FX News Today

- Tense geopolitical events in the Mid East injected some risk in the market, providing a boost to bonds after reports surfaced overnight that two oil tanker were damaged off the coast of Iran.

- Stock markets traded mixed in Asia with Hong Kong and China bourses under-performing.

- Australian yields marked new record lows amid concern that geopolitical trade tensions will hit global growth and prompt central banks to step up easing measures.

- The FTSE 100 future is posting fractional gains as Brexit supporter Boris Johnson emerges as the clear favorite to win the leadership contest in the conservative party and succeed Teresa May.

- Investors await data releases that are expected to show ongoing weakness in the economy.

- The WTI future is at USD 52.16 per barrel after yesterday’s attacks.

Charts of the Day

Technician’s Corner

- EURUSD headed to 1-week lows of 1.1269 at mid-morning, and it is now traded higher at 1.1277 area. Trade this week has been centered on the 1.1300 mark, and further consolidation is expected ahead of next week’s FOMC policy announcement. There is not much of a chance for a rate move next week, but the FOMC is expected to make an important change in its statement, removing the word “patient” and likely replacing it with language similar to Powell’s comment from June 4 where he said the Fed will be “closely monitoring the implications of these developments” on trade and other matters. Until then, EURUSD can be expected to remain between its 50-day moving average at 1.1219, and its 200-day moving average at 1.1363.

- USDJPY has been rangebound,topping at 108.53 before later ebbing back to 108.23 lows. Treasury yields however, continue under pressure following benign CPI on Wednesday, and soft import prices early on Thursday, putting some pressure on the Dollar. As a result, USDJPY has been nearly static. Further consolidation is expected into next Week’s Fed policy announcement.

Main Macro Events Today

- Retail Sales and Industrial Production (USD, GMT 12:30) – Retail Sales are expected to have grown by 0.6% for May and 0.3% for ex-auto sales, following a -0.2% figure for the April headline and a 0.1% increase in ex-autos. Industrial production is projected at 0.6% in May, after a -0.5% reading in April.

- Michigan Consumer Sentiment Index (USD, GMT 14:00) – The preliminary result of the Sentiment Index is expected to show a return to April’s number below 100, and more specifically to 98.

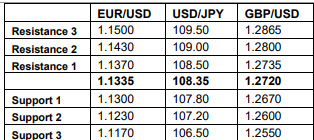

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.