May and June data out of the UK, as elsewhere, have showed a strong rebound from April, when the coronavirus lockdown measures were in full force. However, the path ahead looks to be a rocky one. New lockdown measures being re-introduced in city of Leicester, due to a spike in coronavirus cases there, is an ominous sign of the challenges being faced as the UK economy reopens.

Concerns also remain about the risk of the UK leaving its transitory membership of the EU’s single market at year end and shifting to trade on less-favourable WTO terms. Trade negotiations remain in deadlock, with the latest round of talks having ended last Thursday, a day earlier than planned. The EU’s chief negotiator Barnier said, “after four days of discussions, serious divergences remain.” There is also a prevailing view that the BoE might be prematurely tapering its QE program.

As in other economies, the primary focus is now on the r-rate of new coronavirus infections amid the de-restricting of social and economic activity. The UK’s hospitality industry reopened on Saturday, which along with a halving in the government’s two-metre social distancing guideline, will present a challenge to maintaining a sub-1.0 coronavirus infection r-rate.

The UK-EU post-Brexit trade issue is not likely to be resolved until October, the deadline for when an agreement has to be made before the UK’s access to the single market ends. The risk is that there will only be a narrow deal, or no deal at all, leaving the UK on much less favourable terms of trade.

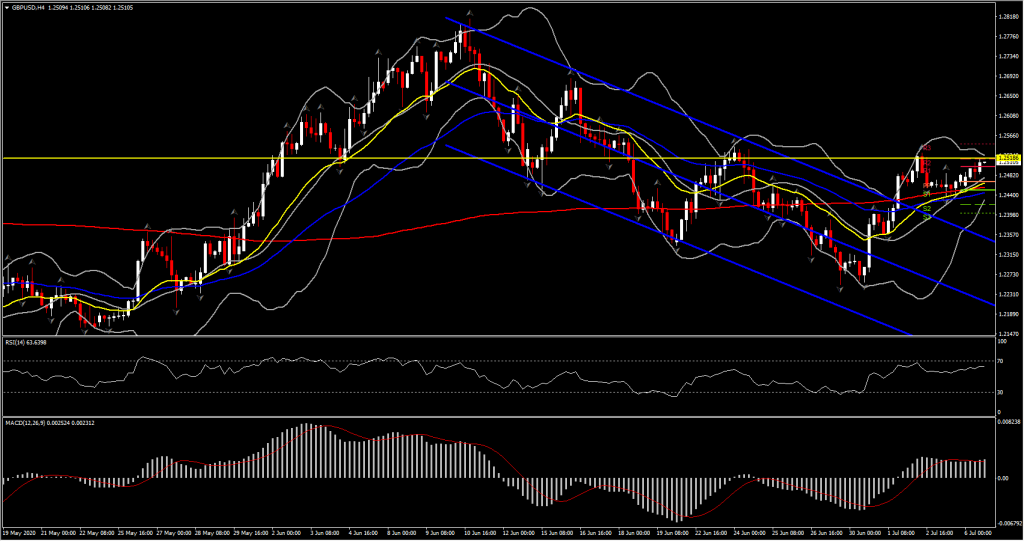

Hence as the UK calendar this week is quiet, risk-on positioning has been ensuing so far today and is expected to hold for the whole week. The underperformance in the Dollar and Yen, boosted Cable to a 4-day high at 1.2518, further above the Flag formation seen the whole of June, while EURGBP lifted out of Friday’s 0.9003 18-month low to a 5-day high at 0.9056 as Euro has been supported by data releases in Europe this morning. The data showed rebounds in German manufacturing orders and Eurozone retail sales in May, but volumes remain below the levels seen last year. Still, a UK construction PMI that jumped above the 50 point no change mark in June and a further marked improvement in Eurozone Sentix investor confidence helped to underpin sentiment.