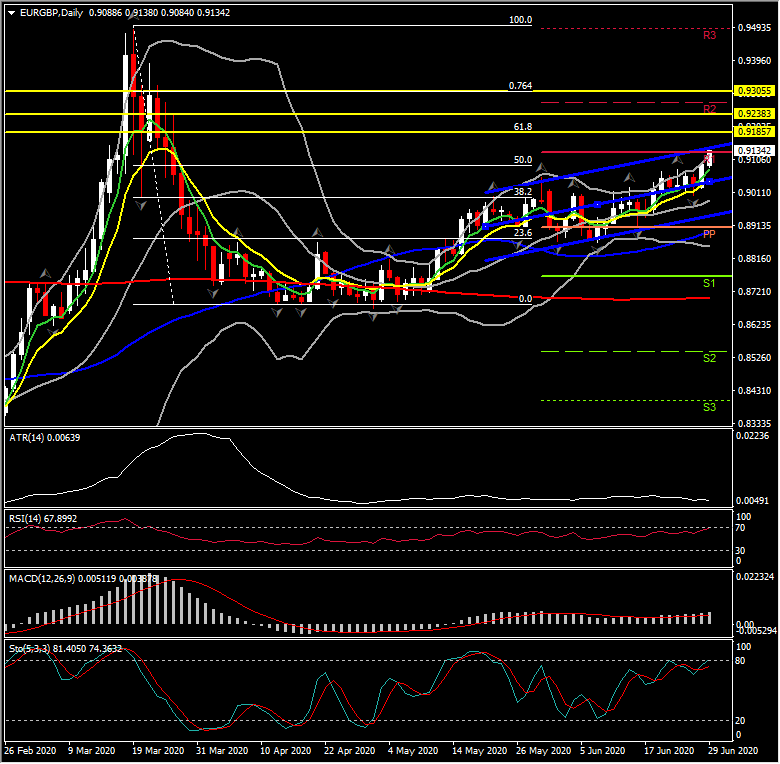

Cable has found a footing in the mid 1.2300s after last week tumbling from the mid 1.2500s, which culminated late Friday with a 1-month low at 1.2312. EURGBP, meanwhile, has printed a fresh 3-month high, at 0.9104, making this the fourth consecutive week of higher weekly highs.

Euro positive factors

A combo of the upcoming EU recovery fund, which is being greeted as a Euro positive by most analysts, and the market perception that the BoE is unwinding monetary stimulus prematurely, has been underpinning EURGBP. Additionally, the comments from a top German judge suggesting that it is now up to the ECB to decide whether to participate in the ECB’s bond purchase program were taken as positive, especially after the ECB last week released some documentation justifying its extension of the QE program.

In general the EU’s proposed EUR 750 bln multiannual financial framework fund has been interpreted as a factor that supports the EUR against all majors, as according to Morgan Stanley analysts, the EU proposal means that some of the risk premium for EU break-up risk will abate, and that the creation of a new large and liquid, higher-yielding AAA asset will attract inflows from real money investors and reserve managers. The team at MS is forecasting EURUSD at 1.2000 by Q2 next year.

For now however the medium term picture remains cautious as there is a long road back to economic normalcy, especially in hospitality and tourism that is likely to remain a problem in the coming months, and likely won’t be achieved until such time as there is a vaccine or effective treatment for the SARS Cov-2 coronavirus. The latest proof is the Eurozone ESI economic confidence this morning which was improved – but less than expected.

The services sector in particular continues to face ongoing restrictions, with travel, holiday and hospitality still hit hard by the fallout from Covid-19 and in countries such as Italy, Spain and Greece, which disproportionately rely on tourism it will be a difficult come-back for many companies, despite temporary government support measures. Borders have re-opened now and the EU is set to publish a list of countries deemed to be sufficiently safe to allow travel to this week, but the balance of risks remains tilted to the downside and the weaker than expected rebound in the headline acts as a reminder that it will be a long way back to pre-crisis activity levels for many countries. Additionally, the rising jobless numbers in Germany and the Eurozone will likely keep a lid on headline rates going forward.

Now in regards to the UK and the Pound, the Pound is expected to remain under pressure in the weeks ahead, assuming there won’t either be a significant breakthrough in UK-EU trade talks, nor a walk back in the BoE’s apparent tapering in QE.

Meanwhile, the UK economy looks to be in a vulnerable position, too. The risk of a narrow trade agreement, or no trade agreement at all, with the EU remains very much on the cards at a time when it’s becoming apparent that a V-shaped recovery from the pandemic lockdown is going to more likely resemble an “L” shape, at least for a good while (scientists at Oxford University, who are among the leaders in the pack of researchers developing candidate vaccines, say that a vaccine is not likely to be ready for global rollout until the latter portion of 2021).

This is not an ideal combo for an open economy with a large currency account deficit. We expect this backdrop to translate into a weak pound, even though the currency is already running at about an 11-12% trade-weighted discount compared to the average levels in the several years preceding the vote to leave the EU in June 2016.

Hence as EURGBP, from the fundamental and technical perspective, remains bullish, the asset could turn back to March highs. It has been in an uptrend since early May , while it has reversed more than 50% of the downleg seen in March. Daily momentum indicators are positively configured with RSI looking northwards and readying to cross the 70 barrier, and MACD keeps extending higher while BB are extending to the upside as well. Next Resistance levels to be watched are 0.9185 (61.8% Fib. level.), 0.9238 (March 26 high) and 0.9300 (76.4% Fib. level.)

Stocks of UK companies that derive the majority of their revenue domestically will also be apt to underperform, while stocks of larger-cap corporations, which in the UK are highly international entities, will likely hold their own relative to global peers. Triple A rated Gilts should continue to remain a safe haven asset for investors, though ratings agencies are monitoring the endgame of Brexit carefully. The next round of trade talks is due in July, though October will — as the EU’s chief Brexit negotiator Bearnier said last week — be “the real moment of truth.”

Click here to access the HotForex Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.