AUDUSD, H1

The Dollar and Yen rose and commodity currencies underperformed amid safe haven positioning in global markets. Stock markets in the Asia-Pacific region have declined sharply, and S&P 500 futures racked up a loss of nearly 3% at the lows (subsequently retracing to a 2% loss in opening cash trades), while oil prices were showing a near 5% loss at the lows. Front-month USOil prices printed a two-week low at $34.36, which is over $6 down on the three-month high that was seen a week ago. Concerns about a second wave of coronavirus infections remain front and centre. Beijing has reported a new cluster of cases, originating from a wholesale food market, forcing the city to enact lockdown measures. Also, the r-rate has been creeping back above 1, indicating an exponential spread, in a number (13) states in the US and some areas in Europe. UK shops reopen today, despite the r-rate being back above 1 in some parts of northern England.

The US Empire State manufacturing index jumped 48.3 points to -0.2 in June, much better than expected, after rallying 29.7 points to -48.5 in May, which was the second worst print in history. The -78.2 from April is the record low (and was a record -56.7 drop). The 2019 high was 14.4 in May. Gains were broadbased. The employment component improved to -3.5 from May’s -6.1 and has risen from -55.3 in April. The workweek increased to -12.0 from -21.6. New orders surged to -0.6 from -42.4. Prices paid climbed to 16.9 from 4.1, with prices received at -0.6 from -7.4. The 6-month index nearly doubled to 56.5 from 29.1, and is up from 7.0 in April and 1.2 in March. The future employment gauge was up to 19.0 from 10.4, with new orders at 52.9 from 35.0, while prices paid were 25.6 from 20.3, with prices received at 7.5 from 2.0.

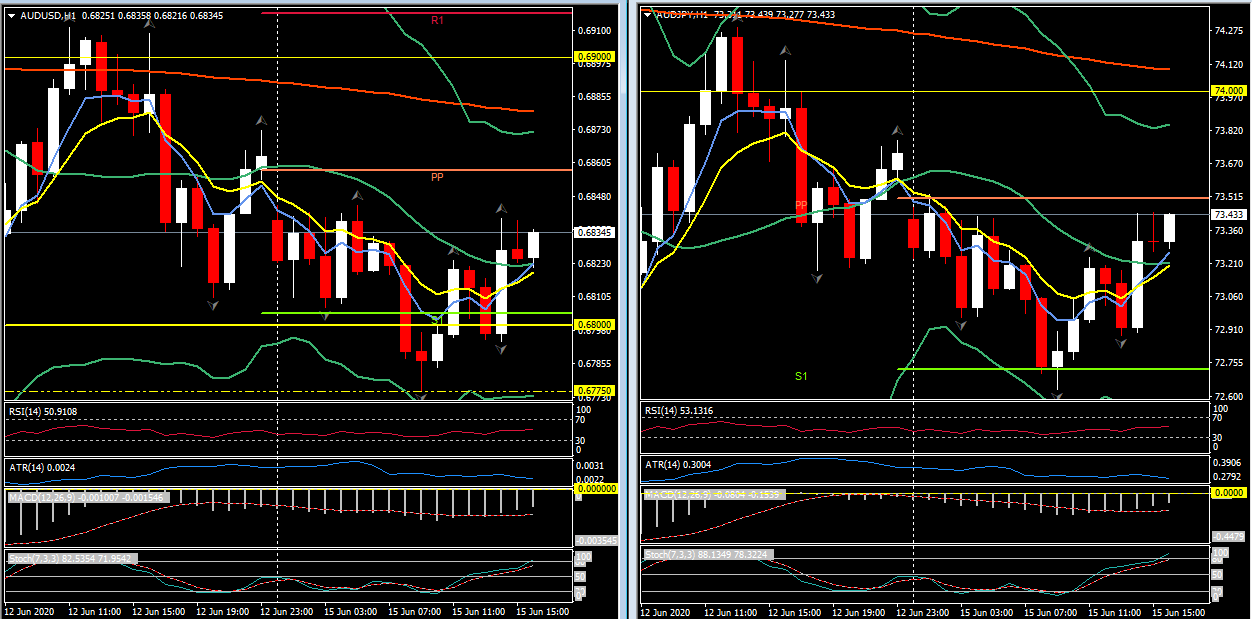

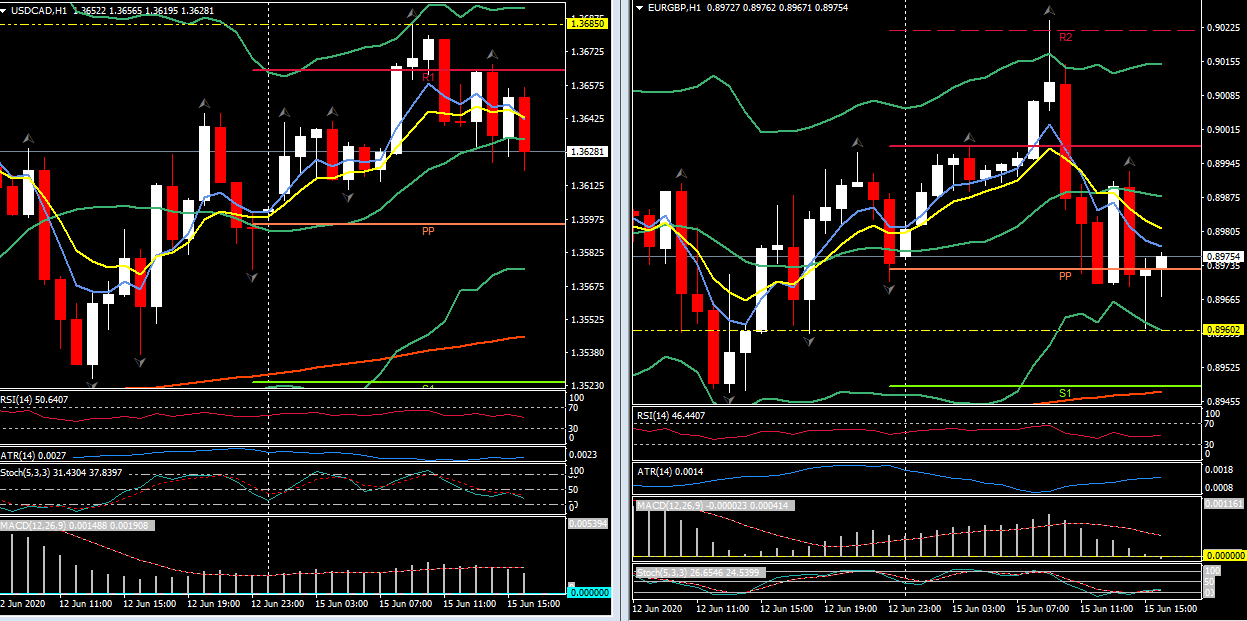

In the currency realm, the biggest mover out of the main dollar pairings and cross rates has been the risk-sensitive AUDUSD, which fell by more than 1.1% in posting a 13-day low at 0.6776. AUDJPY declined by nearly 1%, while NZDUSD and NZDJPY fell by similar magnitudes. The Canadian Dollar and other oil-correlating currencies also rotated lower. This lifted USDCAD by over 0.7% to a two-week peak at 1.3685. USDJPY edged out a low at 107.00, which is about 35 pips below Friday’s New York closing levels, though the pairing subsequently found its feet, with the Dollar itself finding demand as a safe haven currency. The narrow trade-weighted USDIndex posted a high at 97.39, though remained shy of the 11-day peak that was seen on Friday at 97.45. EURUSD concurrently carved out a low at 1.1227, remaining above the 11-day low the pairing saw last week at 1.1212. Sterling’s pandemic-era proclivity to underperform during risk-off phases in global markets has once again been on display. Cable posted a two-week low at 1.2455, while the Pound concurrently hit a two-week nadir against the Euro, at over 0.9022. The Pound managed a bounce after European Commission president von der Leyen said that the EU was ready to intensify trade talks. EURGBP tested down to 0.8960 ahead of the US open.

Click here to access the HotForex Economic Calendar

Stuart Cowell

Head Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.