USDindex, H1

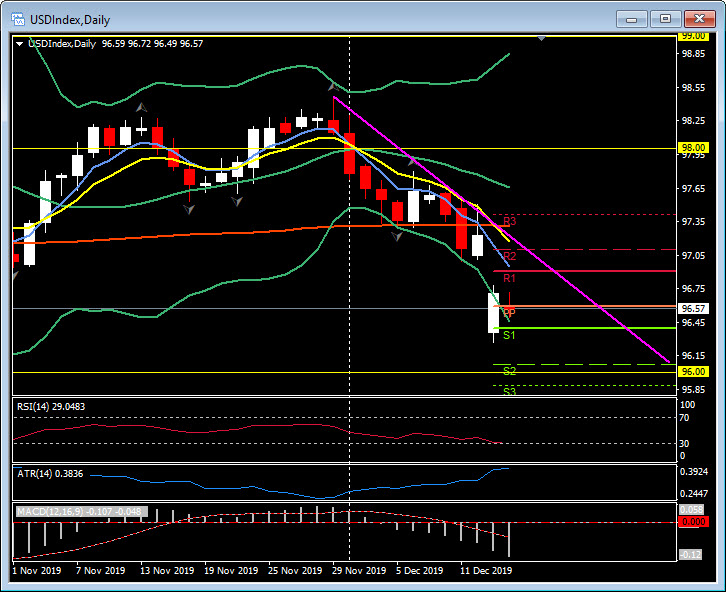

The dollar majors have been seeing typically narrow early-week ranges in quite year-end-approaching conditions. The narrow trade-weighted USD Index (DXY), at 96.97, was showing a 0.2% decline heading into the London interbank open, correcting about half the gain seen on Friday. The Index has been trending lower over the last two weeks, producing a five-and-a-half-month low last Thursday, at 96.59. The decline came amid a backdrop of rallying global stock markets, and associated gains in the Canadian Dollar and other commodity currencies, along with advances in Sterling and the Euro, as risks for a disorderly Brexit scenario evaporated. The optimism of this period proved to be justified, with the phase-1 trade deal between the US and China having been “totally done” (in the words of US Trade Representative Lighthizer), and with UK prime minister Johnson having gained a strong mandate to implement his Brexit deal with the EU after his Conservative Party won a commanding majority in the UK election last week.

This should leave markets to establish the Dollar at softer levels versus most currencies. The week ahead is packed with data releases, and the BoE and BoJ are meeting on policy this week, where both are expected to leave prevailing rates and settings unchanged. Several Asian central banks other than the BoJ meet this week, and all are expected to leave policy unchanged. US data releases should endorse the Fed’s decision to pause on policy after trimming rates three times this year. Focus will be on New Zealand data following strong New Zealand Dollar outperformance since early November after the RBNZ shifted gears. Australian employment data will also be a highlight. Preliminary December PMI data will be the prime focus in Europe, where expectations are for slightly firmer headline readings out of both the Eurozone and the UK.

Click here to access the Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.