GBPUSD, H1 & Weekly

UK March retail sales dove 5.1% m/m, the largest decline in the series history. The data captured some of the impact of the lockdown, which started on March 23rd and saw all non-essential retailing outlets close following official government guidance in response to the coronavirus pandemic. Clothing accounted for the biggest decline among the sub-sectors, contracting by 34.8% m/m, while food stores and non-store retailing were the only sectors to show growth. Sales at food stores rose 10.4% m/m, the biggest monthly jump on record, while online sales hit record high growth of 22.3% m/m.

Yesterday UK preliminary April composite PMI plummeted to a reading of just 12.9, down from 36.0 in March. As has been seen in other countries, the service sector drop was eye watering, diving to 12.3 from 34.5. This is the first month of data to fully capture the true impact of the coronavirus/lock, and so it hasn’t been a surprise, even if eyebrow-raising. The scale of decline in the composite reading is, of course, the biggest since records began in 1998, reflecting the extent of business mothballing. 81% of service providers and 75% of manufacturers reported a fall in business activity during April, which was overwhelmingly attributed to the pandemic. In the manufacturing realm, the small minority of businesses reporting output growth were involved in medical supply chains or producers of food or drink. Many sub-components fell by record amounts, but while staffing levels dropped there were numerous reports that the fall reflected the use of the government scheme to furlough workers. A ray of light came from business optimism for the year ahead, which lifted off its record low that was seen in March, and which likely reflected expectations for a phased reopening of the economy. UK markets were unperturbed by the report having already become well braced for the dismal run of data that’s only now starting to show the full impact of the global lockdowns. The data should help sharpen government about the trade-off between containing the coronavirus and economic prosperity.

However, the government is facing increasing criticism at home for its slow initial response and a focus on herd immunity, the very low level of testing and the lack of PPE for key front line staff. How to reopen economies before there is a cure or vaccine without risking a second wave of coronavirus infections is the major question, and current thinking is that it will take there being, other than social distancing, sufficient supplies of protective clothing along with availability of widespread diagnostic testing, which could take another month or two to realise.

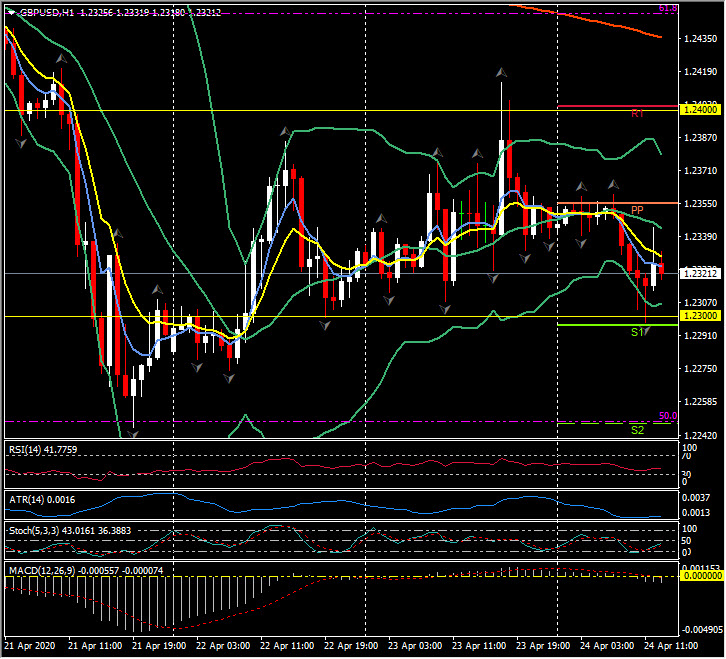

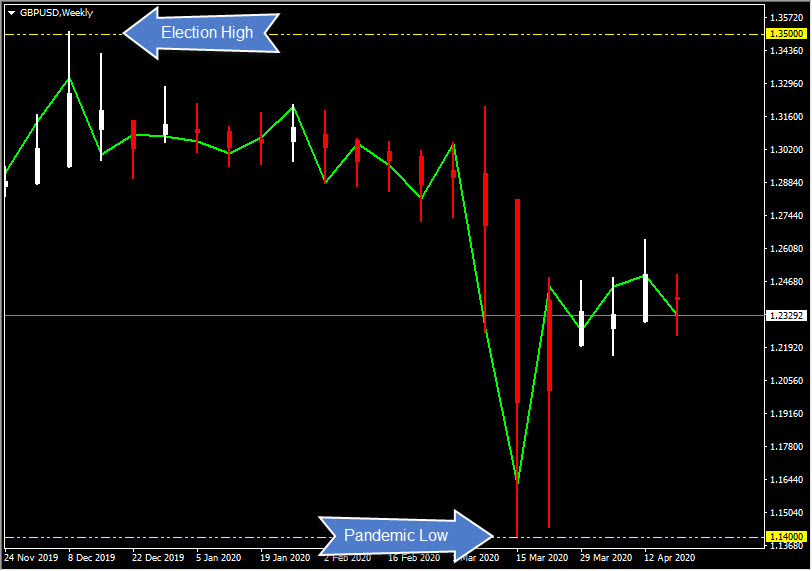

The Pound is up by over 8% from the 35-year seen in March, but is down by 7% on the year-to-date. The combo of the UK’s open economy, current account deficit and outsized financial sector, has meant that the Pound has been vulnerable to risk aversion in global markets.

As Deutsche Bank report today via Reuters¹ – “Britain – and by extension sterling – could well be a laggard as the major developed economies get back to work, and it cited two main factors.

The first centres on the still low level of virus testing relative to other rich economies, despite ambitious targets, and also opinion polls showing relatively high levels of support for a “hard lockdown” in Britain. Both these may affect the speed with which the country will likely re-open, it argues.

Even government minister Brandon Lewis on Thursday described the lack of virus testing in the country so far as “dreadful”.

The second factor was the relatively high exposure of a very services-dependent UK economy to prolonged distancing and economic disruption, with Deutsche citing data showing consumption makes up a whopping 84% of the economy – more than any other major economy apart from Brazil and Argentina.

Britain’s Office for Budget Responsibility last week forecast the UK economy would contract by 35% in the second quarter – more than three times similar estimates for manufacturing and export-heavy Germany.

“The UK appears to be caught in a double whammy,” wrote Deutsche Bank strategist Oliver Harvey. “This should ultimately translate into a relatively harder hit to growth and, on a structural basis, be bearish for the pound.”

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.