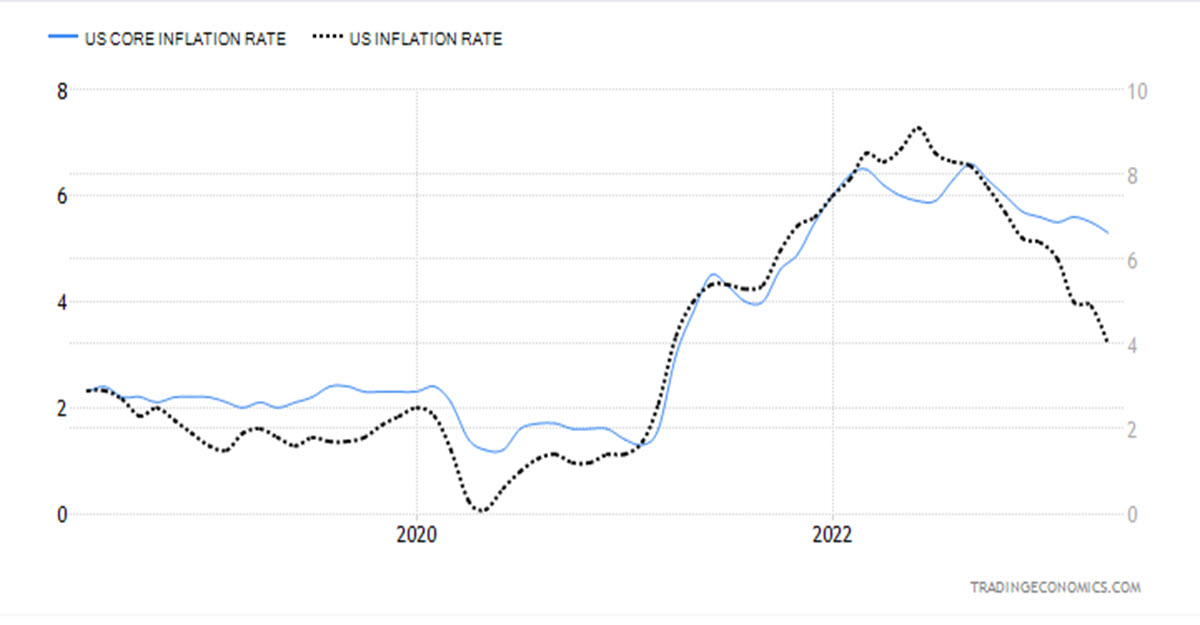

Yesterday the Consumer Price Index figure for May came out, published by the US Bureau of Labor Statistics (BLS). The CPI grew at an annual rate of 4%, the lowest reading in two years. On a monthly basis it was 0.1%. The Core CPI, on the other hand, which does not take into account food and energy as volatile items, was still too high at 5.3% y/y.

In fact, the drop in prices so far has been concentrated mainly in energy due to a reduction in the levels reached as a result of the start of the war in Ukraine. This continues to be the case, although hot components until a few months ago such as used cars (and now also new cars on a monthly basis) are starting to fall.

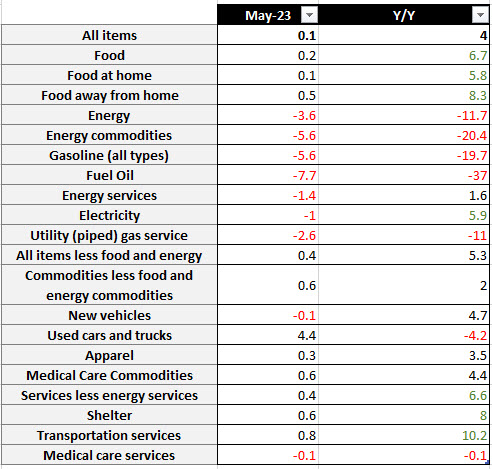

But this is not the case for all components and households continue to see their purchasing power deteriorate too fast when we talk about  Food – consumed both at home (+5.8% y/y) and outside (+8.3% y/y) – or Shelter (+8% y/y). Transportation services also continues to be too expensive (+10.2% y/y).

Food – consumed both at home (+5.8% y/y) and outside (+8.3% y/y) – or Shelter (+8% y/y). Transportation services also continues to be too expensive (+10.2% y/y).

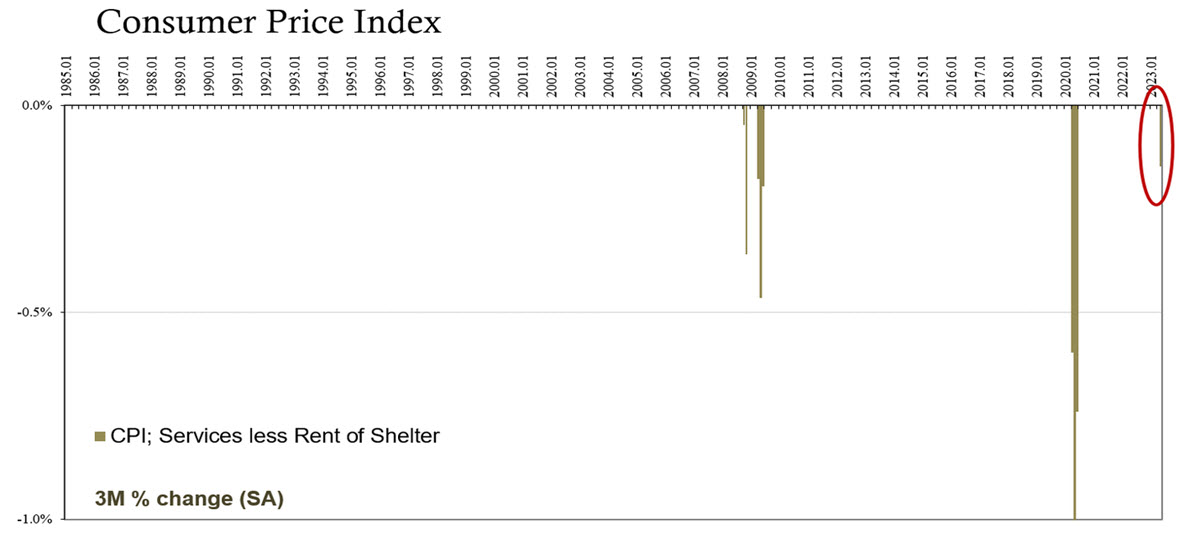

However, there are those who point out a particular and very interesting fact: services, a worrying component since it has remained stubbornly high, after subtracting Shelter is now in negative, deflationary territory! It has only happened 8 times in 40 years, most recently in 2008, 2009 and 2020: we all know how the economy was back then. Shelter will probably keep the CPI reading high for a while, but now it is no longer just energy that is slowing down or even declining (Food is up only 0.2% m/m).

Services – Shelter components are in deflationary territory!

The reaction

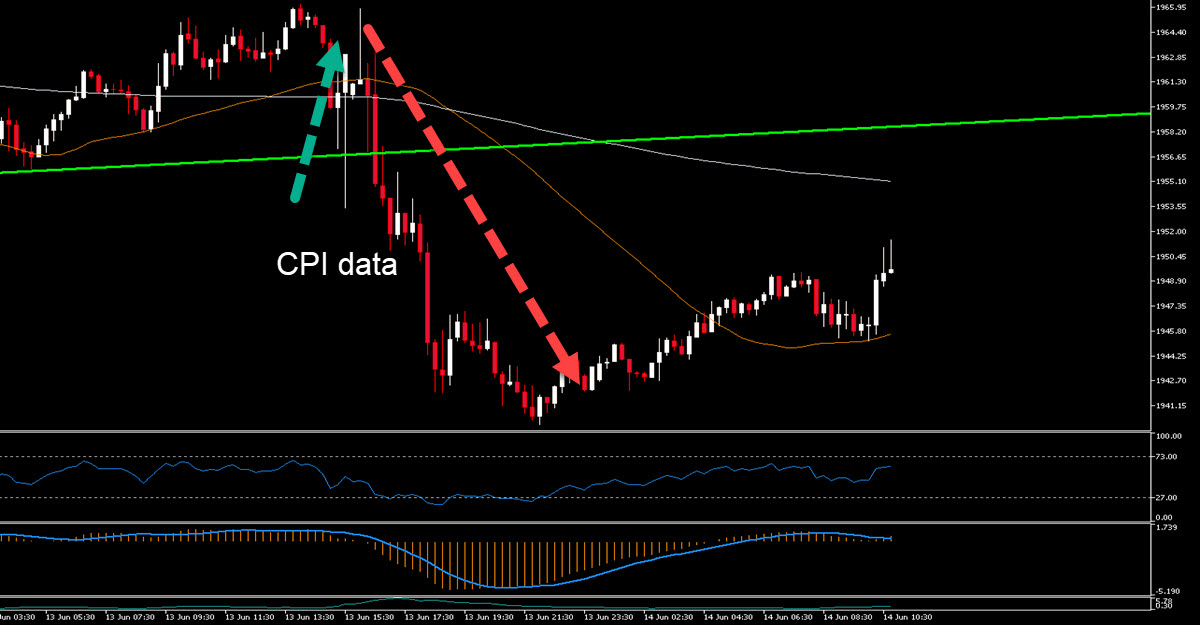

Initially, yields went down and gold went up but this movement soon totally turned around (however the drop was capped at the important $1940 support once again): this is because although traders are expecting a pause at today’s Fed meeting (stuck at 5%), expectations for cuts by the end of the year are diminishing (now it is not quite certain whether it will be at 4.5% or 4.75%). The 2y US is back to its highest level since March and is charging upwards.

GOLD, 15 mins

The USD fell with conviction but soon caught some bids that limited its movement (EURUSD is back below 1.08, for example); against the Yen, it even locked in some gains. (>140 again).

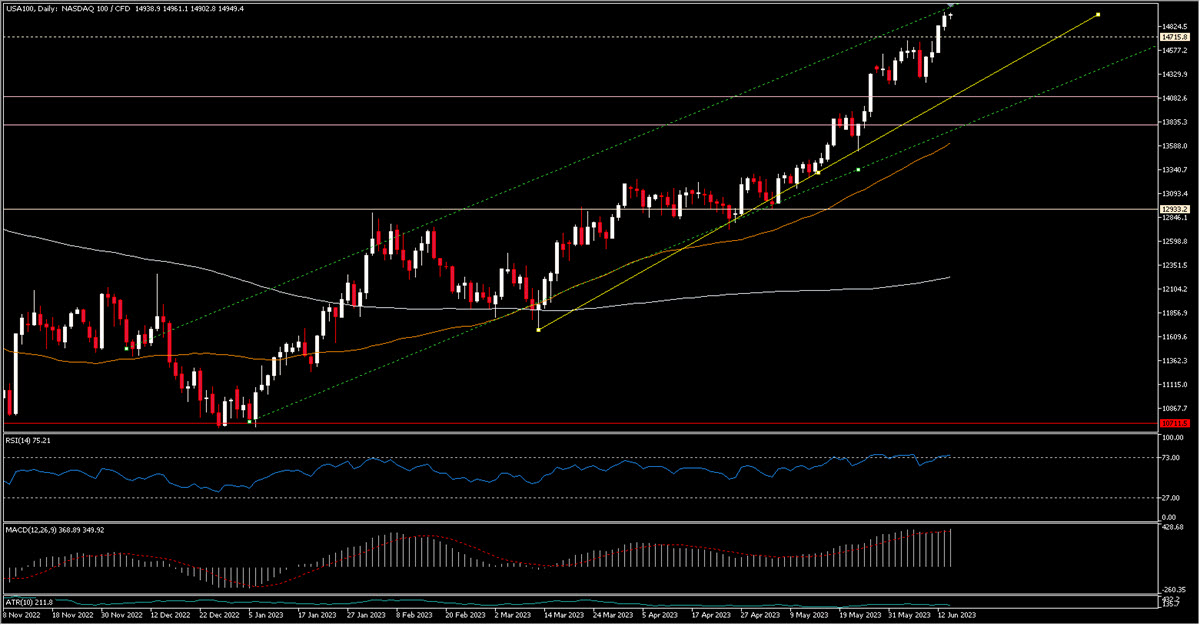

Indices went up: US500 is up for the 4th day in a row and the Nasdaq even outperformed (1.74%), although it is considered to be rate sensitive.

US100, Daily

After this important data, tonight the Fed is expected to pause, with a 95.3% probability. This in no way detracts from the possibility of another 25 bps hike on 26 July, currently priced at 63.1%, and the central bank is likely to remain hawkish at the same time that it will affirm the need for a pause in order to assess the effects of monetary policy to date and not make the mistake of overstretching (it probably won’t say this explicitly). The indices have in any case already celebrated the very likely pause by showing FOMO-like behaviour: we will see if there will be a classic ”buy the news, sell the fact” reaction.

Click here to access our Economic Calendar

Marco Turatti

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.