The data calendar this week is quite busy, featuring, in chronological order, monthly labour market data today, January inflation figures (Wednesday), January retails sales (Thursday), and the preliminary January PMI surveys (Friday).

The UK employment is anticipated to hold steady at 3.8% in December data, though the average household income to dip to a 3.1% y/y rate in the three months to December. The headline CPI has forecasted to remain unchanged at 1.3% y/y rate, which is well off the BoE’s 2.0% target, though would fit the central bank’s projections. A 0.6% m/m rebound in retail sales is expected following the 0.6% contraction in December. As for the preliminary PMI data, the market consensus if for a dip in the headline composite reading, to 52.7 from 53.3, with service sector expansion seen slowing after the acceleration in January, and manufacturing sector activity dipping back into mild contraction.

Overall, the as-expected data will affirm a picture of a post-election rebound in activity. This, combined with markets anticipating a fiscally expansive 2020-21 budget presentation from the government in March, should keep the pound underpinned. The impact of the coronavirus hasn’t, by anecdotal measures, been much as yet.

On the Brexit front, concerns persist. The government has clearly signalled that it aims for divergence from the EU, and leave, without a new trading agreement if necessary, the Brexit transition period at the end of the year. This would imply the UK shifting to WTO trading terms and conditions, which would erode terms of trade. Bear in mind that when the UK leaves transition phase, it won’t just be leaving the EU’s single market and customs union, but also the 40 free trade agreement that the Union has around the globe.

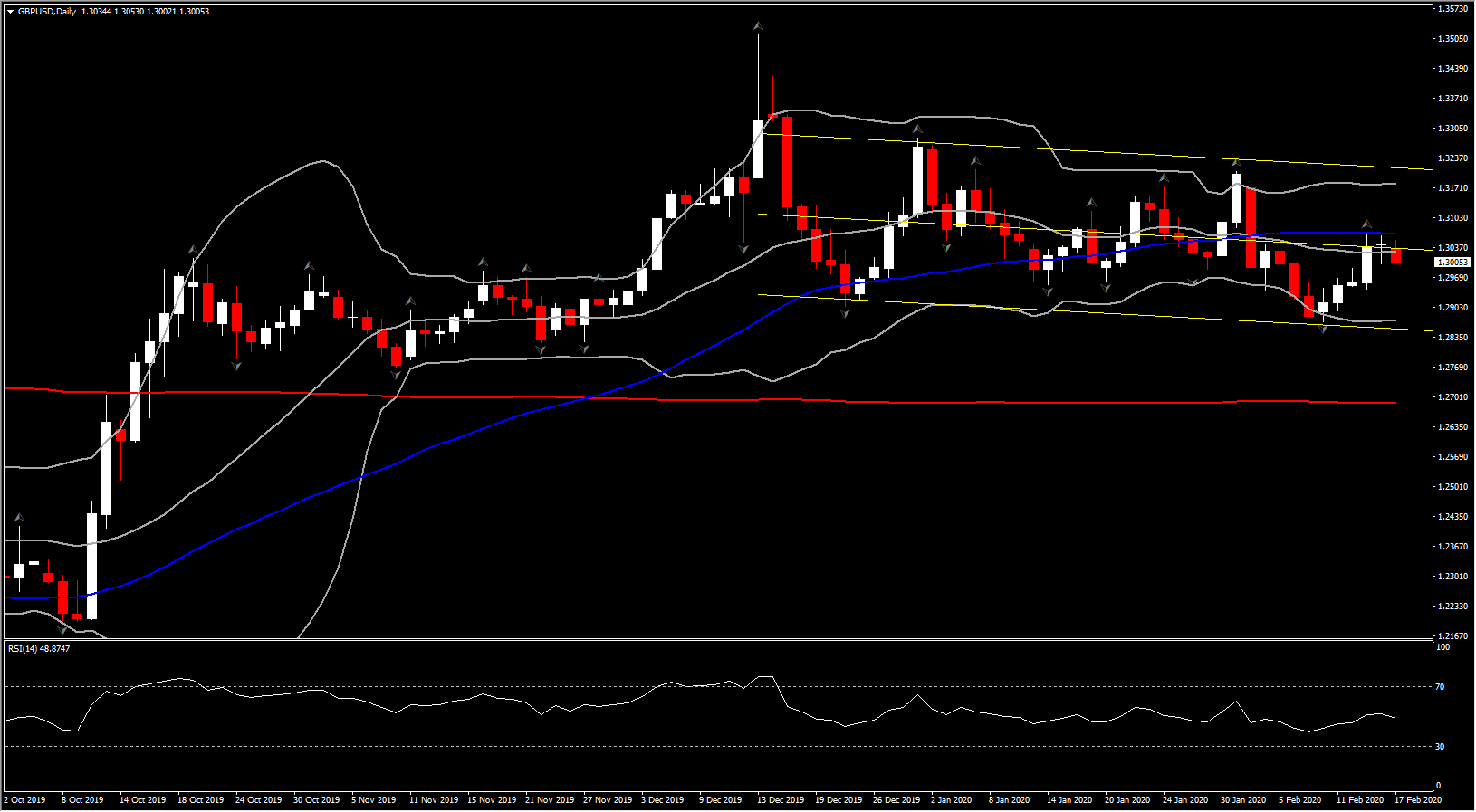

In currency market meanwhile, Cable has continued to consolidate gains seen mid last week following signs that the government is gearing up a fiscally expansive policy. The pair has pullback to 1.3000 area, off from the two-week high of last Thursday at 1.3069.

On the year-to-date, and from the mid-December election, the Pound has been trading mixed versus the other main currencies, lacking domestically generated directional bias. Political developments have seen UK Prime Minister Johnson strengthen his power, most notably with last week’s resignation of Chancellor of the Exchequer Sajid Javid, who was replaced by Rishi Sunak, which effectively green lights a fiscally expansive policy to finance major infrastructure projects (details are due to be announced at the government’s 2020-21 budget presentation in March).

Available January data out of the UK have also confirmed a rebound in economic activity as the fog of political uncertainty cleared following the general election. On the negative side of the balance are persisting concerns about Brexit.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.