FX News Today

- Bund yields are coming down again and the 10-year Treasury rate is at 2.412%, down -1.1 bp on the day, underperforming versus bonds in Australia, New Zealand and China.

- The US 10-year rate remains below the 3-month rate, which continues to feed concerns about the growth outlook and the risk of recession, especially against the background of dovish shifts at major central banks, and is underpinning choppy trade in stocks.

- Japanese equities, which outperformed Tuesday, underperformed today and Topix and Nikkei lost -0.52% and -0.23% respectively.

- Chinese markets, meanwhile, outperformed after heading south yesterday, although mainland China indices are down from earlier highs. The Shanghai benchmark is still up 0.60%, the blue-chip CSI 300 1.00% higher on the day and the Hang Seng up 0.59%.

- US stock futures are also moving higher in tandem with European futures and the front end WTI future is at USD 60 per barrel.

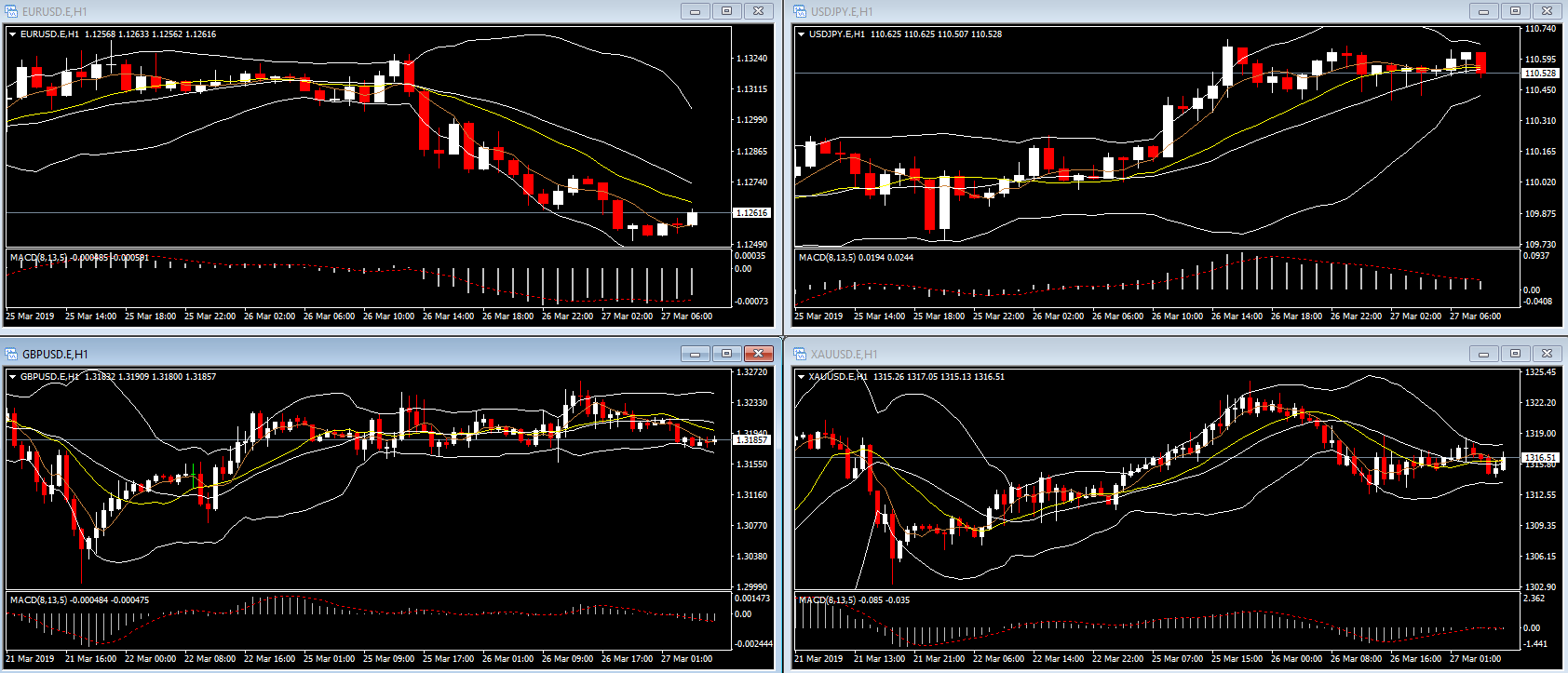

Charts of the Day

Technician’s Corner

- EURUSD broke through the 1.13 level yesterday, and is currently trading around its 1.1256 Support level. Immediate Resistance is at 1.13. Indicators are issuing positive signals.

- GBPUSD pushed down from the 1.32 level, trading around the 1.318 Support level, while the indicators suggest a slightly upwards tendency.

- USDJPY gained yesterday, breaking through the 110.34 Resistance level and is now trading between it and the 110.73 Resistance. Indicators are showing bearish signs.

- XAUUSD same as yesterday, Support and Resistance levels remain at 1313.8 and 1320 respectively, with Gold trading between those two bands.

- Biggest loser – NZDUSD: After the RBNZ’s comments that the next interest rate move is likely to be a reduction, the Kiwi lost 104 pips, pulling the AUD down along the way, albeit in a shorter movement. Resistance stands at 0.6807, while Support is at 0.6790.

Main Macro Events Today

- Draghi Speech (EUR, GMT 08:00) – The ECB President is due to speak at the “ECB and its Watchers” conference in Frankfurt, where many other ECB representatives are also expected to speak.

- US and Canada Trade Balance (USD / CAD, GMT 12:30) – Both trade deficits are expected to improve, with the US trade deficit expected to decrease to $57 billion from $59.8 billion last month. The Canadian trade deficit is expected to have declined to $3.5 billion from $4.6 billion in December.

- UK Brexit Vote (GBP, GMT 19:30) – Many options on the table for today’s vote, including a second referendum, customs union, revoking Article 50, and, of course, no-deal Brexit.

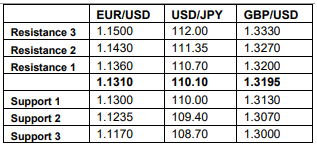

Support and Resistance

Click here to access the Economic Calendar

Dr Nektarios Michail

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.