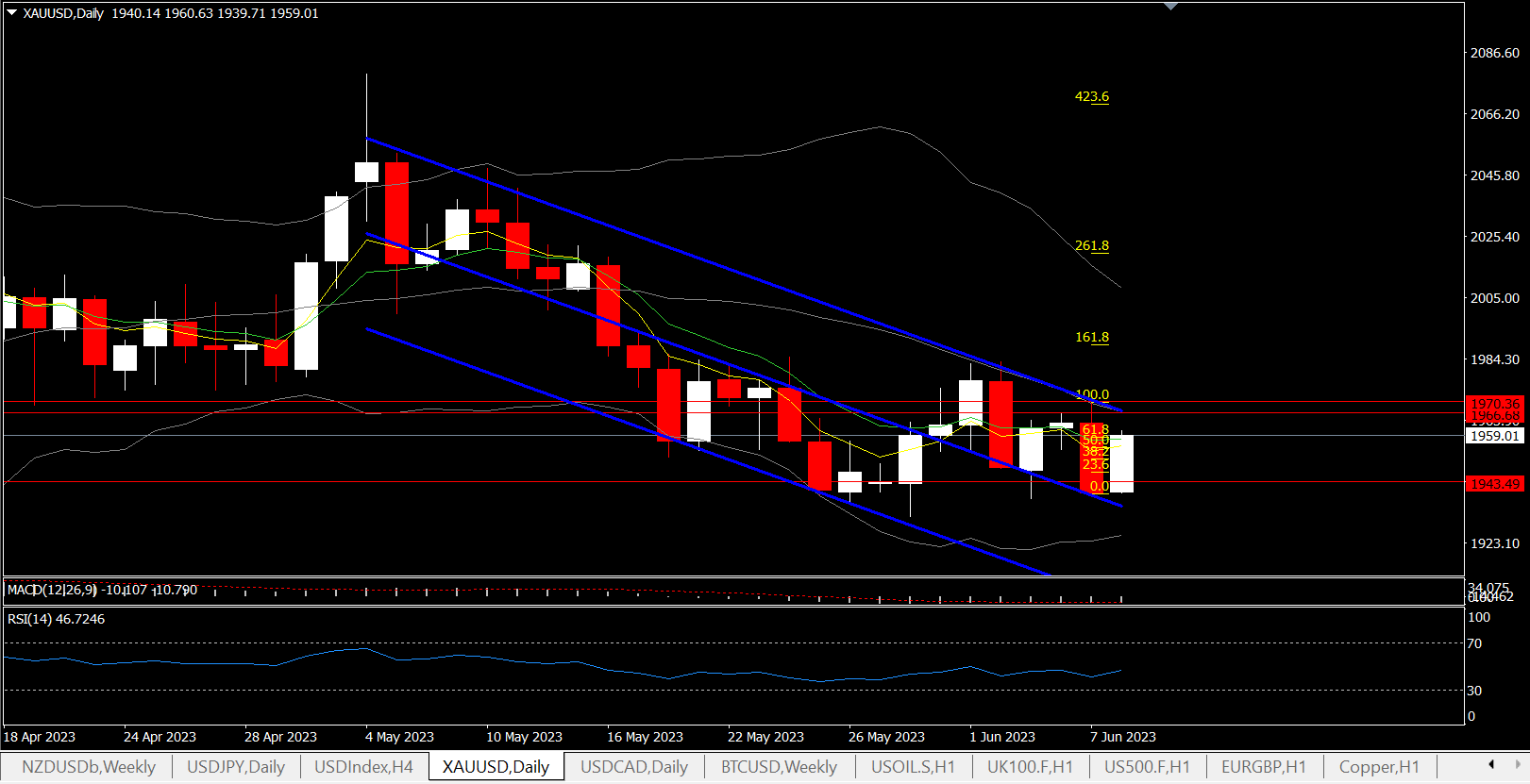

The Dollar extends decline on the climb of initial jobless claims retesting 20-day SMA, at 103.50, extending its slump from an overnight high. The pop higher in initial jobless claims helped lower the temperature on Fed rate hike fears. Significant is the fact that Gold recovered more than 60% of yesterday’s downleg, turning the attention to the key resistance area at 1966.75, which coincides with the 20-day SMA and top trendline of 1-month channel. Overall, however, Gold holds within a downchannel with momentum negatively configured, indicating than a move below $1930, could retest the crucial $1900.

Treasury yields dove and erased earlier losses, with the 2-year yield slid 5 bps to 4.508% and the 10-year is down fractionally at 3.790%, versus respective overnight highs of 4.60% and 3.818%. Wall Street futures are mixed and little changed with the US30 down -0.12%, while the US100 is up 0.21% and the US500 is fractionally firmer.

The 28k initial claims pop to a 2-year high of 261k at the start of June from 233k (was 232k) reversed the tightening in claims since April. Continuing claims diverged sharply however, with a -37k plunge to a 3-month low of 1,757k at the end of May from 1,794k (was 1,795k), leaving that measure well below the 17-month high of 1,861k in April.

Initial claims are entering June above prior averages of 234k in May and the 18-month high for the average of 239k in both March and April. For continuing claims, we now expect an 11k rise between the May and June BLS survey week readings, after a -54k drop in May that marked the first tightening since September, but prior gains of 26k in April, 99k in March, 60k in February, and 31k in January. It’s too early to tell if today’s big claims divergences imply anything about the risks for our 200k June nonfarm payroll estimate.

Meanwhile implied Fed funds futures slipped after the claims data eased fears of Fed rate hike next Wednesday. However, it’s only 1 blip on the radar screen amid a very noisy batch of numbers since the May 2-3 FOMC. The June contract fell to 5.147% from 5.157% yesterday, with July at 5.273% from 5.283%. December is at 4.991% from 5.029%.

The futures are suggesting about a 25% chance the FOMC will follow the BoC and RBA with a quarter point tightening. July is reflecting about a 63% probability for a move up in rates by the end of July. The markets will now await the CPI report on June 13, the first day of the FOMC’s 2-day meeting where we are forecasting gains of 0.2% and 0.4% for the headline and core. Results in line with our forecasts would see the y/y rates slow to 4.2% from 4.9% in April for the headline, and 5.2% from 5.5% for the core, although both clearly remain more than double the 2% goal.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.