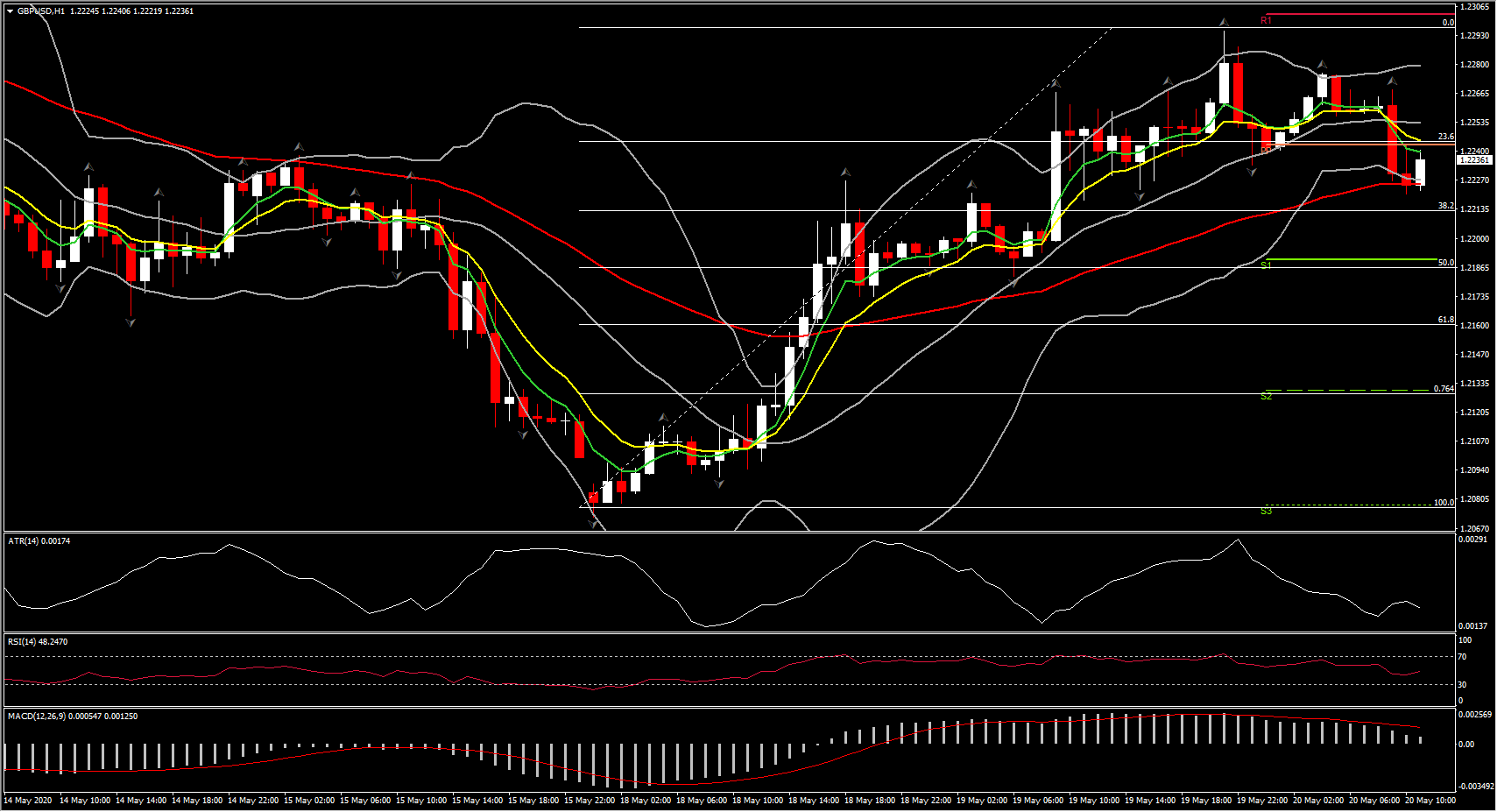

Sterling saw a moderate rotation lower against the Dollar, Euro and other currencies, correcting after rising over the previous two sessions. Cable ebbed to the lower 1.2200s, down from the 1-week high that was seen yesterday at 1.2297.

UK April CPI, released first thing in London, fell to a 0.8% y/y rate, the lowest level seen since August 2016 and down from 1.5% y/y in March. The outcome slightly undershot the median forecast for 0.9% y/y. Not surprisingly, falling energy and fuel pump prices contributed the biggest downward components to the shift in headline inflation, with core CPI consequently declining more moderately, to a rate of 1.4% y/y, from 1.6% y/y in the month prior, matching the median expectation. The rebound in oil prices over the last month, coupled with reopening economies, should put the brakes on the disinflationary trend.

The GBP will continue to take most of its directional cues from broad direction in global stock markets (to which the UK currency has been correlating positively with over the pandemic crisis era so far) and developments on the UK-EU trade negotiation front. The GBP’s upside is expected to be limited given risk of the UK leaving its post-Brexit membership of the EU’s single market at year-end. Negotiations between the UK and EU are coming to a head, with less than a month-and-a-half until the July-1st deadline for the UK to decide whether it wants to extended is post-Brexit transition membership of the EU’s single market (which includes 40 free-trade deals with global economies) beyond year-end.

From the technical perspective now,intraday a rebound above 1.2250 today could suggest the retest of 1.2300 territory as the asset remains well above May’s bottom with intraday momentum indicators sustaining a move above neutral zone.

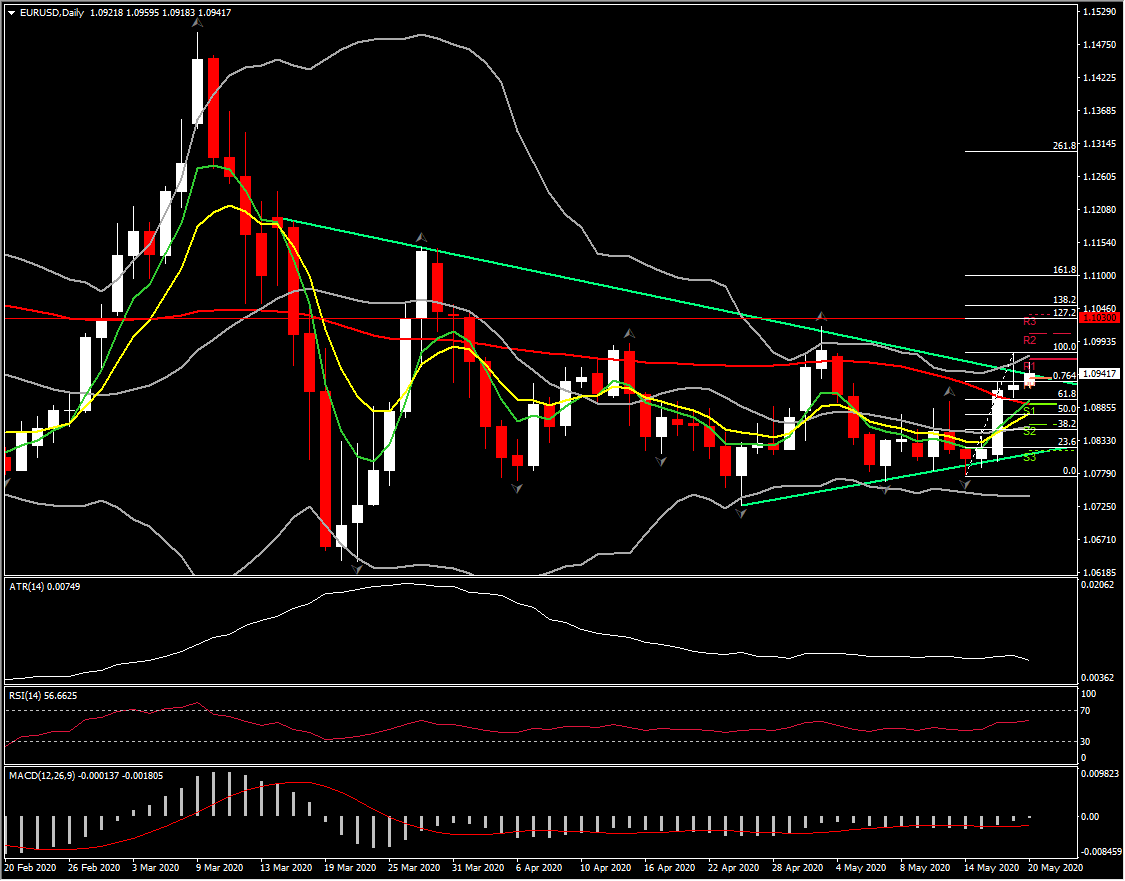

In Europe meanwhile, EURUSD traded slightly firmer, to levels near 1.0950, but remained comfortably shy of the 16-day high seen Tuesday at 1.0977. The asset was unaffected from the latest Eurozone data, with Eurozone HICP inflation down to 0.3% for April from 0.4%, core confirmed at 0.9%. The full breakdown confirmed that lower energy prices were a key factor behind the decline in the headline rate, with energy prices falling, while Food price inflation meanwhile is accelerating sharply, with the index for food, energy and tobacco rising 3.6% y/y in April, from 2.4% y/y in the previous month.

Against that background food price inflation is likely to remain elevated and while headline inflation rates are very low and support the ECB’s very expansionary policy, the absolute numbers are less reliable than usual as many prices are just not available with much of the services sector and many shops shut down.

Earlier, we saw the Eurozone current account surplus narrowed sharply in March – to EUR 27 bln from EUR 38 bln in the previous month. Accumulated data show a total surplus of EUR 338 bln – or 2.8% of GDP, down from 3.0% of GDP in the period to 2019. Still a substantial surplus and the financial account showed that non-residents made net acquisitions of euro area portfolio investment securities amounting to EUR 334 bln, up from just EUR 3 bln in the 12 months to March last year.

Hence with data being ignored for the time being , it seem that EURUSD remains in a positive outlook supported mainly by the USD weakness and also by the announcement on Monday that Germany’s Merkel and France’s Macron backed the creation of a jointly funded EUR 500 bln recovery fund, that would give the Commission the option of raising debt on the open markets.

Not an overly huge amount considering the size of the EU, but still a positive signal for markets, but also citizens. At the same time, ECB President Lagarde’s interview in a number of European newspapers signaled strong support, but also seemed to back the arguments of core countries, that for additional joint debt issuance in the Eurozone there also needs to be more co-ordination on fiscal policies. It is still a long way until monies will be paid out and likely tensions between countries most hit by Covid-19, like France and Spain, and those that so far have received the majority of EU funding – Hungary and Poland. Still, the signal that officials are eager to safe the union has done more to bring Eurozone spreads in over the past two days than the ECB’s latest announcements.

The ECB meanwhile will allot funds from the new loan facility designed to address the impact of the pandemic today (PELTRO), in a bid to further support liquidity. The data calendar focuses on U.K. inflation data at the start of the session.

EUR supported by USD weakness

EURUSD is ranging within 1.0930-1.0964 today, underpinned by broader dollar weakness, while the common currency found domestically-driven support yesterday from rare good-news from the data front, with the forward-looking German ZEW investor confidence for May surging back to a 51.0 headline reading — the highest since April 2015. In the medium term, the EURUSD continues to trade in a broad consolidation range to the south of the halfway mark of the volatile range that was seen during the height of global market panic in March, which was marked by 1.0637 on the downside and 1.1494 on the upside.The pair is expected to lack sustained directional bias for now, though the somewhat frayed politics of the Eurozone tips the balance toward downside risk in the long term.

In the near term however, momentum remains bias to the upside, with MACD extending higher, RSI is at 62 and Stochastic rebounding northwards from OS area. Meanwhile in the 1-hour chart Parabolic SAR turned below the price action suggesting that there is further potential to the upside. Next Resistance levels come at 1.0980, 1.1000 and 1.1030. Support remains at 1.0915.

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.