EURUSD, H1

The -323,000 initial claims drop to 2.123 million in the fourth week of March extended the -241,000 decline to 2.446 million (was 2,438 million) in the BLS survey week, leaving a decline that was largely in line with assumptions. More importantly, we saw a -3.860 million plunge in continuing claims to 21.052 million, as this measure has finally “turned the corner” to initiate it’s unwind starting in the May BLS survey week. Unfortunately, continuing claims still lie above the 18.011 million level seen in the BLS survey week in April, suggesting some deterioration in the job market between the two survey weeks. The May nonfarm payroll estimates have now been raised to -2.000 million from -2.200 million, though assumptions are still for a -400,000 factory payroll decline. Overall, claims are continuing to fall from the 6.867 million record high at the end of March, but we’re seeing a long lag between the gains seen in most high frequency measures of activity since mid-April, and improvement in the initial claims figures. It remains good news, however, that the inflow of workers to the pool of unemployed is lower than the outflow from re-openings, and this switch-over should accelerate over the coming weeks as payrolls rebound and the jobless rate commences its downtrend from an estimated 17.4% (was 17.5%) rate in May.

US Q1 GDP was revised to a -5.0% growth rate versus the -4.8% pace registered in the Advance report. In 2019 GDP posted growth rates of 2.1% in Q4 and Q3, 2.0% in Q2, and 3.1% in Q1. Consumption for the past quarter was bumped to -6.8% after sinking -7.6% in the Advance report, and versus the 1.8% clip in Q4. Business fixed investment dropped -7.9% (was -8.6%) and has declined for four straight quarters. Government spending was up 0.8% (was 0.7%). Inventories subtracted -1.43% versus Q4’s -0.98%. Net exports added 1.32% compared to Q4’s 1.51% add. The chain price index inched up 1.4% from 1.3% in the Advance report, previously, while the core rate decelerated to 1.6% from 1.8%.

US Durable Goods orders dropped another -17.2% in April after March’s -15.3% (was -14.7%) decline. Transportation orders collapsed -47.3% from the prior -43.1% (was -41.5%). Excluding transportation, orders were down -7.4% from -1.7% (was -0.6%) in March. Nondefense capital goods orders excluding aircraft dropped -5.8% from -1.1% (was 0.1%). Durable shipments declined -17.7 % from March’s -5.5% (was -4.7%). Nondefense capital goods shipments ex-aircraft fell -5.4% from -1.2% (was -0.3%). Inventories edged up 0.2% from the prior 0.6%. The inventory-shipment ratio spiked to 2.21 after jumping to 1.82 (was 1.81).

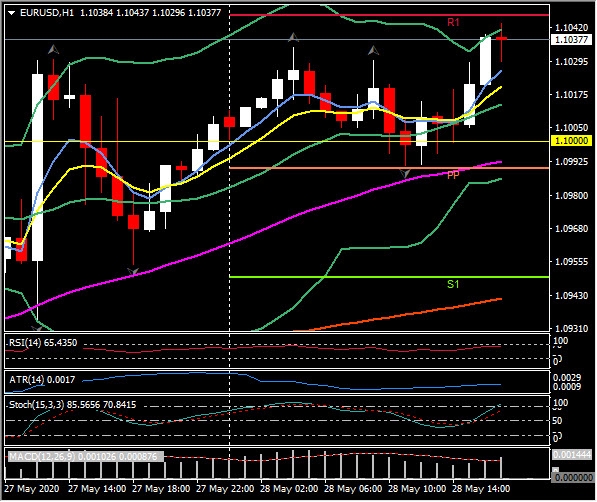

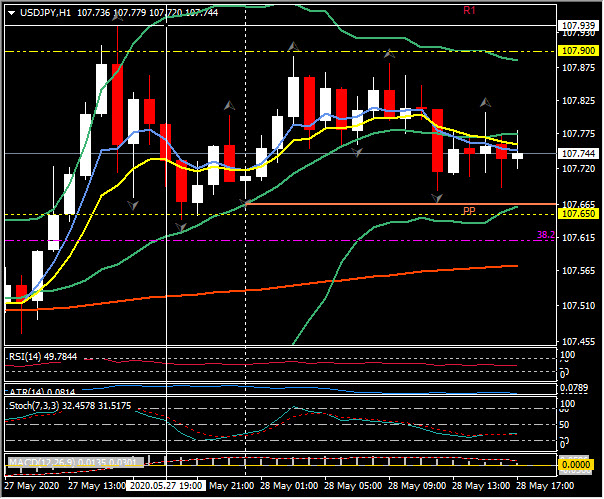

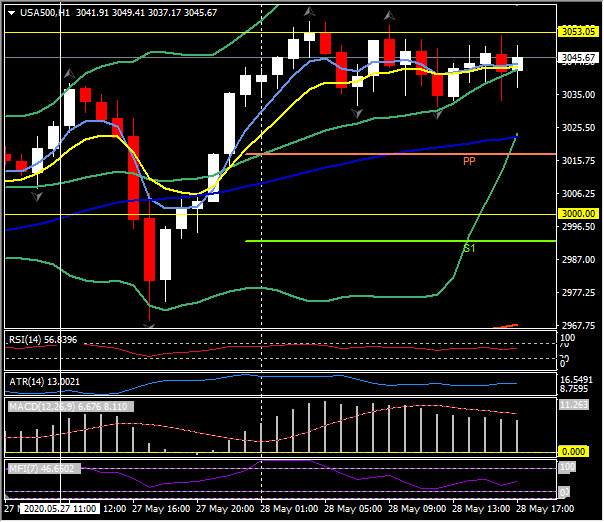

USD was pretty much static following the mix of data, EURUSD holds over 1.1000 and trades at 1.1035, USDJPY flat for the day at 107.70 from highs of 107.89 and lows at 107.68. US Equity markets have opened flat, whilst Futures remain bid with USA500 trading at 3040, down from the day high at 3056.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.