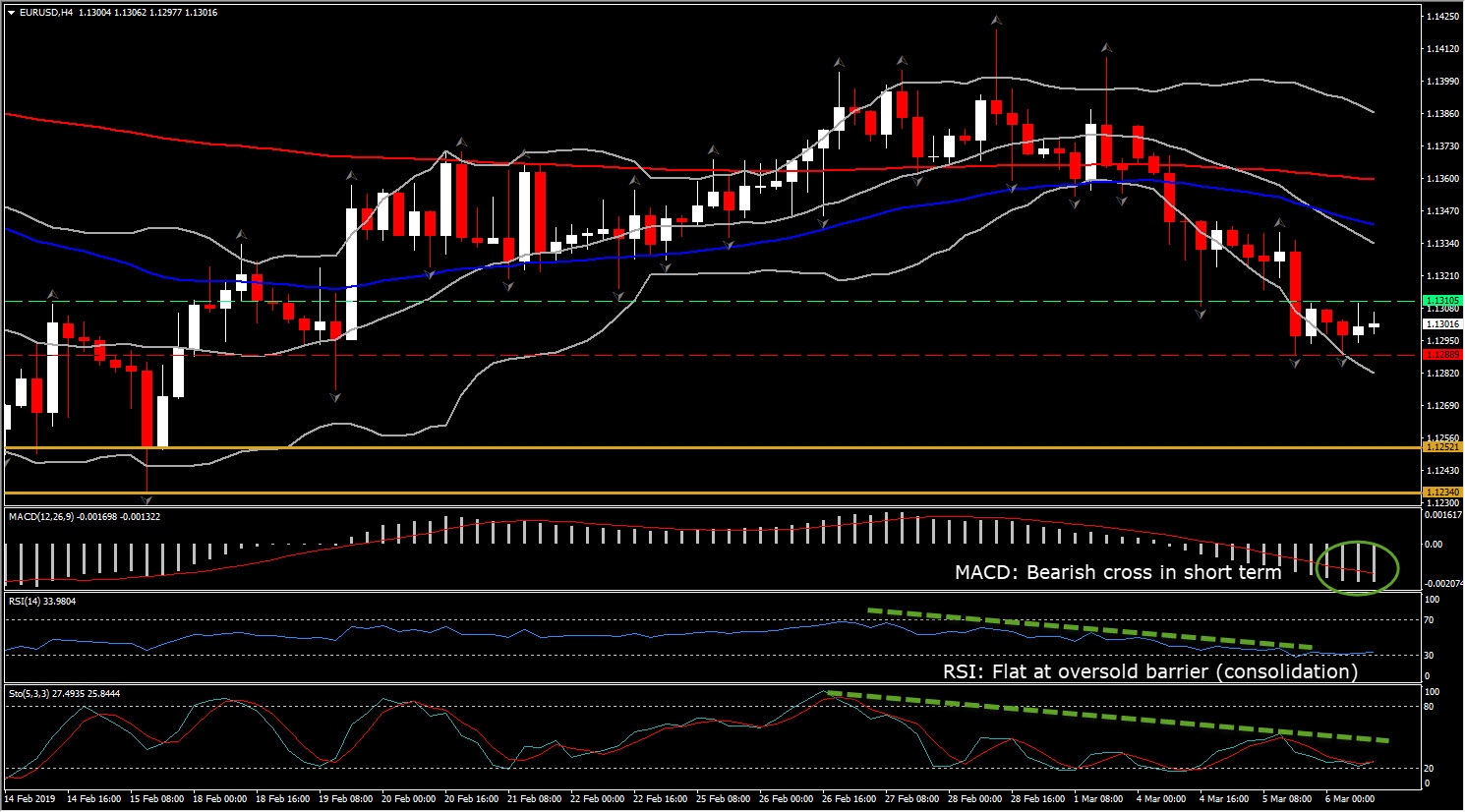

As of Euro, it has been plying a narrow ranges so far today, with EURUSD around 1.1300, holding above the 2-week low seen late yesterday at 1.1289. EURUSD has resistance at 1.1310. In the bigger view, the pair has been in a downward trend since February 2018, though momentum has been slackening.

A break and daily close below 1.1250 (3-month support) but more precisely below 1.1234, which is February’s low, will reinforce the downtrend for EURUSD.

Nevertheless, upcoming near term catalysts include the ECB’s decision and guidance on Thursday, and also Friday’s US jobs report, along with Fed Chairman Powell’s comments.

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.