FX News Today

- Trade developments remained the centre of attention.

- A Bloomberg report suggested that after a weekend of confusing signals only a few negotiators in Beijing expect that a deal with the US will be possible ahead of the 2020 election in the US election, partly because there are concerns that any deal signed now may eventually be broken by Trump.

- With hopes of a deal dampened again, Asian stocks drifted.

- Concern that the gaze of the US will also focus on imports from Japan and the EU again continueS to linger and central banks may not be quite as eager to inject more stimulus as markets are.

- JPN225 managed marginal gains of 0.16%, the Hang Seng rose 0.05%, but CSI 300 and Shanghai Comp lost -0.28% and 0.24% respectively.

- China announced measures to help boost consumption and flagged the possible removal of restrictions on car purchases, but that wasn’t enough to prevent Chinese markets from slipping.

- Norwegian Oil Fund planning to shift up to EUR 100 bln out of European stocks. The influential fund said it wants to reduce the current share of European stocks, which is at around 30%, after being scaled back previously. In the future, the US share, which is already higher, will be stocked up.

- The WTI future is trading at USD 55.54 per barrel.

- German import price inflation fell further into negative territory.

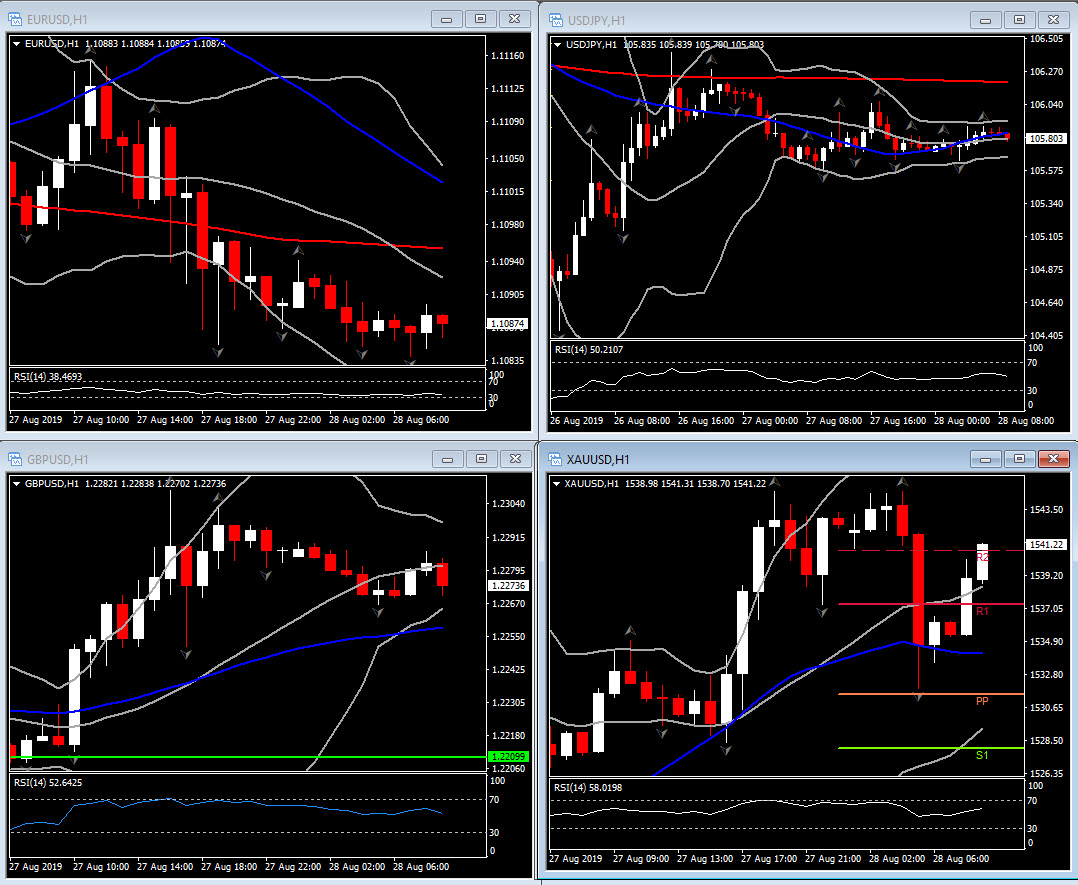

Charts of the Day

Technician’s Corner

- GBPUSD turned higher, printing near 1-month highs of 1.2310, as markets downplay the potential for a no-deal Brexit. The Brexit battle will commence next Tuesday, when parliament reopens after the summer recess. Given the level of support in parliament for ruling out the no-deal option, including some members from the government’s own Conservative Party, there is a reasonable chance that no-to-no-deal members will succeed. If a no-deal Brexit is legislated off the table, this would increase the odds of there being an extension, which in turn would put Prime Minister Johnson, having promised to deliver Brexit on October 31, in a difficult position.

- USDCAD moved mildly higher even as crude oil prices firmed. Perkier oil prices provided some support to the CAD in London morning trade. USDCAD closed above its 20-day MA, which is seen as a fresh bullish development. The level (1.3266) now becomes Support, with Resistance at 1.3315 and 1.3342, the August peak.

Main Macro Events Today

- German GfK consumer confidence held steady at 9.7% y/y in the advance September reading, unchanged from the previous month. The full breakdown, which is only available until August, also showed an improvement in the willingness to buy, while saving becomes even more unpopular in the light of falling interest rates. So far then consumption seems to be holding up, but with the labour market starting to be affected by the contraction in manufacturing it seems only a matter of time until consumption trends also slow.

- US Calendar is light, and has mortgage and oil inventory data, 2-year and 5-year auctions.

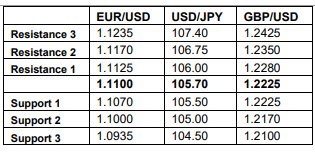

Support and Resistance levels

Click here to access the Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.