Economic Indicators & Central Banks:

- German GfK consumer confidence unexpectedly declined. It has hit the lowest level since March 2023, despite the fact that inflation has slowed and the labor market is still looking robust – shows that business and income expectations deteriorated sharply.

- UK GfK consumer confidence improved more than expected. Falling mortgage rates and the decline in inflation clearly has helped to stabilize sentiment. Retail sales data for December as well as the CBI retailing survey for January were pretty dismal and while there is only a spurious relation to overall consumption, the data continue to flag downside risks to domestic demand.

- US: Fed funds futures are firmer as the markets see the economy’s “immaculate deflation” intact. Implied Fed funds are reflecting slightly less than a 50-50 bet for a -25 bp cut in March, with June reflecting about -60 bps in easing, while the December contract points to -140 bps by year-end.

- Yellen says strong US GDP does not raise ‘inflationary concerns’.

- ECB: Policy was held unchanged. While Lagarde didn’t really give much away, a refusal to commit to keeping rates on hold through the first half of the year, or rule out a cut in April, was enough to fuel speculation of an early move from the central bank

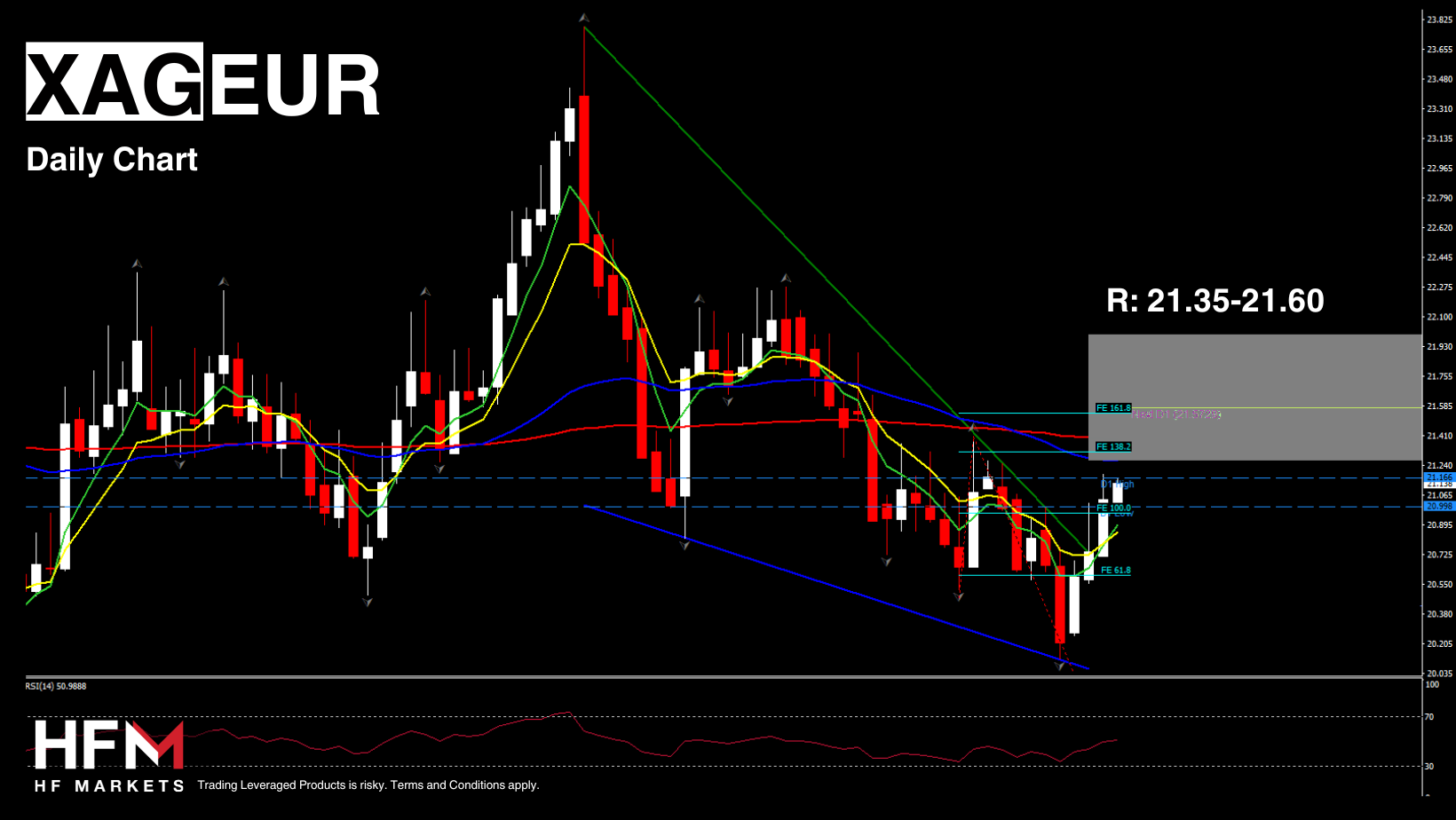

Market Trends:

Market Trends:

- European futures are slightly higher, although the GER40 (DAX) is underperforming, as markets continue to read dovish signals into Lagarde’s comments from yesterday.

- Asian stock markets corrected, led by a -1.5% drop in the Hang Seng after tech stocks came under pressure in US pre-market trading. Hang Seng and CSI 300 are still heading for solid weekly gains, however, amid signs that officials really are stepping up support measures for capital markets and the wider economy.

- JPN225 (Nikkei) lost 1% to 35,874.82 post a deceleration in Japanese inflation supporting a -2.1 bp drop in the 10-year JGB rate.

Financial Markets Performance:

- The USDIndex breached 103.50, while EUR has been under pressure. EURUSD dipped to 1.0812 post ECB day.

- USOIL broke $76 level and 2-month high, heading for the biggest weekly gain since October on sustained geopolitical tensions, lower US crude stockpiles, and prospects for additional government stimulus in key crude importer China.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.